- Organizations with excess cash may benefit from proper liquidity management by partnering with the team at Fort Washington to better manage this process and potentially realize the value of cash segmentation to increase interest income.

- Basel III and the return to a ZIRP (zero interest rate policy) environment has changed the landscape for liquidity management dramatically.

- Understanding cash segmentation can help organizations properly balance risk, return, and liquidity.

- Active cash management requires effective and regular communication with clients, a key tenet of Fort Washington’s Liquidity Management Strategy.

- By thoroughly understanding liquidity needs and properly segmenting cash, investment income can be increased materially.

Using current yield levels for various liquidity instruments, we have demonstrated how a basic cash segmentation strategy could result in additional interest income in this hypothetical example:

| Basic Cash Strategy | Purpose | Assets | Yield | $ Income |

|---|---|---|---|---|

| Prime Money Market Fund | Sweep | 50,000,000 | 0.15% | $75,000 |

| Cash Segmentation Strategy | Purpose | Assets | Yield | $ Income |

|---|---|---|---|---|

| Prime Money Market Fund | Operating Cash: Daily Liquidity | 20,000,000 | 0.15% | $30,000 |

| Enhanced Cash | Tactical Cash: Monthly Liquidity | 10,000,000 | 0.24% | $24,000 |

| Ultra Short Duration | Strategic Cash: 6-12+ Months | 20,000,000 | 1.15% | $230,000 |

| Total | Optimized Cash Strategy | 50,000,000 | 0.57% | $284,000 |

| Difference | 0.42% | $209,000 |

Source: Fort Washington. The above hypothetical is being presented for illustrative purposes only, and represents an example of cash management strategies and allocations. Actual allocations, yield, and income will be different from those shown, depending on current market and economic conditions, and client-specific needs. Yield shown does not reflect a single source, but was approximated using a variety of average yield calculations and representative portfolio holdings as of August 2020. Income shown does not take into consideration any account fees and expenses that may be incurred with the management of a similar strategy. Past performance is not indicative of future results.

