- Last year was full of surprises, but two are particularly noteworthy: (i) The COVID-19 pandemic was not brought under control; and (ii) U.S. bond yields were remarkably steady even as inflation spiked to a three decade high.

- Looking ahead, the worst of the pandemic may be over before long, but we are uncertain that inflation will recede materially. That said, markets appear confident the Federal Reserve will win the battle over inflation.

- Meanwhile, we continue to overweight risk assets in investment portfolios because the economic outlook is favorable. However, we are prepared to reduce risk if inflation stays elevated and the Fed tightens more than expected.

Key Issues for Investors

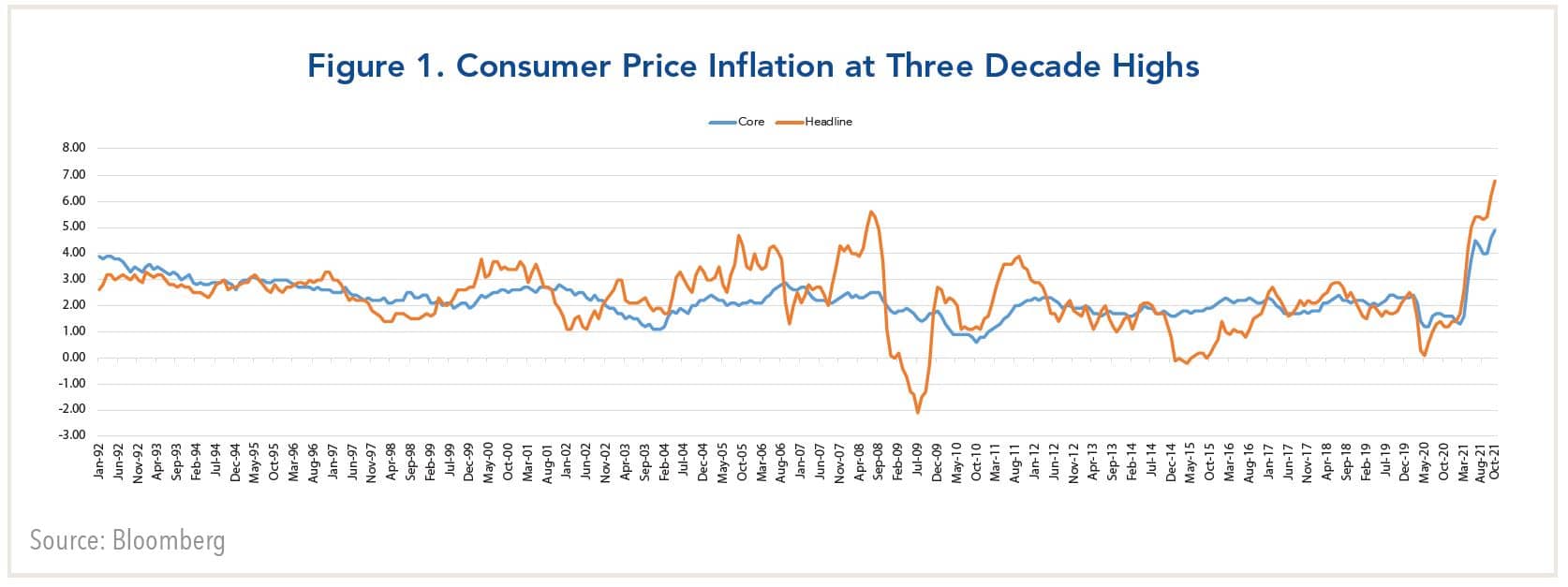

One year ago, the consensus view among forecasters was that the U.S. economy would return to normal and bond yields would approach pre-pandemic levels. Instead, reining in coronavirus proved to be a more difficult task due to the emergence of the Delta and Omicron strains and the reluctance of many Americans to become vaccinated. Also, while Treasury yields surged in the first quarter, yields subsequently settled into a trading range and closed the year around 1.5% for 10-year Treasuries. This occurred even though inflation surged to a three decade high (Figure 1).

On the political front, one of the main uncertainties was how much of President Biden’s ambitious legislative agenda would be enacted considering that Democrats controlled Congress by the narrowest of margins. By year’s end, the Build Back Better plan was still up in the air, although the administration succeeded in passing a $1.9 trillion COVID relief package and a $1.2 trillion infrastructure bill. The Biden administration, however, did not overturn the tax provisions in the Tax Cut and Jobs Act enacted in the Trump administration.

