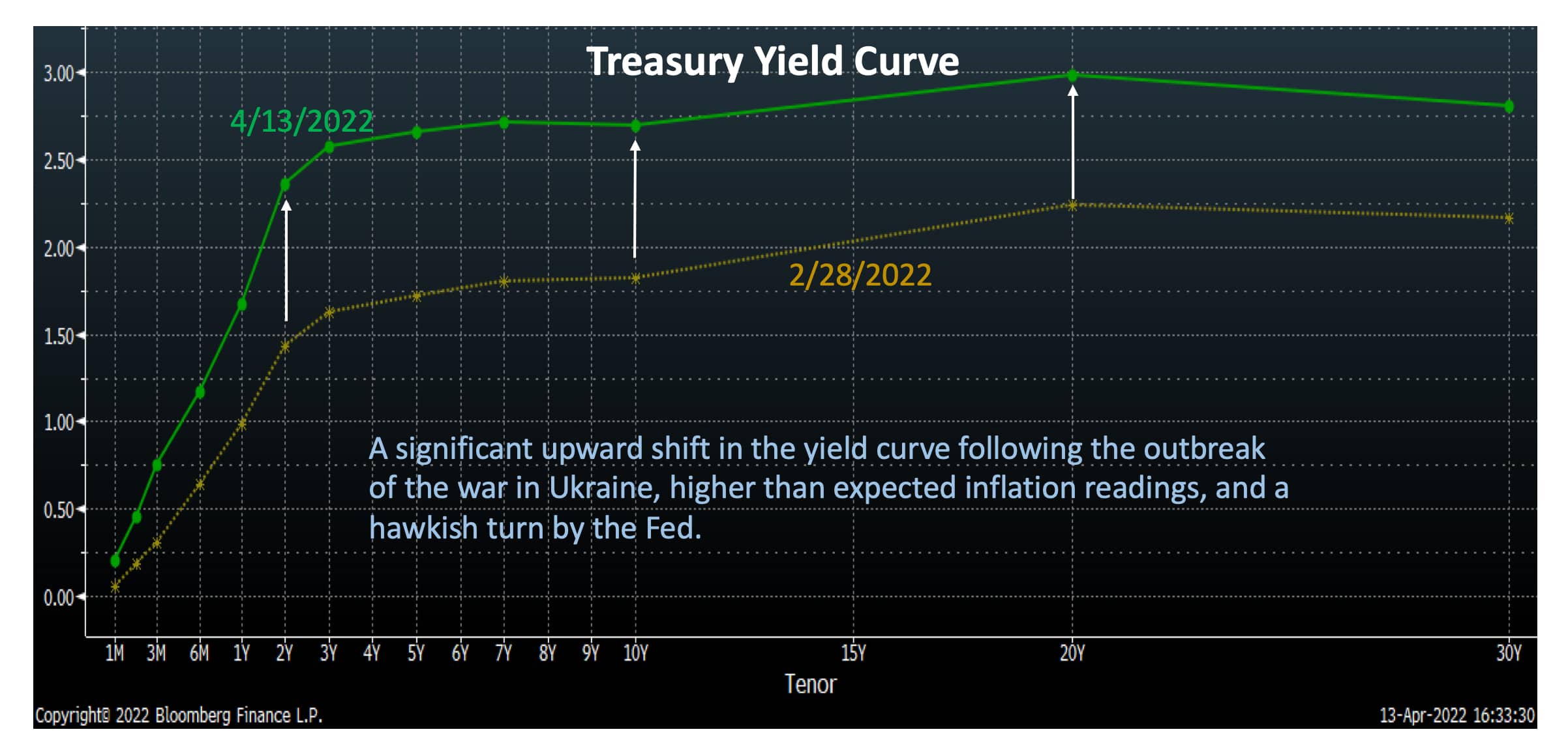

The speed of this cycle is breathtaking. Our Stage of the Economic Cycle Model has moved from early to late cycle conditions in less than two years’ time. In the month since putting together our last Quarterly Themes much has transpired and we want to keep you abreast of our thoughts on those changes. Most impactful has been the change in interest rates and the tone of the U.S. Federal Reserve Board (Fed). Since the end of February, 10 year Treasury yields have jumped nearly 100 basis points (up more than 50%). And the Fed has communicated that it is willing to sacrifice economic growth to tame inflation.

