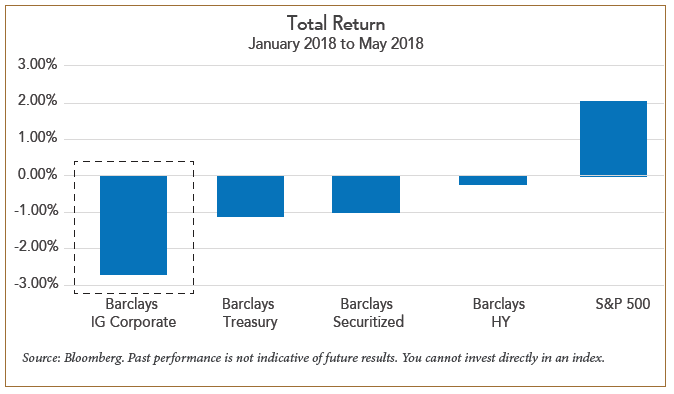

From Unloved...

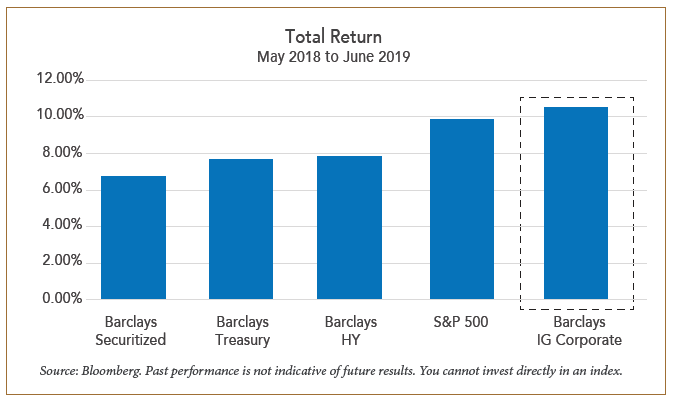

As we noted at the time, however, the prospects for investment grade corporates were compelling. We found 7 to 10 year bonds particularly attractive given their combination of overall yield, a steep credit curve, and the potential for price appreciation on lower treasury yields and tighter spreads. One year later, investment grade corporates have not only generated strong absolute returns of more than 10%, but they have also outperformed both equities and other fixed income sectors on a relative basis.

...To Beloved

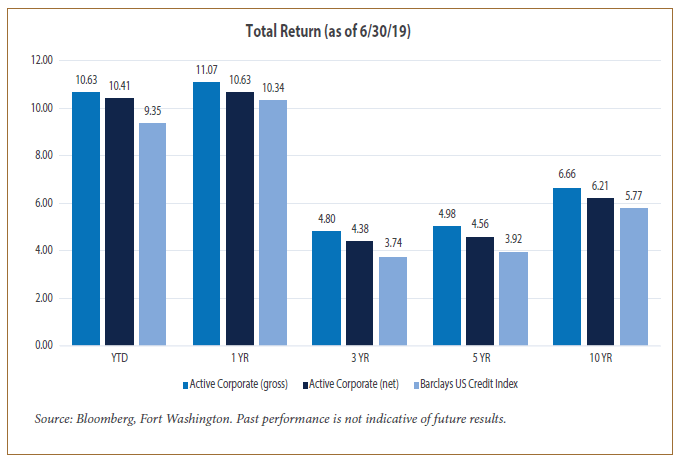

During this period, Fort Washington’s Active Corporate strategy was well positioned to outperform the market through a combination of strong bottom-up security selection and a tactical overweight to the 7-10 year part of the curve. Additionally, this performance has enhanced the strategy’s longer-term performance, which has consistently outperformed the benchmark over 1, 3, 5, and 10 year periods.

We attribute this long-term outperformance across multiple market environments to three key tenets of Fort Washington’s Active Corporate strategy. Specifically, we believe in:

- Active Management: Fixed income index construction is inherently inefficient and disadvantageous to investors. An actively managed portfolio can take advantage of these inefficiencies and generate consistent alpha.

- Bottom-up Security Selection: Market inefficiencies are best exploited through fundamental research and bottom-up security selection rather than top-down, macro driven bets. The large number and wide variety of inputs needed to forecast macro outcomes can make it difficult to consistently generate alpha via macro-driven bets. Individual companies have relatively fewer drivers and are more easily analyzed, making them a more consistent avenue for generating alpha.