Amid this, risk assets continued to garner stellar returns (Figure 2). During 2021, the S&P 500 Index posted a total return of 28.7%, while returns for the NASDAQ composite and Russell 2000 Index were 22.2% and 14.8%, respectively. U.S. equity markets have now doubled in value from their lows in March of 2020, far outpacing other developed markets (EAFE) and emerging markets. Similarly, corporate bonds—both investment grade and high yield—have outperformed Treasuries considerably.

Amid this, risk assets continued to garner stellar returns (Figure 2). During 2021, the S&P 500 Index posted a total return of 28.7%, while returns for the NASDAQ composite and Russell 2000 Index were 22.2% and 14.8%, respectively. U.S. equity markets have now doubled in value from their lows in March of 2020, far outpacing other developed markets (EAFE) and emerging markets. Similarly, corporate bonds—both investment grade and high yield—have outperformed Treasuries considerably.

| STOCK MARKET | 2021 | Mar. 31, 2020 - Dec. 30, 2021 |

|---|---|---|

| U.S. (S&P 500) | 28.68 | 89.48 |

| NASDAQ | 22.21 | 105.91 |

| Russell 2000 | 14.78 | 98.43 |

| International (EAFE $) | 11.86 | 56.93 |

| Emerging Markets (MSCI $) | -2.51 | 51.57 |

| U.S. BOND MARKET | 2021 | Mar. 31, 2020 - Dec. 30, 2021 |

|---|---|---|

| Treasuries | -2.32 | -2.50 |

| IG Credit | -1.08 | 11.68 |

| High Yield | 5.28 | 29.15 |

| MSCI EM | -2.29 | 41.41 |

Source: Bloomberg. For informational purposes only. Frank Russell Company (FRC) is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and copyrights related thereto. The presentation may contain confidential information pertaining to FRC and unauthorized use, disclosure, copying, dissemination, or redistribution is strictly prohibited. This is a Fort Washington Investment Advisors, Inc. presentation of the Russell Index data. Frank Russell Company is not responsible for the formatting or configuration of this material or for any inaccuracy in Fort Washington’s presentation thereof. You cannot invest directly in an index.

Looking ahead, the key issues are similar to last year’s. Namely, will the coronavirus pandemic finally be reined in? How will bond yields fare as the Federal Reserve tightens monetary policy? Also, will risk assets continue to outperform?

When Will the Pandemic Become Endemic?

Of these issues, the hardest to forecast is how the coronavirus pandemic will play out. On the Fourth of July, President Biden confidently declared that the United States had achieved “independence” from COVID-19. Instead, cases have surged since then as a result of the Delta variant and more recently the rapid spread of the Omicron variant, although deaths have not spiked thus far.

As 2022 begins, epidemiologists are forecasting that cases will continue to spike in January. The good news is that many experts also believe coronavirus will become endemic over time. This means that while the virus will continue circulating around the world for years, its prevalence and impact will abate to manageable levels such that it winds up more like the flu than a virulent global disease.

One criterion for an infectious disease to be classified as endemic is that the rate of infections (and hospitalizations) stabilize over time. While we clearly aren’t there yet, the rapid spike in Omicron infections is building population-level immunity in addition to those who are vaccinated and have received booster shots. The big unknown, of course, is whether new strains will surface that will be resistant to existing vaccines.

As 2022 begins, epidemiologists are forecasting that cases will continue to spike in January. The good news is that many experts also believe coronavirus will become endemic over time. This means that while the virus will continue circulating around the world for years, its prevalence and impact will abate to manageable levels such that it winds up more like the flu than a virulent global disease.

One criterion for an infectious disease to be classified as endemic is that the rate of infections (and hospitalizations) stabilize over time. While we clearly aren’t there yet, the rapid spike in Omicron infections is building population-level immunity in addition to those who are vaccinated and have received booster shots. The big unknown, of course, is whether new strains will surface that will be resistant to existing vaccines.

Impact on the Economy and Monetary Policy

Regarding the economic impact, one of the main lessons from the Delta variant is that it did not produce lasting damage because businesses and schools remained open. Fed Chair Jerome Powell told lawmakers the economic effect of the Omicron variant would not be “remotely comparable” to what occurred during the onset of the pandemic. By the same token, it could influence monetary policy if the economy were to slow materially.

