Risk of a bitter debt ceiling fight was brought to light as House Republicans needed 15 votes and numerous compromises just to elect House speaker Kevin McCarthy. It is unclear at this point what promises McCarthy made, but one Republican that eventually voted for him had previously stated that he would only vote for McCarthy if he agreed not to raise the debt ceiling and would instead shut down the government and default on the national debt.

For now the markets do not appear that concerned, though it is still early. We have been through this before and politicians eventually relented and found a way to compromise as the massive threat of default created too much political risk. We believe this will be the likely outcome this time, though the political gambling ahead of such a potentially economically damaging outcome may introduce significant risk in terms of asset and rate volatility. Even averting the crisis, we think the political compromise may entail some austerity measures (government spending cuts) that could be concerning for the markets and potentially slow economic growth.

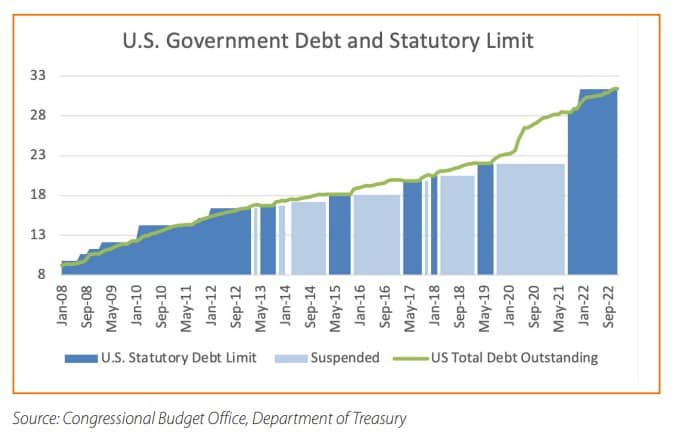

According to Treasury Secretary, Janet Yellen, we have already bumped up against the debt ceiling. The Treasury Department will now use “extraordinary measures” to meet obligations in the short-term by shifting around funds. It is believed that these measures could take us into the summer. So we have time, but if they run out of things they can do it could result in not paying certain bills. At that point, Congress would need to either lift the debt ceiling, suspend it, or let the government default.

The government would not necessarily default on its debt, as there is plenty of cash flow to cover interest payments, but rating agencies would likely consider missed payments on obligations as a technical default. Even a technical default would be destructive for our economy as it would be expected that rating agencies would likely downgrade our debt putting upward pressure on interest rates and downward pressure on the U.S. Dollar. In fact a representative from Fitch, a rating agency, stated that the inability to meet obligations would not be consistent with a triple-A rating. It is difficult to speculate just how damaging a U.S. debt default would be, but severe enough that we believe politicians are unlikely to trigger it.

Shutdown versus Default – What's the Difference?

It might be helpful to distinguish the difference between a shutdown and a default and how they have played out politically in the recent past. A shutdown occurs when Congress fails to pass legislation to authorize government spending, while a default occurs when Congress fails to increase or suspend the debt ceiling. Each are triggered when the Treasury can no longer continue to fund obligations. While they sound similar only one is considered a technical default and is what matters to the markets.

In late 2018 the government shut down for 35 days, the longest in history, as President Trump refused to sign a bill that didn’t include funding for a wall on the Mexican border. Over the time of the shutdown the S&P 500 rallied 13% – though that was after a steep market decline in the fourth quarter of 2018 tied to economic concerns following monetary policy tightening. One thing that did fall was President Trump’s ratings, which we think may have influenced his decision to endorse a stopgap bill to reopen the government. Prior to that, in 2013, the government shut down for 15 days, this time over the Affordable Care Act where the Republican – controlled House wanted to defund it. The S&P 500 rose 2% with that shutdown. We believe it was voter discontent with the shutdown that appeared to shift the Republicans off of their demands.

More significant for the markets was the debt ceiling crisis of 2011. The Republicans had just taken over the House and were demanding spending cuts in exchange for an increase in the debt ceiling. Two days before the government was expected to run out of funds the Democrats relented and agreed to $2 trillion in spending cuts (most of these cuts were later reversed). We would speculate that Democrats may have been influenced by the decline in the market (the S&P 500 fell 17% in the few weeks leading up to the deadline) as well as fearful headlines suggesting another financial crisis in the event of a default.

The Democrats may feel emboldened by the government shutdowns in 2013 and 2018, but a default is very different from a shutdown. Also it is unclear whether voters would be supportive of Democrats taking a hard stance. In our opinion, after 3 years of massive government spending programs a proposal to reduce spending may not upset voters in the same manner as funding a border wall or defunding the Affordable Care Act. Additionally the economic risk would be much greater. In fact it is unclear how damaging a default would be, but this is the largest economy in the world, and our currency serves as the world’s reserve currency. So we surmise it would be hard to overstate the damage a true default would cause.

Conclusion

We don’t believe Congress will let the government default, as the economic risks are too high. But given how polarized the government has become (even within parties), we expect to be made very uncomfortable with this prediction. As Winston Churchill was believed to have stated, “Americans will do the right thing – after they have tried everything else.” It is likely that there will be a deal that includes significant spending cuts to discretionary spending with the defense budget potentially to be hit the hardest. It is less certain whether mandatory spending portions of the budget get addressed. Entitlement cuts would be much less politically palatable, though we believe we do need to address our entitlement programs, and think it would be less economically impactful if we were to address them sooner than later.

Please see our debt research for more on entitlements.

Glossary of Investment Terms and Index Definitions

The information provided reflects the research and opinion of Touchstone Investments as of the date indicated, and is subject to change without prior notice. Past performance is not indicative of future results. There is no assurance any of the trends mentioned will continue or forecasts will occur. Investing in certain sectors may involve additional risks and may not be appropriate for all investors.

The indexes mentioned are unmanaged statistical composites of stock or bond market performance. Investing in an index is not possible.

Please consider the investment objectives, risks, charges and expenses of the fund carefully before investing. The prospectus and the summary prospectus contain this and other information about the Fund. To obtain a prospectus or a summary prospectus, contact your financial professional or download and/or request one on the resources section or call Touchstone at 800-638-8194. Please read the prospectus and/or summary prospectus carefully before investing.

Investment return and principal value of an investment in a Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. All investing involves risk.

Touchstone Funds are distributed by Touchstone Securities, Inc.*

*A registered broker-dealer and member FINRA/SIPC.

Touchstone is a member of Western & Southern Financial Group

Not FDIC Insured | No Bank Guarantee | May Lose Value