International Equities Monthly

- The U.S. Dollar Index recently moved modestly above the 97–100 trading range that had contained it for roughly a year. The breakout followed Chair Warsh’s first FOMC meeting, that was more hawkish than markets expected, leading investors to reassess the possibility of a rate hike. However, we do not view this as the beginning of a sustained new rally in the dollar.

- The U.S. 2-year Treasury yield moved modestly higher, but 2-year sovereign yields in Europe and the UK increased by slightly more. As a result, our DXY-weighted 2-year yield spread has rolled over, removing some of the interest-rate support behind the dollar’s initial move higher.

- The renewed hostilities surrounding the Strait of Hormuz are an unfortunate development and create additional near-term upward pressure on the dollar. The escalation also comes at a more precarious point in the energy cycle, with inventories at very low levels and less capacity to absorb another prolonged disruption. Iran continues to view control over the Strait as its primary source of leverage and appears unwilling to surrender it without meaningful concessions. That raises the risk that shipping disruptions persist, and oil prices move higher.

- Over the longer term, the structural backdrop for the dollar remains challenging. Large fiscal deficits, elevated policy uncertainty, higher valuation, gradual reserve diversification, and greater currency hedging by international investors continue to limit the case for a renewed secular bull market.

- Taken together, the dollar’s modest breakout deserves attention, particularly given renewed geopolitical risk. However, relative interest rate support is already fading, and we see little evidence that the structural headwinds facing the dollar have diminished. We therefore continue to view the dollar as more likely to remain near its recent range than begin a sustained advance toward its previous highs, preserving a supportive currency backdrop for U.S.-based investors in international equities.

- We remain neutral on developed international equities. The continuation of Middle East hostilities reintroduces an important macro headwind. Higher energy prices could again pressure inflation, interest rates, and corporate margins. While the geopolitical backdrop has become more uncertain, it also strengthens the case for an active approach rather than changing our overall allocation.

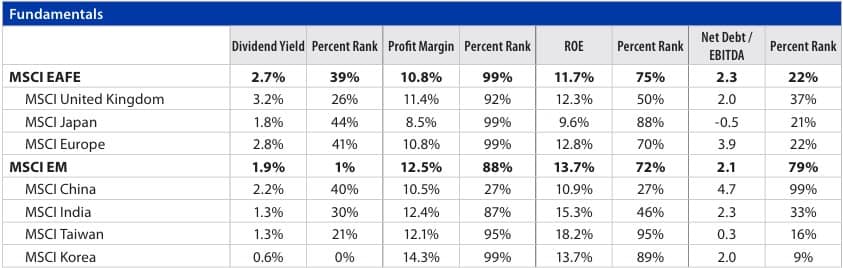

- Europe continues to present a mixed picture. Consensus expects another solid quarter of earnings growth, though roughly half is expected to come from Energy sector. That said, Europe still offers selective opportunities, particularly among companies benefiting from the global AI infrastructure build-out and industrial electrification trends.

- In Japan, beyond supplying semiconductor manufacturing equipment, companies are increasingly benefiting from broader AI-related investment in factory automation, robotics, industrial machinery, optical components, and digital infrastructure. Combined with a weaker yen and improving domestic economic conditions, these trends have supported broader earnings participation than we are currently seeing in Europe.

- The increasing divergence between Europe and Japan illustrates why active management matters. Developed international markets are being driven by distinct regional and company-specific factors rather than a single macro narrative, making stock selection and country allocation increasingly important. Developed international equities also complement U.S. portfolios. They provide exposure to different earnings drivers and secular growth themes than the increasingly concentrated U.S. market, helping diversify portfolio risk.

- While near-term geopolitical developments are likely to create periods of volatility, they do not alter our view that international equities remain an important component of a well-diversified portfolio.

- Emerging markets have a more nuanced picture. In late March, we tactically reduced our emerging market (EM) allocation to a slight underweight because we believed a prolonged disruption in the Strait of Hormuz would disproportionately affect many Asian economies that rely heavily on imported Middle Eastern energy. While those concerns remain relevant with the continuation of hostilities, the investment backdrop has changed meaningfully over the past month. While we are maintaining our current tactical positioning, the recent correction has made emerging markets increasingly worthy of another look.