At the December FOMC meeting, the Fed announced it would accelerate its tapering of bond purchases to conclude in March 2022, and it increased the projections for the federal funds rate. The median forecast of FOMC members now calls for three rate hikes in both 2022 and 2023, with a terminal rate of 2%-2 ¼% by 2024. Subsequently, the minutes from the meeting revealed that some officials are concerned that inflation is becoming entrenched. Market participants now believe the Fed could begin to raise rates in March and that it could begin to shrink its balance sheet while it raises rates.

The looming issue is whether this gradual glide path of rate increases will be sufficient to bring inflation back to the Fed’s average annual target of 2%.

There are several reasons to be skeptical. First, the median projections of Fed members for the coming year call for real GDP growth of 4% and the unemployment rate to fall to 3.5%. If realized, they suggest the economy will be approaching its long-term potential before long. Second, inflation expectations are becoming embedded in wages, which have risen steadily and are now approaching 4% as the jobs market has tightened. Third, while supply chain disruptions may ease as the coronavirus pandemic abates, the housing component of the CPI is likely to stay elevated.

Meanwhile, economic policies are highly accommodative as indicated by financial market conditions that are the easiest on record (see Figure 3). With inflation in the vicinity of 4%-5%, interest rates are decidedly negative in real terms, which has helped boost stock prices to record levels.

With respect to fiscal policy, the surge in the federal budget deficit to record levels in the past two years is about to end as COVID-relief winds down. Nonetheless, according to the Congressional Budget Office, the deficit will stay relatively high in the vicinity of 4.5% of GDP in the current fiscal year. Moreover, CBO’s forecast does not take into account the impact of the $1.2 trillion infrastructure bill that was enacted (over 10 years) or the $2 trillion BBB plan that could still be enacted. Accordingly, federal spending is expected to stay high while transfer payments to households diminish.

At the December FOMC meeting, the Fed announced it would accelerate its tapering of bond purchases to conclude in March 2022, and it increased the projections for the federal funds rate. The median forecast of FOMC members now calls for three rate hikes in both 2022 and 2023, with a terminal rate of 2%-2 ¼% by 2024. Subsequently, the minutes from the meeting revealed that some officials are concerned that inflation is becoming entrenched. Market participants now believe the Fed could begin to raise rates in March and that it could begin to shrink its balance sheet while it raises rates.

The looming issue is whether this gradual glide path of rate increases will be sufficient to bring inflation back to the Fed’s average annual target of 2%.

There are several reasons to be skeptical. First, the median projections of Fed members for the coming year call for real GDP growth of 4% and the unemployment rate to fall to 3.5%. If realized, they suggest the economy will be approaching its long-term potential before long. Second, inflation expectations are becoming embedded in wages, which have risen steadily and are now approaching 4% as the jobs market has tightened. Third, while supply chain disruptions may ease as the coronavirus pandemic abates, the housing component of the CPI is likely to stay elevated.

Meanwhile, economic policies are highly accommodative as indicated by financial market conditions that are the easiest on record (see Figure 3). With inflation in the vicinity of 4%-5%, interest rates are decidedly negative in real terms, which has helped boost stock prices to record levels.

With respect to fiscal policy, the surge in the federal budget deficit to record levels in the past two years is about to end as COVID-relief winds down. Nonetheless, according to the Congressional Budget Office, the deficit will stay relatively high in the vicinity of 4.5% of GDP in the current fiscal year. Moreover, CBO’s forecast does not take into account the impact of the $1.2 trillion infrastructure bill that was enacted (over 10 years) or the $2 trillion BBB plan that could still be enacted. Accordingly, federal spending is expected to stay high while transfer payments to households diminish.

Markets Currently Side with the Fed

For the time being, financial markets concur with the Fed’s assessment of the economic outlook and its interest rate trajectory. Amid all of the angst over inflation, one of the big surprises is that gold prices fell last year. Similarly, two other widely-followed market indicators—the shape of the Treasury yield curve and the tradeweighted value of the U.S. dollar—suggest investors have confidence the Fed will keep inflation under control.

