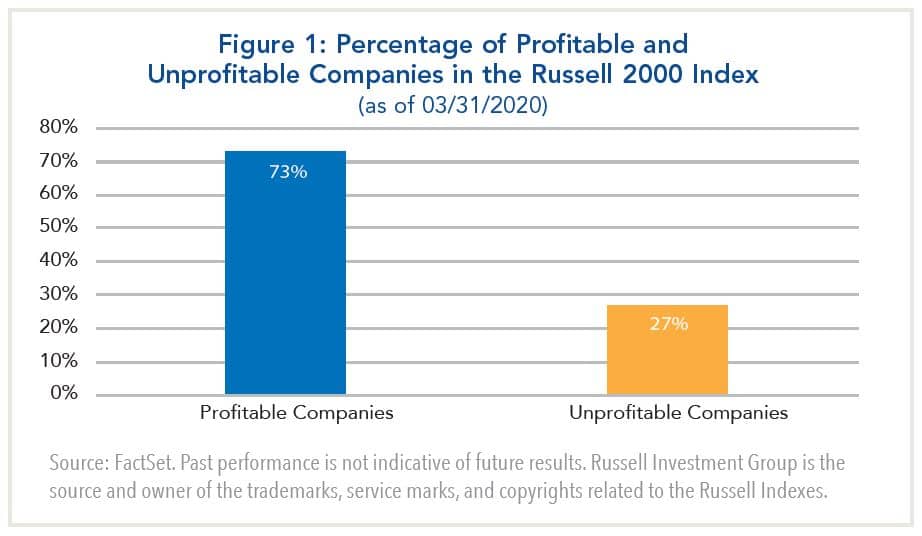

Small capitalization, or “small cap,” stocks have generated attractive investment returns over the long term. In fact, dating back to 1926, U.S. small cap stocks have produced annualized total returns of 11.90%, compared to 10.14% for U.S. large cap stocks, and 5.5% for U.S. government bonds. There are several reasons small cap stocks outperform, including higher levels of long-term earnings growth and greater research inefficiencies due to a smaller number of “buy-side” and “sell-side” investors focused in the small cap spectrum of the market due to liquidity. Small cap stocks also outperform over time because they are inherently a riskier asset class. Looking closer at the U.S. small cap asset class, one of the reasons they are riskier and more volatile is the percentage of unprofitable companies in the asset class. As of March 31, 2020, about 27% of companies within the Russell 2000 Index were unprofitable.

The Russell 2000 Index is a widely used small cap benchmark. In fact, many exchange-traded funds (ETF’s) and passive mutual funds with a significant amount of assets mirror this market-cap weighted benchmark. Many investors might believe a passive ETF or mutual fund is “safer,” not realizing the high level of exposure to unprofitable companies. A successful active manager will dig deeper to find the most promising small cap stocks with strong business models that exhibit growth, profitability, and free cash flow generation that allows them compound returns over time.