Basel III Implications

Balancing Liquidity, Risk, and Reward

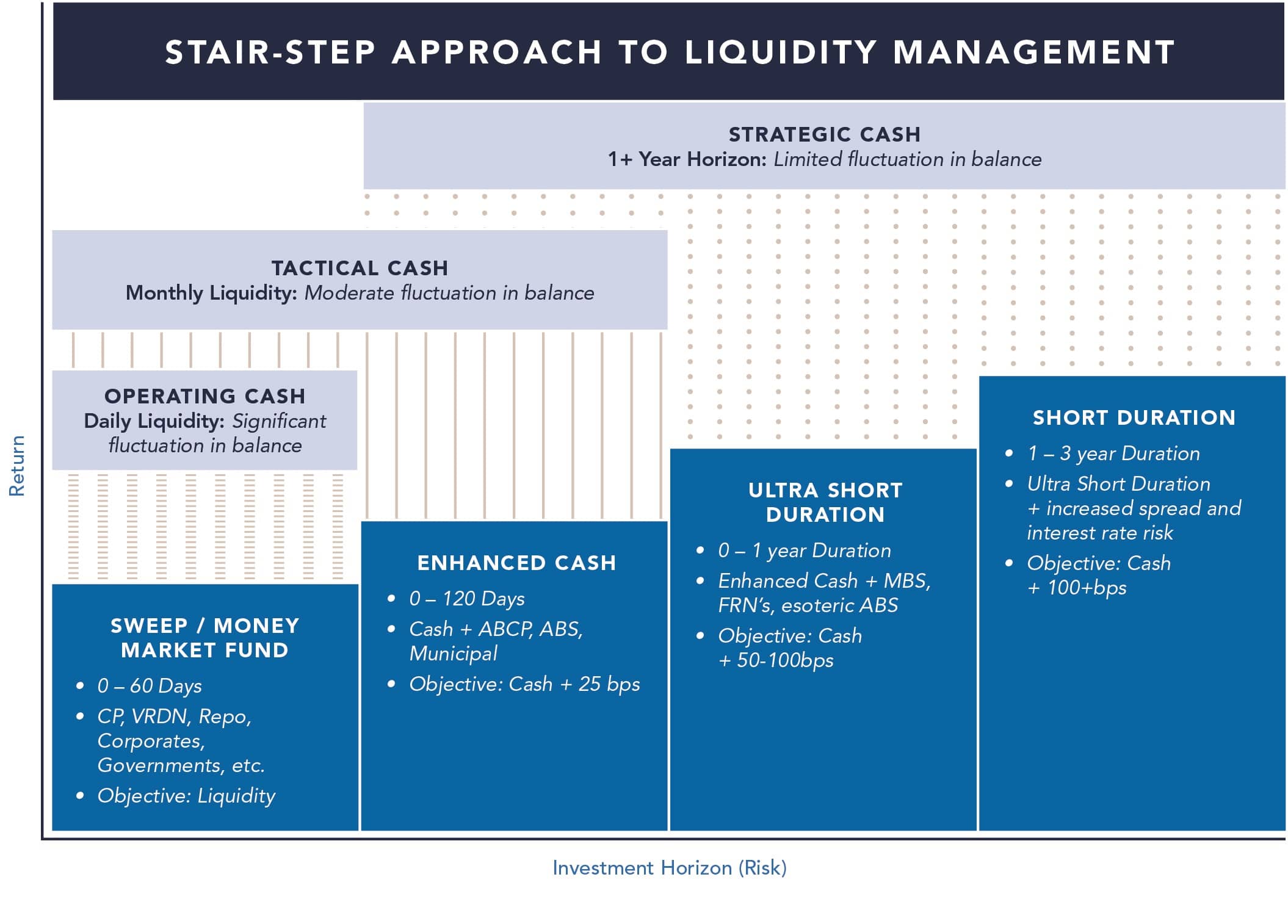

Figure 2: Stair-Step Approach to Liquidity Management

Source: Fort Washington. ABCP: Asset-Backed Commercial Paper, ABS: Asset-Backed Security, CP: Commercial Paper, FRN: Floating-Rate Note, MBS: Mortgage-Backed Security, Repo: Repurchase Agreement, VRDN: Variable Rate Demand Note.

Source: Fort Washington. ABCP: Asset-Backed Commercial Paper, ABS: Asset-Backed Security, CP: Commercial Paper, FRN: Floating-Rate Note, MBS: Mortgage-Backed Security, Repo: Repurchase Agreement, VRDN: Variable Rate Demand Note.Partnering with Clients

The Fed adopted a zero interest rate policy (ZIRP) in March 2020, effectively driving money market rates close to zero. Investors are once again forced to focus on an asset class that is often overlooked, similar to the last ZIRP environment from 2009-2015. Although the fundamentals of liquidity management have not changed, the investment landscape has changed dramatically. By having a thorough understanding of our clients’ liquidity needs and risk tolerance, as well as a deep knowledge of cash segmentation strategies, Fort Washington’s Liquidity Management team can structure an optimized portfolio aimed at generating a meaningful additional return on cash investments.

A key tenet of Fort Washington’s Liquidity Management Strategy is effective and regular communication with clients. This allows us to gain a thorough understanding of clients’ cash needs and how these needs may change on a real-time basis. In fact, many clients view our strategy to be accretive to their internal treasury function.

With this construct, we are able to work toward optimizing returns while providing proper liquidity management, adhering to policy constraints and risk tolerances with preservation of capital as an overriding goal. The process may be summarized as follows:

- Investment Horizon/Liquidity Ladder

- Analyze historical cash balances to determine confidence intervals fora maximum downside scenario

- Apply knowledge of the cash segmentation “stair step” to develop a liquidity plan

- Immunize known cash flows

- Risk Tolerance

- Determine universe of investable assets and create an Investment Policy Statement (IPS) to govern liquidity, credit quality, diversification, maturity, and other risk drivers.

- Risk Management

- Utilize best-in-class third-party systems and proprietary tools for compliance and risk monitoring

What is Your Optimal Liquidity Solution?

Each investor's needs and objectives are unique. A prudent investor understands all investment objectives, keeps current with the market environment, and stays abreast of dynamic and changing investment options. By having a thorough understanding of a client’s liquidity needs and properly segmenting cash, significant value can typically be added through a proper liquidity solution.

Why Fort Washington?

Fort Washington adds value through unparalleled customer service. Our liquidity management team strives for strong ongoing communication in order to manage expectations as they relate to client risk tolerance, investment returns, and investment policy statement construction and compliance. We recognize that liquidity and safety of principal are paramount when managing cash and want to help clients become comfortable with the agreed upon levels of portfolio risk and return.

We believe actively managing cash can allow organizations to tailor liquidity needs while optimizing returns. If your organization is not optimizing cash balances and failing to benefit from additional income that can be earned with a cash segmentation strategy, we hope you will contact our team at Fort Washington to better manage this process and realize the benefits of active liquidity management.