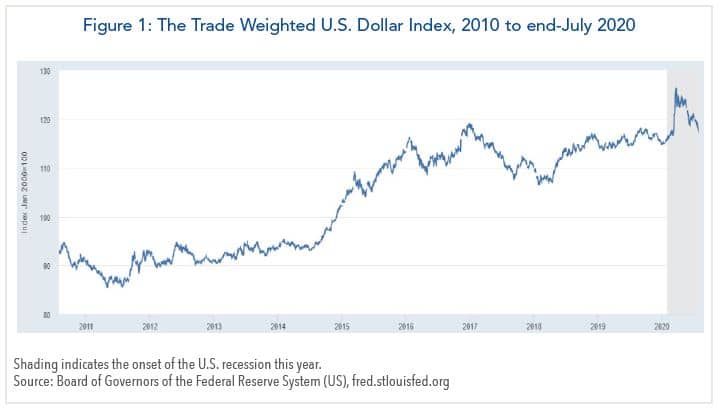

- After rising by nearly 40% throughout the past decade, the U.S. dollar has come under pressure since late March declining by about 6% on a trade-weighted basis. The weakening is linked to accommodative U.S. monetary and fiscal policies to combat the COVID-19 pandemic.

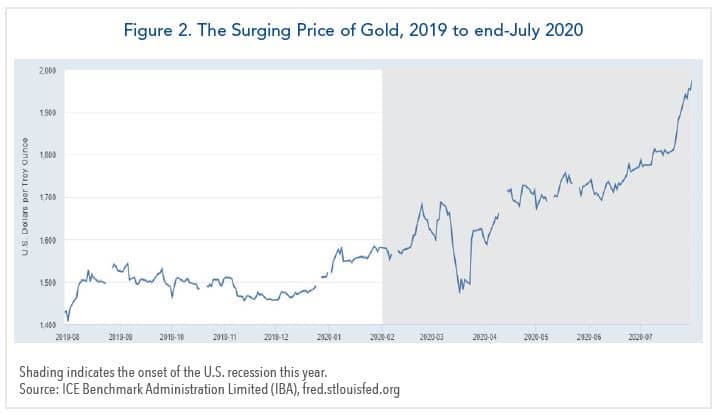

- The dollar’s softening has also coincided with a surge in the price of gold to a record high. However, the U.S. bond market is not signaling a quick resurgence of U.S. inflation.

- The dollar is likely to remain under pressure for the balance of this year and into next year. However, a full-blown loss of confidence is unlikely and the dollar’s status as the world’s reserve currency is not likely in question.

Background: The Turn in the Dollar

The U.S. dollar had a remarkable run over the past decade, rising by 38% on a trade-weighted basis (Figure 1) amid the longest U.S. economic expansion on record. The dollar’s trade-weighted appreciation in this period was shy of its 45% rise in the second half of the 1990s but lasted twice as long.

Most of the dollar’s rise occurred from 2015 when the euro was severely strained and China experienced a growth slowdown. Investors were attracted to it by relatively favorable U.S. economic performance and positive interest rate differentials versus the euro-zone, where interest rates eventually became negative.

The dollar’s strength lasted until the first quarter of this year when the U.S. economic expansion was aborted by the COVID-19 pandemic. The turning point in late March coincided with unprecedented U.S. policy actions to combat the effects of social distancing and shutdowns of U.S. businesses.

The dollar’s strength lasted until the first quarter of this year when the U.S. economic expansion was aborted by the COVID-19 pandemic. The turning point in late March coincided with unprecedented U.S. policy actions to combat the effects of social distancing and shutdowns of U.S. businesses.

For its part, the Federal Reserve quickly lowered interest rates to zero and augmented bond-buying programs it launched during the 2008 financial crisis. Pressures on the dollar subsequently intensified after the June FOMC meeting, when Chairman Jerome Powell emphasized that “We’re not thinking about raising rates. We’re not even thinking about thinking about raising rates.”

Meanwhile, investors are awaiting Congressional action to bolster the economy and lower unemployment. Federal programs enacted to tackle the pandemic currently tally $3.3 trillion and according to the Congressional Budget Office will boost the federal deficit by $2.5 trillion. Democrats favor additional programs totaling $3 trillion while Republicans initially opposed legislation that exceeded $1 trillion. A compromise bill is expected to be enacted shortly that will boost the federal deficit further.

Surge in the Price of Gold

Thus far, there is little to indicate that inflation or inflation expectations have increased materially. Treasury bond yields, for example, are at or near record lows, and inflation expectations as measured by the spread in Treasury yields versus Treasury Inflation Protected bonds (TIPs) are also low, running at about 1.5%.

Much of the appeal of gold is it is perceived to be a hedge during times of economic strain and heightened uncertainty. Considering that there is no prior experience of a pandemic in the post-war era, investors view gold as a safe haven either if inflation accelerates or if deflation adds to financial strains.