- The post-election rally in equities and other risk assets continued in the first two months of this year but paused in March when the House Republicans could not agree on a replacement for Obamacare.

- For the time being, businesses and consumers are optimistic about the U.S. economy’s prospects, but so-called soft data (sentiment) has not yet translated into accelerated growth as reflected in hard (quantifiable) data. With jobs growth solid and core inflation near 2%, the Fed is likely to continue raising interest rates gradually.

- Looking ahead, markets will be fixated on pending tax legislation for businesses and households. Whereas House Republican leaders favor tax reform that is deficit neutral, President Trump campaigned on implementing a big tax cut for the middle class. It’s too early to gauge the outcome, but tax cuts are normally easier to pass than cuts in deductions. Amid this uncertainty we expect market volatility to increase from unusually low levels.

- With the economy on solid footing, we are still comfortable overweighting risk assets relative to treasuries in fixed-income portfolios. We are also upgrading quality in equity portfolios while maintaining normal cash holdings.

The “Trump Trade” Fades

Following President Trump’s surprise victory on November 8, investors responded by buying equities and other risk assets, while treasury yields and the dollar surged. As this pattern continued into 2017, the so-called “Trump trade” became synonymous with rising stocks, higher bond yields, and a stronger dollar. It was mainly driven by expectations that the pro-growth strategy of the Trump Administration would succeed in restoring economic growth of 3% or more.

This optimism helped boost the U.S. stock market to record highs in the first two months of this year, when U.S. equities posted returns of 13%-19% from the November election. During March, however, the stock market surrendered some of its gains, when the House Republicans failed to reach agreement on legislation that would replace the Affordable Care Act, commonly known as “Obamacare.”

The healthcare outcome was a great disappointment for both the President and House Speaker Paul Ryan, as one of the over-riding themes of the GOP during the campaign was the repeal of Obamacare. Moreover, the specter of the Freedom Caucus blocking passage of the House Republican bill raised doubts for the first time about whether the Trump Administration and Republican-controlled Congress would be able to enact legislation on tax reform and infrastructure spending.

While the fading of the Trump rally is linked to the vote on healthcare, investors were beginning to hedge their bets even before the vote. The stock market rally last year, for example, was led by small-cap value stocks; however, they have lagged large-cap growth stocks so far this year (see Figure 1). Meantime, Treasury bond yields remain well above their levels prior to the election, while the dollar has surrendered all of its gains since the election.

Figure 1: Investment Results Post Election & First Quarter of 2017

| nov. 18, 2016 - mar. 31, 2017 | Q1 2017 | |

|---|---|---|

| Dow Jones | 13.8% | 4.6% |

| S&P 500 | 11.3% | 5.5% |

| Russell 2000 | 16.6% | 2.1% |

| U.S. Treasuries | -2.0% | 0.7% |

| IC Credit | -0.7% | 1.3% |

| High Yield | 4.5% | 2.7% |

| US Trade Weighted Dollar | 1.1% | -3.1% |

*Includes dividends except for Emerging Markets, which is price change. Source: Bloomberg.

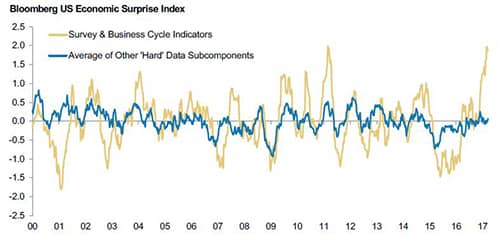

Economic News: “Hard” Versus “Soft Data”

One of the most unusual aspects of the current situation is the stark contrast between indicators that reflect sentiment about the economy – so called “soft data” — and those that measure the actual performance — called “hard data.” The huge divergence in the two sets of data are shown in the accompanying chart.

Figure 2: “Soft” versus “Hard” Economic Data

Source: Bloomberg, Morgan Stanley Research.

Based on survey data, it would appear the economy is booming. Consumer confidence, for example, surged to a 16-year high in a Conference Board poll that was taken before the healthcare vote. Similarly, the survey of small businesses showed one of the largest boosts in confidence readings shortly after the election. Other indicators including the ISM indices for the manufacturing and services sectors also have increased noticeably.

