Some commentators have dismissed the results as a statistical fluke owing to seasonal adjustments and benchmark revisions. Normally, payrolls drop by about 3 million in the survey taken between mid-December and mid-January, as many businesses close for the holidays and winter weather often impacts construction activity. This year, however, the raw payroll account declined by about 2.5 million and the seasonal adjustment added the standard 3 million to the adjusted tally. Consequently, some of the reported gains could be reversed in the next job report.

Estimates for the January report were well below the actual results partly because of news reports of large layoffs at leading technology companies. However, the tech sector accounts for only 4% of total employments, and net job losses in the sector tallied only 5,000.

Demand for Labor Is Strong Despite a Slowing Economy…

Looking at the employment data over the past year, what stands out is there have been broad-based gains in services (see Figure 1.) Leisure and hospitality, health care, and professional and business services led the way, accounting for almost one-half of the overall gain in private sector jobs. This suggests that businesses impacted by the COVID-19 pandemic are gearing up, now that the worst is over.

The manufacturing sector has also added more than 400,000 new jobs since the beginning of 2021. One reason is that as businesses were impacted by supply-chain disruptions they have brought capabilities onshore that had been sent abroad.

The manufacturing sector has also added more than 400,000 new jobs since the beginning of 2021. One reason is that as businesses were impacted by supply-chain disruptions they have brought capabilities onshore that had been sent abroad.Further indication of the strong job market is the latest Job Opening and Labor Turnover Survey (JOLTS) that showed job openings rose to 11 million in December from 10.4 million in November. With 6 million people currently unemployed, there are now more than 1.8 openings for each job seeker. Before the pandemic struck in March of 2020, the ratio was 1.2 openings per unemployed person in an already tight labor market.

…While the Labor Force Has Expanded

One explanation is that this group is now feeling the pinch of higher inflation squeezing their real income, as well as increased uncertainty about the economic outlook.

After the pandemic hit, roughly 4 million workers dropped out of the labor force. They included people who were close to retirement age and opted to take early retirement and those who were concerned about COVID-19 exposure.

In addition, many people received generous transfer payments from the federal government and were able to save a significant portion of the proceeds, while they also reduced spending on items such as restaurants and travel. According to Moody’s Analytics, U.S. households amassed $2.7 trillion in extra savings by the end of 2021.

Faced with this predicament and the prospect of the economy slipping into recession, some workers who opted out of the workforce are now returning.

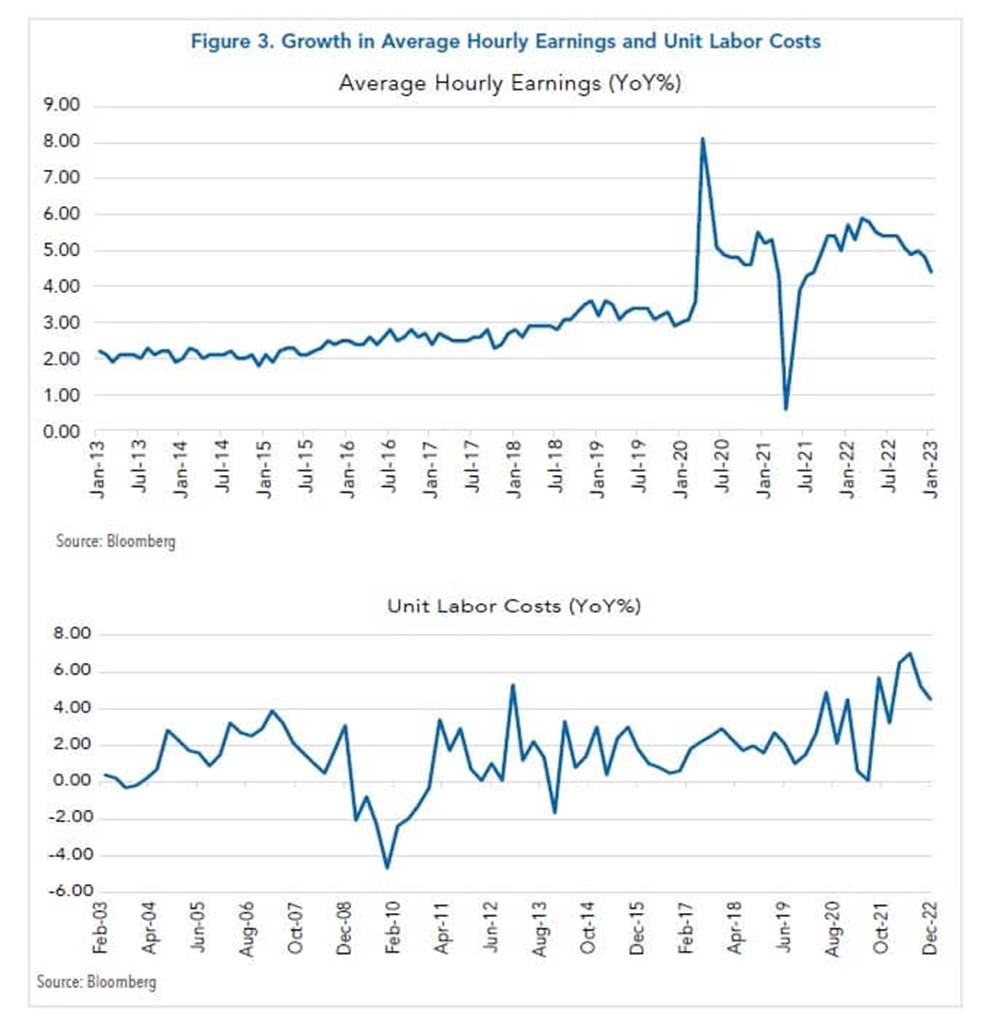

Wage Increases Show Signs of Moderating

With the number of job openings still plentiful, one might expect wage pressures to continue to build. However, there are indications that they are moderating. The year-over-year increase in average hourly earnings, for example, has recently slowed to about 4.5%, down from 6% in mid-2022, and it has been accompanied by a slowing in unit labor costs (Figure 3).

This suggests that new entrants into the job market have less bargaining power, as many of the positions being filled are for entry-level work or have low skill requirements.

This increases the likelihood that inflation will continue to slow this year and next. Most of the slowing thus far is the result of goods prices falling as supply disruptions have eased. Looking ahead, the rent component is also expected to ease as home prices and mortgage rates have eased.

How the Fed Is Likely to Respond

For his part, Fed chair Jerome Powell has indicated that the battle to bring inflation back toward the 2% target is ongoing and will take considerable time to achieve. Although wages are not the cause of higher inflation, the tight labor market is an impediment to a quick drop in core inflation.

Looking ahead, one of the challenges for the Fed is how it will respond if the economy slips into a mild recession. In this regard, it is important to keep in mind that the Fed’s dual mandate is to seek both price stability and full employment. With unemployment now at a five-decade low and inflation at a four-decade high, investors should not expect the Fed to lower rates unless there is a significant rise in unemployment and decline in inflation.