*Model based on Capacity Utilization, Unemployment Rate, Treasury yield spreads, Consumer Confidence Indexes, and Conference Board business cycle indicators

Source: Bloomberg

We do not believe the speed of change will slow. In fact we believe that investors need to prepare for more market volatility. The Fed has only one way to deal with inflation, and that is to slow demand. The Fed is now telling us in no uncertain terms that they are going to lower inflation. We should take that message seriously. The big unknown is just how far the Fed will need to go.

Source: Bloomberg

Source: Bloomberg

There are many factors to consider. Working in the Fed’s favor: Both the rate of inflation and economic growth was already expected to slow this year due to the removal of fiscal stimulus and a natural slowing from a near record high rate of growth in 2021. We are also seeing early evidence of an easing in supply chain conditions. On the other hand, sanctions on resource rich Russia and COVID-19 outbreaks in China are likely to keep inflation running higher than originally expected and recent inflation reports point to a broadening of price increases to more sticky items like homeowners equivalent rent. Meanwhile, the economy continues to open and consumers are signaling a desire to spend more on leisure, travel, and entertainment where labor conditions remain very tight.

Source: Bloomberg

Source: Bloomberg

With the exception of the very short end, much of the yield curve has already risen considerably. While there is certainly the potential for more, we believe we are nearing the end. Our 10 year Treasury yield model suggests that the yield should be closer to 3.5% today, but it is not a forecast model. The large difference between the Federal Funds rate and the 2 year Treasury note yield is what is guiding our model to suggest a higher yield for the 10 year Treasury. But if we substitute currently implied Federal Funds rate expectations for year end, then the model indicates a 10 year yield below 3%.