- Duration/Curve Neutrality: For the same reasons that consistent forecasting of other macro outcomes is difficult, accurate prediction of interest rate movements is rare. As such, active interest rate bets should be limited in favor of active positioning in individual issuers.

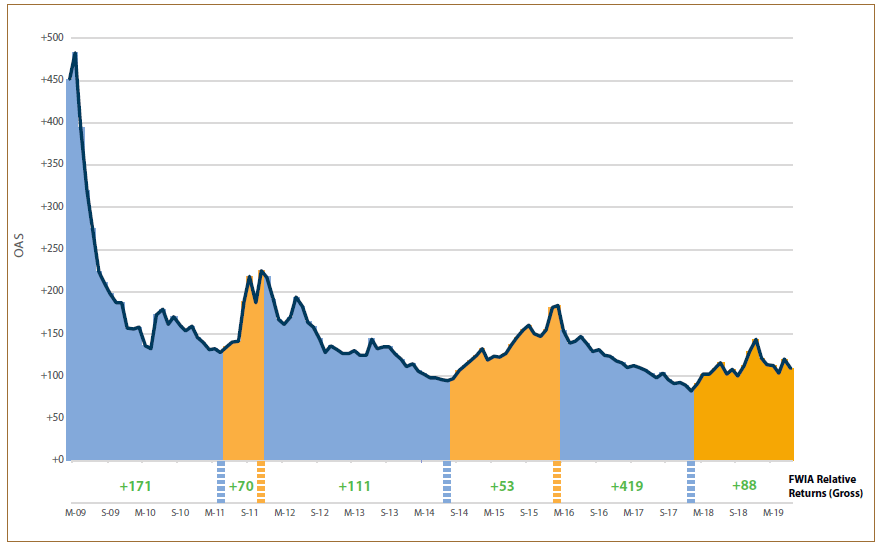

Source: Bloomberg. The chart represents the Bloomberg Barclays US Credit Index OAS. For illustrative purposes only. Past performance is not indicative of future results. Returns are presented gross of fees for illustrative purposes only and do not reflect the deduction of advisory fees. Returns will be reduced by the advisory fees and other expenses. For example, an advisory fee of 1% compounded over a 10-year period would reduce a 10% annual return to 8.9%. Past performance is not indicative of future results. M=March, S=September.

Source: Bloomberg. The chart represents the Bloomberg Barclays US Credit Index OAS. For illustrative purposes only. Past performance is not indicative of future results. Returns are presented gross of fees for illustrative purposes only and do not reflect the deduction of advisory fees. Returns will be reduced by the advisory fees and other expenses. For example, an advisory fee of 1% compounded over a 10-year period would reduce a 10% annual return to 8.9%. Past performance is not indicative of future results. M=March, S=September.

What Does the Remainder of 2019 Hold?

After the strong performance of the past 12 months, the corporate market holds somewhat limited appeal for investors focused on absolute yield and total return. The yield of the Barclays US Credit Index closed the month of June at 3.10%, the lowest levels since late 2017, implying that corporate bonds will likely need a combination of continued low inflation, dovish Federal Reserve policy, and stable credit spreads to earn a total return greater than 3%.

It is during this type of low expected return environment when the benefits of active management are typically most relevant. Despite the less favorable rate and spread backdrop, our bottom-up research is still uncovering attractive investment opportunities in individual issuers that can offer above-market yield and the potential for issuer specific spread tightening. The current portfolio has a yield 45 basis points above that of the benchmark while maintaining a risk target of 40-70% of our maximum risk budget. In a market of 3% yields, we believe this 45 basis point yield advantage is significant.

Our team is finding attractive bottom up opportunities, particularly in BBB-rated credits within defensive industries. This has led us to be overweight risk in defensive sectors such as consumer staples, utilities, and REITs, with more cautious positioning in cyclical sectors like metals, energy, autos, and emerging market sovereign debt.

| Active corporate composite | bloomberg barclays u.s. credit | |

|---|---|---|

| Effective Duration | 7.34 years | 7.39 years |

| Yield to Worst | 3.55% | 3.09% |

| OAS | 149 | 109 |

| Average Quality | A3 / BAA1 | A2 / A3 |

Conclusion

With the first half of 2019 providing a 6 month return that is among the best of the past 30 years, the risk of investor complacency is high. As corporate bonds investors have seen several times in the past 10 years, the market can quickly shift to “risk off” without the economy falling into a recession. We believe that active management of credit risk through bottom-up focused security selection will offer the best opportunity for long-term outperformance regardless of the macroeconomic environment.