- The MSCI EM index has declined roughly 10% over the last month (through July 20), while the S&P 500 has been essentially flat. Much of the weakness has been driven by just two Korean chip companies due to capacity expansion concerns. However, earnings estimate revisions continue to rise causing valuations to fall significantly.

- China presents a different story altogether. Economic growth continues to soften as property, consumer spending, and employment remain under pressure. At the same time, Beijing appears increasingly committed to supporting strategic industries such as semiconductors, AI, advanced manufacturing, and green technology rather than pursuing broad-based stimulus. The result is a "two speed" economy, where technology-related sectors continue to expand even as more traditional parts of the economy struggle. Recent market weakness, together with targeted policy support and state-backed equity purchases, suggests selective opportunities may be emerging for active managers despite the challenging macro backdrop.

- Taken together, we believe our tactical underweight is becoming less clear-cut than it was several months ago. The original macro headwinds from higher energy prices remain, particularly if hostilities in the Middle East persist. However, recent market weakness has already discounted some of those risks, while semiconductor valuations have become considerably more attractive.

- Today, returns are increasingly shaped by country-specific policy decisions, AI adoption, industrial specialization, and geopolitical developments. We believe active managers are better positioned to navigate these divergent trends than passive benchmark-based strategies.

Equity Indexes Characteristics

The Indexes mentioned are unmanaged statistical composites of stock market or bond market performance. Investing

in an index is not possible.

Glossary of Investment Terms and Index Definitions

*Local currency earnings estimates are not available for broad indexes with a mix of currencies.

Source: Bloomberg. Percent ranks are based on 30 years of monthly data as of the end of May; EPS growth estimates based on consensus

bottom-up analyst estimates.

The Touchstone Asset Allocation Committee

The Touchstone Asset Allocation Committee (TAAC) consisting of Crit Thomas, CFA, CAIA – Global Market Strategist, Erik M. Aarts, CIMA – Vice President and Senior Fixed Income Strategist, and Tim Paulin, CFA – Senior Vice President, Investment Research and Product Management, develops in-depth asset allocation guidance using established and evolving methodologies, inputs and analysis and communicates its methods, findings and guidance to stakeholders. TAAC uses different approaches in its development of Strategic Allocation and Tactical Allocation that are designed to add value for financial professionals and their clients. TAAC meets regularly to assess market conditions and conducts deep dive analyses on specific asset classes which are delivered via the Asset Allocation Summary document. Please contact your Touchstone representative or call 800.638.8194 for more information.

A Word About Risk

Investing in equities is subject to market volatility and loss. Investing in foreign and emerging markets securities carry the associated risks of economic and political instability, market liquidity, currency volatility and accounting standards that differ from those of U.S. markets and may offer less protection to investors. The risks associated with investing in foreign markets are magnified in emerging markets due to their smaller economies. Events in the U.S. and global financial markets, including actions taken to stimulate or stabilize economic growth may at times result in unusually high market volatility, which could negatively impact asset class performance. Banks and financial services companies could suffer losses if interest rates rise or economic conditions deteriorate.

Performance data quoted represents past performance, which is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than performance data given. For performance information current to the most recent month-end, visit TouchstoneInvestments.com/mutual-funds.

Please consider the investment objectives, risks, charges and expenses of the fund carefully before investing. The prospectus and the summary prospectus contain this and other information about the Fund. To obtain a prospectus or a summary prospectus, contact your financial professional or download and/or request one on the resources section or call Touchstone at 800-638-8194. Please read the prospectus and/or summary prospectus carefully before investing.

Touchstone Funds are distributed by Touchstone Securities, LLC.*

*A registered broker-dealer and member FINRA/SIPC.

Touchstone is a member of Western & Southern Financial Group

Not FDIC Insured | No Bank Guarantee | May Lose Value