Source: Bloomberg

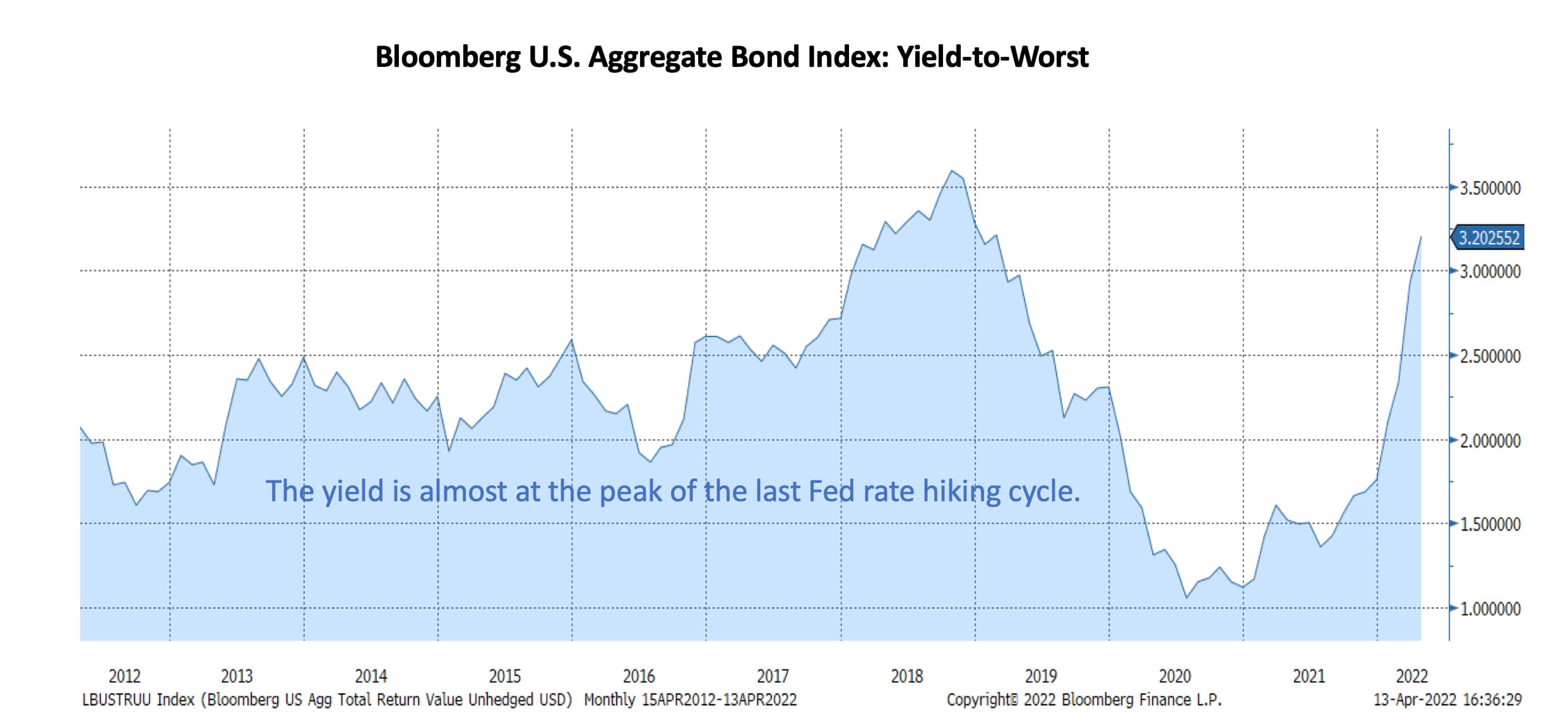

After the jump in yields, we moved our duration recommendation from a slight underweight to one that is equivalent with the Bloomberg U.S. Aggregate Index. Even the yield on the Bloomberg U.S. Aggregate Index looks interesting at 3.2% in mid April. It is significantly above the 10 year average and very near the highs reached in late 2018 (when the Fed had to stop raising rates). Certainly, if adjusted for current inflation this yield doesn’t look attractive. We are making the assumption that inflation slows, considerably over the next 18 months. Why?

• Economic growth is slowing.

• Wages are not keeping up with inflation.

• Fiscal stimulus has ended.

• The Fed is tightening policy.