Historically, the shape of the Treasury yield curve has been considered one of the best indicators of economic activity. If investors thought the Fed was behind the curve, the Treasury curve would normally steepen, with long-term yields rising by more than short-term rates. Instead, the shape of the yield curve has changed very little over the past year as it shifted higher. (Figure 4).

The same applies to the U.S. dollar. If investors believed the Fed was behind the curve the dollar would normally weaken, whereas it appreciated by 3.5% on a trade weighted basis over the past year. The primary reason is interest rate differentials favor the dollar, and the Fed is expected to raise interest rates this year while the European Central Bank and the Bank of Japan are on hold and the People’s Bank of China may ease rates. As a result, international investors continue to view the dollar as a safe haven.

The same applies to the U.S. dollar. If investors believed the Fed was behind the curve the dollar would normally weaken, whereas it appreciated by 3.5% on a trade weighted basis over the past year. The primary reason is interest rate differentials favor the dollar, and the Fed is expected to raise interest rates this year while the European Central Bank and the Bank of Japan are on hold and the People’s Bank of China may ease rates. As a result, international investors continue to view the dollar as a safe haven.

So, why are investors unfazed by the spike in inflation?

One explanation is that investors’ expectations about inflation and interest rates have been shaped by the experience following the 2008 Global Financial Crisis (GFC), when economic growth and inflation were subdued for a decade. The coronavirus pandemic, however, is a completely different type of shock that did not inflict lasting damage on the economy and the financial system. Throughout the travail, what stands out is many U.S. companies are highly adaptable and experienced increased productivity while others have seen their businesses disrupted. Therefore, one should not expect the same outcome as occurred after the GFC.

Historically, the shape of the Treasury yield curve has been considered one of the best indicators of economic activity. If investors thought the Fed was behind the curve, the Treasury curve would normally steepen, with long-term yields rising by more than short-term rates. Instead, the shape of the yield curve has changed very little over the past year as it shifted higher. (Figure 4).

The same applies to the U.S. dollar. If investors believed the Fed was behind the curve the dollar would normally weaken, whereas it appreciated by 3.5% on a trade weighted basis over the past year. The primary reason is interest rate differentials favor the dollar, and the Fed is expected to raise interest rates this year while the European Central Bank and the Bank of Japan are on hold and the People’s Bank of China may ease rates. As a result, international investors continue to view the dollar as a safe haven.So, why are investors unfazed by the spike in inflation?

One explanation is that investors’ expectations about inflation and interest rates have been shaped by the experience following the 2008 Global Financial Crisis (GFC), when economic growth and inflation were subdued for a decade. The coronavirus pandemic, however, is a completely different type of shock that did not inflict lasting damage on the economy and the financial system. Throughout the travail, what stands out is many U.S. companies are highly adaptable and experienced increased productivity while others have seen their businesses disrupted. Therefore, one should not expect the same outcome as occurred after the GFC.

Investors Foresee a Benign Environment

With the economy and corporate profits having recovered from the shutdowns when the pandemic spread globally in early 2020, the U.S. stock market has posted outsized returns since then that far exceed most international markets. To a large extent, the gains last year reflected a strong rebound in corporate profits, with earnings for S&P 500 companies up by about 35%. Going forward, Wall Street analysts are forecasting profit growth for S&P 500 companies in the vicinity of 10%. Therefore, investors should lower their return expectations after outsized results in the past two years.

How well the stock market performs will also hinge to a large extent on how inflation fares. If it recedes as the Fed expects and interest rate increases are gradual, valuations are likely to remain high. However, should inflation prove to be persistent and the Fed is compelled to accelerate the pace of rate hikes, the stock market would likely become vulnerable.

Accordingly, we are currently maintaining moderate overweight positions in risk assets in investment portfolios. But, we are also prepared to alter our strategy if it becomes evident that the rate hikes the Fed is currently projecting are too modest to bring inflation under control.

How well the stock market performs will also hinge to a large extent on how inflation fares. If it recedes as the Fed expects and interest rate increases are gradual, valuations are likely to remain high. However, should inflation prove to be persistent and the Fed is compelled to accelerate the pace of rate hikes, the stock market would likely become vulnerable.

Accordingly, we are currently maintaining moderate overweight positions in risk assets in investment portfolios. But, we are also prepared to alter our strategy if it becomes evident that the rate hikes the Fed is currently projecting are too modest to bring inflation under control.