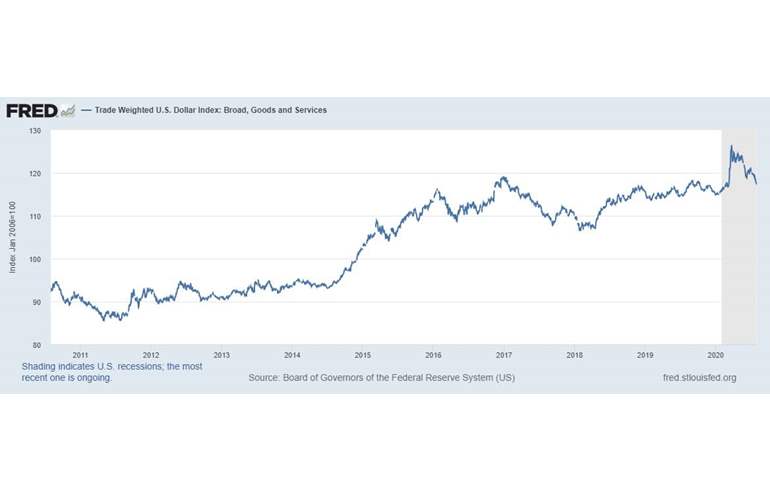

Views about U.S. financial markets are mostly upbeat this year as investors anticipate a return to normalcy in economic conditions by the second half as COVID-19 vaccines become widely disseminated. The outlier is the U.S. dollar, where most forecasts call for continued weakness following a 12% decline on a trade-weighted basis since last spring.

Source: Federal Reserve Bank of St. Louis. For informational purposes only.

The dollar’s turn last year coincided with the Federal Reserve lowering the federal funds rate to zero while expanding its toolkit to deal with the COVID-19 pandemic. In the process the Fed’s balance sheet expanded from $4 trillion to more than $7 trillion. Pressures on the dollar then gained traction in summer when the Fed announced changes in its framework for conducting monetary policy.

Specifically, the Fed announced that it would henceforth target an average annual inflation rate of 2%. Fed officials also signaled they will not raise rates preemptively as long as labor is not fully utilized as judged by a broad array of measures.

Investors have interpreted these actions as implying the Fed is willing to risk – and even to encourage -- higher inflation. This means implicitly that real interest rates will stay abnormally low and possibly negative for the next year or two.

Beyond this, the most bearish forecasts see a potential dollar crisis owing to record federal budget deficits and persistent large U.S. trade deficits.

Economist Stephen Roach of Yale University, for example, has warned that a low U.S. net national savings rate increases the risk of dollar crash. He sees outsized budget deficits spawning trade deficits that make the U.S. heavily reliant on foreign financing. At some point, international investors could become reluctant to hold an increasing supply of dollars.

However, there are several shortcomings with the “twin deficit” argument.

First, it previously applied to a context in which U.S. inflation was high relative to its major trading partners such as occurred in the 1970s and 1980s. Yet, U.S. inflation has been in line with that of other industrial countries for the past three decades.

During that period, the U.S. has run large trade and budget deficits, but there has not been a dollar crisis of note. The reason: The Fed is perceived to be a credible inflation fighter, and most investors believe it would react if inflation moved much beyond its 2% average threshold.

Second, although U.S. interest rates are near record lows, the vast majority of European government bond yields are negative. The prognosis, moreover, is they are likely to stay below U.S. yields for a long while. The reason: European economies have been hit even harder by the COVID-19 pandemic than the U.S. and there is a greater threat of deflation. Accordingly, the European Central Bank is contemplating easing monetary policy further.

The most likely outcome in my view is the dollar will stabilize against the euro, and it may appreciate against it later this year. One reason is the yield spread between U.S. and European bonds is likely to widen in favor of the dollar as the U.S. economy gains traction.

Another consideration is the euro’s appreciation over the past year means it is no longer cheap relative to the dollar. At the current price near $1.22, the euro is slightly above its average level since its inception.

I also look for the dollar to stabilize against the renminbi (RMB) albeit for different reasons than for the euro. The principal reason is the Chinese authorities are likely to intervene in the foreign exchange market to resist further appreciation of the RMB. The RMB already has appreciated by nearly 14% versus the dollar, and the authorities are concerned that a further rise would undermine China’s competitiveness.

During 2018, the RMB weakened by about that amount, when the Trump administration imposed tariffs of 25% on Chinese goods that are imported into the U.S. This meant that China was able to maintain much of its competitiveness with the U.S. However, if the Biden administration leaves the tariffs in place, as seems likely, China’s exports to the U.S. could slow in the future due to the appreciation of the RMB. Accordingly, China’s central bank is reluctant to raise interest rates as the economy recovers from the COVID-19 pandemic.

Another consideration that works in favor of the dollar is the Chinese authorities are unlikely to open its financial markets so that capital can flow freely into and out of the country. This means there is little risk that the U.S. dollar will lose its stature as the world’s reserve currency.

In the end, the dollar’s performance should largely be dictated by how quickly the U.S. economy returns to normal. Even if recovery is delayed, any softening of the dollar is likely to be benign.

A version of this article was posted to Forbes.com on February 1, 2021.