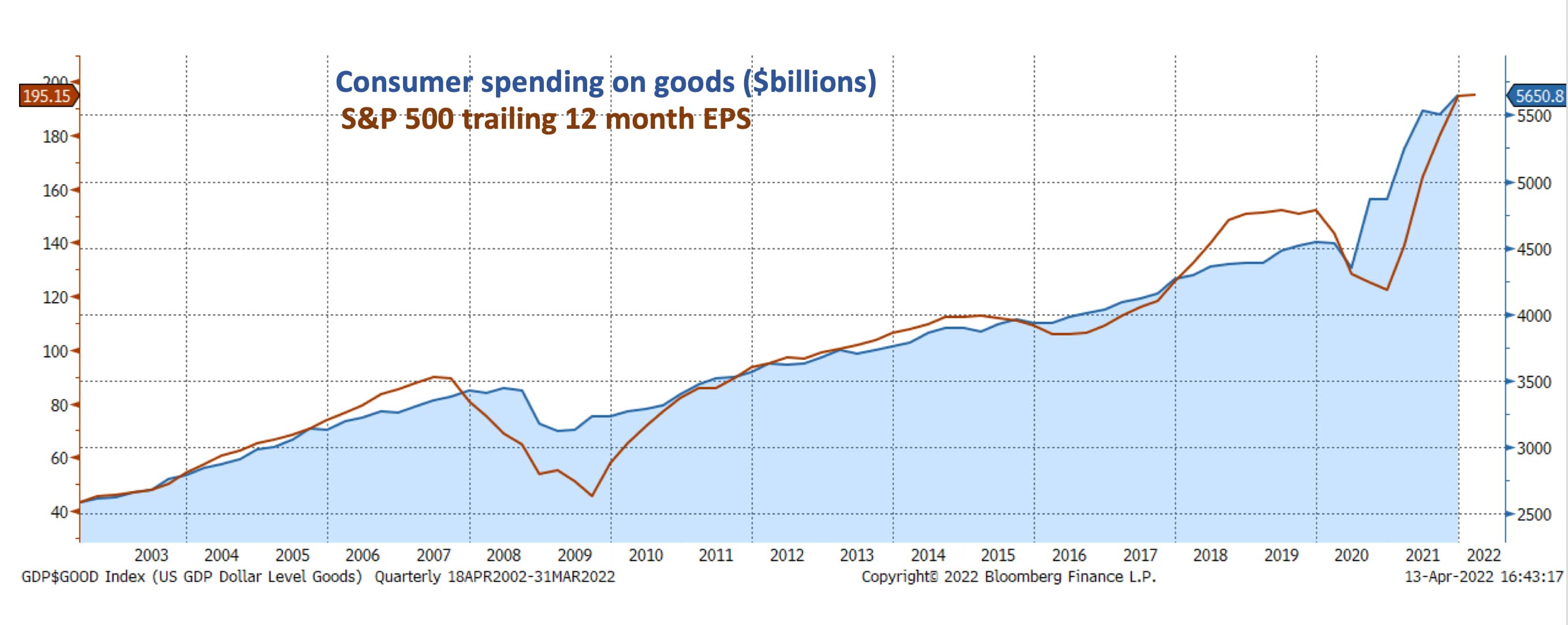

• Consumer spending is expected to shift from goods to services.

The other main market issue we see revolves around forward earnings growth for equities. This first quarter earnings season should be okay, with companies still able to pass through price increases and demand still strong. It is the remainder of the year that could become more difficult. Wage increases have not kept up with inflation and continued high food and energy prices are likely to impact demand for other items, at the margin. Higher interest rates are likely to slow demand for big ticket items like housing. And then there is the likely shift in consumer spending toward services and away from goods. This is important as goods spending has a much higher representation in the S&P 500 than it does in our economy. This is one of the reasons that the market and earnings responded so favorably to the stimulus induced spending boom during the pandemic.

Source: Bloomberg

We believe there is a lot of change coming over the next 6 months and that investors should be proactive in positioning their portfolios. What can investors do? Get active and look for companies that have strong competitive advantages, unique products, less cyclicality, strong balance sheets, high ROIC, exposure to a services rebound, and stock valuations that leave some margin for error.

These considerations should be helpful for positioning within the market, but what about the market as a whole? Ultimately we think it comes down to whether the Fed pushes the economy into a recession or not. Fed policy impacts the economy with a lag, so a recession starting sometime this year seems unlikely.

The risk of a recession lies in 2023 or 2024. We do believe the risk has increased, hence the increase in duration and more conservative positioning within equities - but we don’t see it as our base case. Parts of the economy are still early in the recovery process, the labor market is very tight, and consumers and businesses have relatively strong balance sheets with plenty of cash. Still the economy will slow and we don’t know how far the Fed will go with monetary tightening. The Fed doesn’t know what they will do, they’ve been changing their guidance on almost a monthly basis. It is a bit disconcerting, but also a reflection of these unique times.