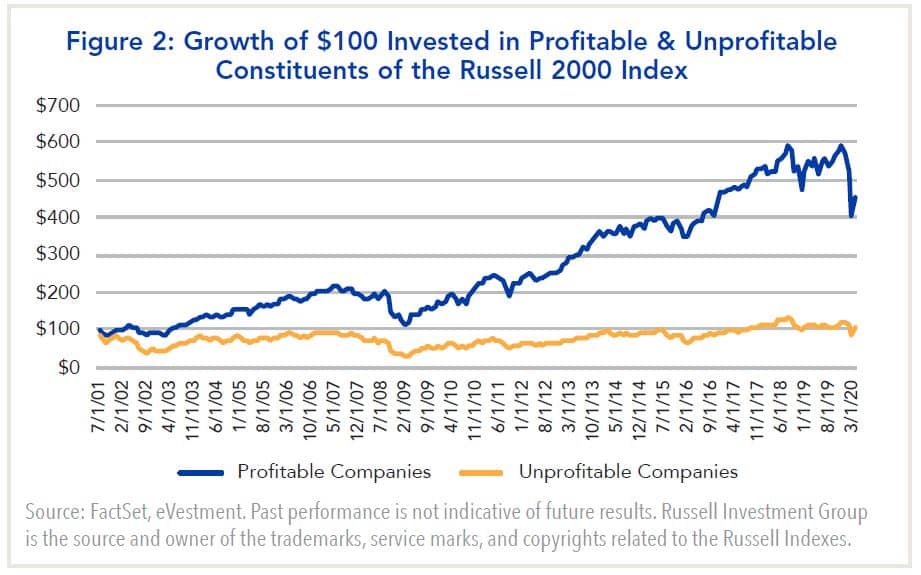

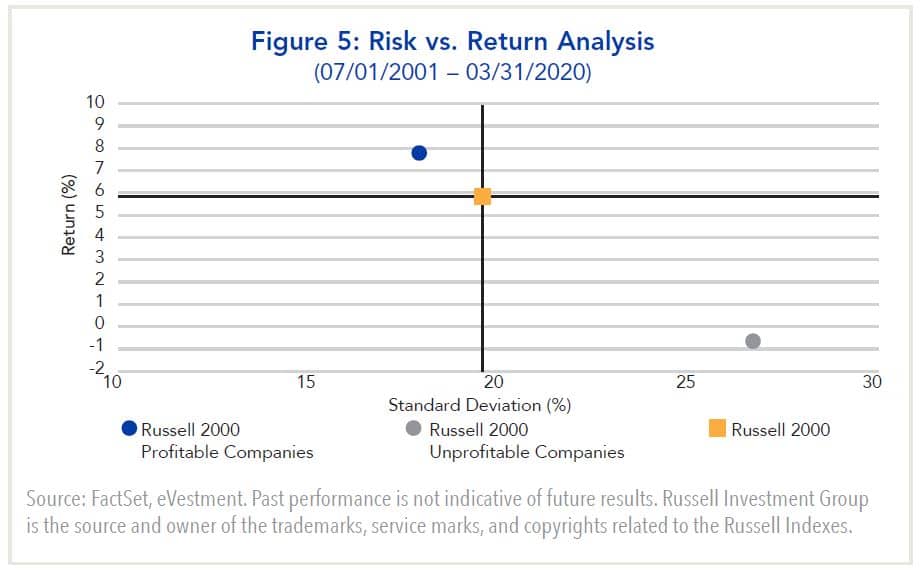

The Fort Washington Small Company Equity strategy only invests in profitable small cap stocks. This is one of the key tenets of our investment philosophy. Avoiding unprofitable small cap stocks reduces the risk levels of investing in small cap stocks. Furthermore, and most importantly, profitable small cap stocks outperform unprofitable small cap stocks with significantly lower volatility. The chart below illustrates the performance of the profitable and unprofitable constituents of the Russell 2000 Index since July 2001.

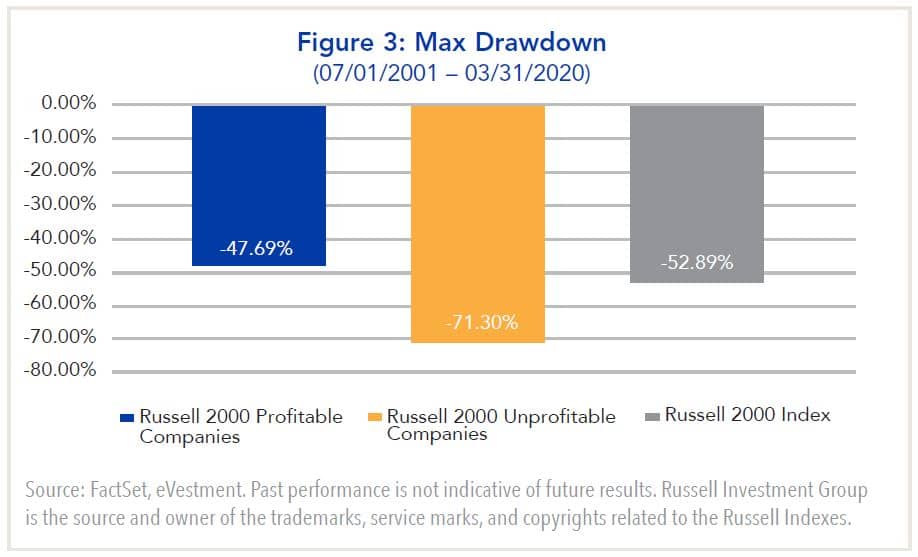

There are a few reasons why profitable small cap stocks outperform over time. First, they generally do not require access to capital to fund their operations. During an economic downturn or any period where the cost of capital is increasing, unprofitable stocks are at a significant disadvantage. Unprofitable small cap stocks have going-concern or bankruptcy risk in recessions. Another reason is that profitable small cap companies can internally invest in future growth, compounding earnings growth over time, which is ultimately what drives long-term stock returns. Profitability provides flexibility to manage through economic slowdowns and recessions. The chart below illustrates the maximum drawdown risk between profitable and unprofitable stocks in the Russell 2000 Index.

