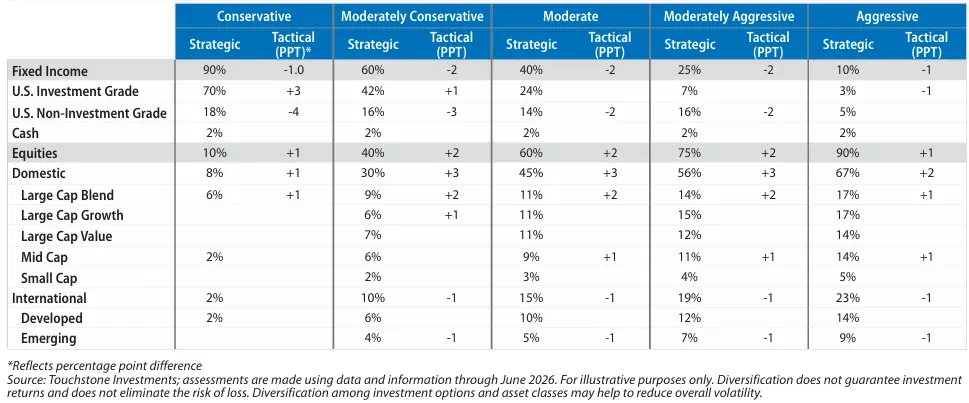

Fixed Income

Weight: Moderate Underweight

We lowered our tactical stance to a moderate underweight as we see more attractive return opportunities in equities and potential inflation related risks.

Duration

Weight: Slight Overweight

We maintained a slight overweight duration stance. While inflation risks have increased, current yields provide a more meaningful income cushion than in recent years, and we do not believe inflation pressures will be sufficient to trigger a sustained rise in long-term yields.

U.S. Taxable Investment Grade

Weight: Neutral

We moved to a neutral position funding our equity overweight. We continue to be drawn to the higher yields and lower economic sensitivity found within corporate and securitized credit.

U.S. Taxable Non-Investment Grade

Weight: Moderate Underweight

We remain underweight high-yield bonds. Credit spreads remain near historic lows, while yield sits only modestly above the historical median. This suggests little cushion should inflation rates rise or economic growth falter.

Equities

Weight: Moderate Overweight

We increased equities to a moderate overweight, supported by improving economic data, progress toward reopening the Strait, and continued strength in earnings. AI remains the dominant market driver.

U.S. Large Cap Blend

Weight: Moderate Overweight

Strong earnings growth and continued AI-related investment have supported equity markets, and now we are seeing progress in the reopening of the Strait. 1Q earnings were very strong, and forward estimates continue to move higher.

Growth

Weight: Neutral

We removed our underweight to Growth in March after valuations improved. AI remains a key earnings driver, though, risks persist given potential delays in data center construction and AI’s potential to disrupt industries.

Value

Weight: Neutral

The Value index contains a diverse mix of defensive, cyclical, and even growth-oriented companies that have migrated from Growth benchmarks. While we see attractive opportunities within the universe, we believe they are best captured through active management rather than passive.

U.S. Mid Cap

Weight: Slight Overweight

We hold a slight overweight, supported by more attractive valuations and potential earnings growth. Within mid caps, we prefer high-quality companies with strong cash generation.

U.S. Small Cap

Weight: Neutral

We remain neutral but see growing reasons to consider an upgrade. Earnings revisions have improved, participation has broadened across industries benefiting from AI-related spending, and lower fuel prices could help alleviate pressure on consumer-oriented businesses.

International Developed

Weight: Neutral

Developed international equities stand to benefit from lower energy prices, although higher interest rates and inflation pressures are headwinds. While valuations are relatively attractive, we believe some discount is warranted given ongoing structural growth challenges, particularly in Europe. We maintain a neutral allocation.

International Emerging

Weight: Slight Underweight

We remain slightly underweight. With roughly 80% of the index concentrated in Asia, emerging markets remain sensitive to energy costs and external demand. Although a resolution in energy markets would be supportive, normalization may take time, warranting a more cautious near-term stance.

Strategic: Strategic asset allocation is a baseline allocation between asset classes established with a longer term focus and congruent with an investor’s investment goals and objectives. The allocation is meant to optimize the asset mix through methodical diversification in an attempt to maximize return and lessen risk.

Tactical: Tactical asset allocation is differentiated from strategic asset allocation by having a much shorter time horizon and the goal of adding alpha beyond what would be allowed through static strategic weights. Markets tend to be more volatile over shorter time horizons, while longer time frames tend to smooth out that volatility. That enhanced volatility in the short term creates the opportunity for either return enhancement and/or risk reduction by adding to or reducing weights of different asset classes.