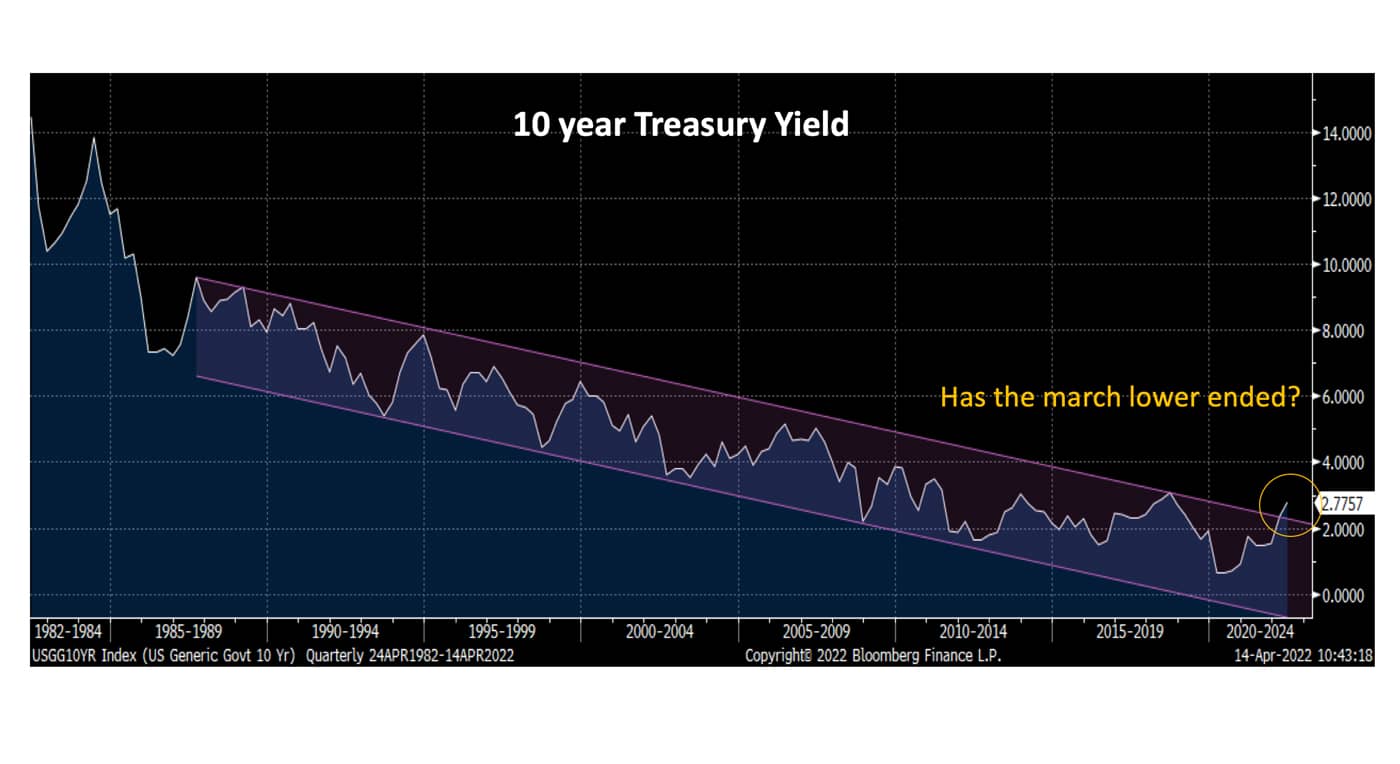

One last thought relates back to interest rates. It appears that we have broken a nearly 40 year downtrend. This may be simply a feature of the unique aspects of the pandemic, but we are hopeful that this trend break remains in place as it suggests that the longer term economic growth prospects have stopped falling. The main ingredients of economic growth are labor force growth and productivity. The prospects for labor force growth have not changed, but tight labor market conditions and rising input costs may advance the outlook for productivity growth. It is too soon to draw any conclusions, but we are seeing increased spending on labor saving equipment and software, and companies certainly have the cash and incentive to do more.

Glossary of Investment Terms and Index Definitions

This commentary is for informational purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security. There is no guarantee that the information is complete or timely. Past performance is no guarantee of future results. Investing in an index is not possible. Investing involves risk, including the possible loss of principal and fluctuation of value. Please visit touchstoneinvestments.com for performance information current to the most recent month-end.

Please consider the investment objectives, risks, charges and expenses of the fund carefully before investing. The prospectus and the summary prospectus contain this and other information about the Fund. To obtain a prospectus or a summary prospectus, contact your financial professional or download and/or request one on the resources section or call Touchstone at 800-638-8194. Please read the prospectus and/or summary prospectus carefully before investing.

Touchstone Funds are distributed by Touchstone Securities, Inc.

*A registered broker-dealer and member FINRA/SIPC.

Not FDIC Insured | No Bank Guarantee | May Lose Value