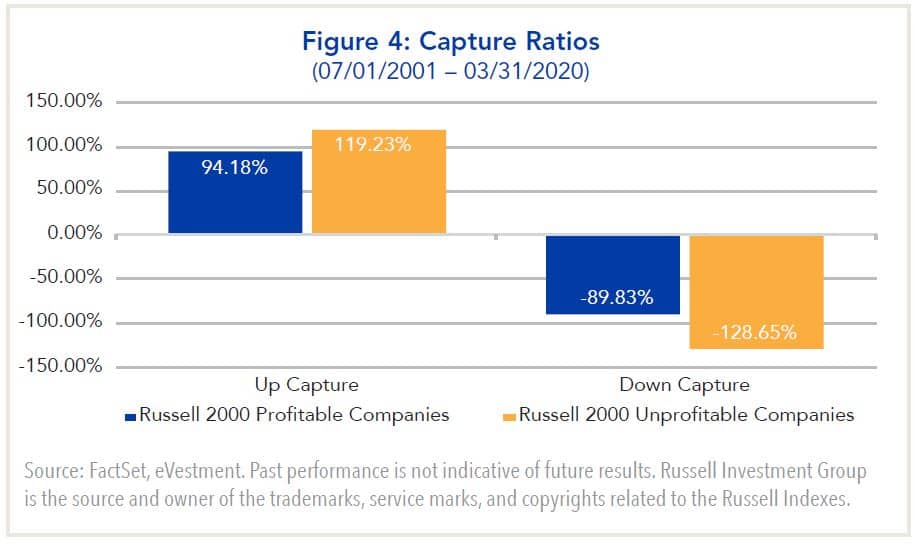

Profitable stocks significantly outperform unprofitable stocks in more challenging economic environments, and they also perform very well in robust bull markets. The chart below illustrates the Up Capture Ratio and Down Capture Ratio for profitable and unprofitable small cap stocks over the period. These up and down capture ratios show whether the strategy has outperformed—meaning gained more or lost less than—its benchmark during periods of market strength and weakness, and if so, by how much.

When combining the favorable long-term outperformance and lower volatility characteristic of profitable small cap stocks, there is a very favorable reward compared to risk for investing in the profitable spectrum of the U.S. small cap asset class.

The Russell 2000 Index is a widely used small cap benchmark. In fact, many exchange-traded funds (ETF’s) and passive mutual funds with a significant amount of assets mirror this market-cap weighted benchmark. Many investors might believe a passive ETF or mutual fund is “safer,” not realizing the high level of exposure to unprofitable companies. A successful active manager will dig deeper to find the most promising small cap stocks with strong business models that exhibit growth, profitability, and free cash flow generation that allows them compound returns over time.

The Fort Washington Small Company Equity strategy only invests in profitable small cap stocks. This is one of the key tenets of our investment philosophy. Avoiding unprofitable small cap stocks reduces the risk levels of investing in small cap stocks. Furthermore, and most importantly, profitable small cap stocks outperform unprofitable small cap stocks with significantly lower volatility. The chart below illustrates the performance of the profitable and unprofitable constituents of the Russell 2000 Index since July 2001.

There are a few reasons why profitable small cap stocks outperform over time. First, they generally do not require access to capital to fund their operations. During an economic downturn or any period where the cost of capital is increasing, unprofitable stocks are at a significant disadvantage. Unprofitable small cap stocks have going-concern or bankruptcy risk in recessions. Another reason is that profitable small cap companies can internally invest in future growth, compounding earnings growth over time, which is ultimately what drives long-term stock returns. Profitability provides flexibility to manage through economic slowdowns and recessions. The chart below illustrates the maximum drawdown risk between profitable and unprofitable stocks in the Russell 2000 Index.

Profitable stocks significantly outperform unprofitable stocks in more challenging economic environments, and they also perform very well in robust bull markets. The chart below illustrates the Up Capture Ratio and Down Capture Ratio for profitable and unprofitable small cap stocks over the period. These up and down capture ratios show whether the strategy has outperformed—meaning gained more or lost less than—its benchmark during periods of market strength and weakness, and if so, by how much.

When combining the favorable long-term outperformance and lower volatility characteristic of profitable small cap stocks, there is a very favorable reward compared to risk for investing in the profitable spectrum of the U.S. small cap asset class.