Thus far, this optimism on the part of households and businesses has not translated into stronger economic growth. The economy ended 2016 with a 2% growth rate, which was in line with the trend rate since the economic expansion began in mid-2009. Estimates for the first quarter of this year range from 1% to 2% annualized, which partly reflects an inventory drawdown that is likely to be reversed in the second quarter. Meanwhile, business spending has remained lackluster despite the optimism expressed by executives, and auto sales have sagged after a banner year in 2016.

One indicator that suggests the economy is on solid footing is jobs growth, which has averaged close to 200,000 people over the past six months. This has resulted in the unemployment rate falling to 4.7%, its lowest level since the expansion began in mid-2009. It has been accompanied by a gradual rise in wages and inflation, which is now at the Fed’s target of 2% for core inflation. Accordingly, the Fed responded by raising the funds rate by a quarter point to 0.75%-1.0% at its March meeting — the third such increase since it began to tighten policy at the end of 2015. Fed officials, moreover, have signaled they are prepared to take further gradual rate hikes in the remainder of this year, and the bond market is anticipating the funds rate will end the year at 1.25%-1.5%.

An encouraging development is that for the first time since the start of this decade the global economy is experiencing a synchronized expansion, which should further buttress the U.S. economy. Worries about a marked slowdown in China’s economy that were prevalent one year ago have faded, as the pace of economic activity improved in the second half of the year owing to the combination of monetary policy easing and fiscal stimulus. The upturn in China’s economy, in turn, has bolstered emerging economies, which are suppliers of raw materials to China.

At the same time, the European Union (EU) has emerged from its slump, with Germany leading the way. Britain’s economy has also proved resilient in the wake of the Brexit vote last year, largely due to the sharp depreciation of the pound, which has boosted the country’s competitiveness. The principal concerns are on the political front, where France, Germany, and Italy face important elections.

All told, we expect a gradual strengthening of the U.S. economy this year, with real GDP growth likely to be slightly above the 2% trend rate for the expansion. However, in order for the economy to achieve and to sustain growth of 3% or more, investors are anticipating meaningful changes in the tax code for businesses and households will take place later this year.

Tax Reform or Tax Cuts?

During the election campaign both Donald Trump and House Speaker Ryan emphasized the need to implement changes in tax legislation in order to restore long-term trend growth of at least 3%. Beyond this commitment, however, there are notable differences in the strategy the Republican House leadership is pursuing and that of the President: Specifically, the former are seeking to implement comprehensive tax reform that will be deficit neutral, whereas President Trump wishes to fulfill his campaign pledges of “massive tax relief for the middle class” and no cutbacks in entitlement programs.

Prior to the vote on healthcare, market participants paid considerable attention to the legislation that the House Republican leadership drafted last summer, as it embodied reforms to the tax code the GOP had embraced for two decades. With respect to the corporate sector, the key provisions included the following: (i) lowering the marginal corporate tax rate from 35% to 20% (versus 15% favored by President Trump); (ii) immediate deduction of expenses on capital outlays, but no interest rate deduction; (iii) incentives for U.S. companies to repatriate profits from abroad; and (iv) a border adjustment tax (BAT) that would effectively subsidize exports and tax imports.

Of these, the most controversial is the BAT, which has attracted considerable opposition from companies whose business models are dependent on global supply chains. Whereas Speaker Ryan favors the provision, partly because it is estimated to generate government revenues of more than one trillion dollars over a decade, President Trump has stated that it is too complex, and he favors a simpler approach of taxing imports.

Prior to the fiasco over healthcare, market participants believed there was a one in three chance the BAT would be included in the final legislation. Now the odds appear considerably lower, as both the President and Republican leadership in Congress cannot risk another legislative defeat. The challenge the Republicans face in that event, however, is that the failure to replace Obamacare means that the current program of expanding Medicaid remains in effect, and it is estimated to cost an additional one trillion dollars in the coming decade. Hence, the combined loss of revenues from failure to repeal Obamacare and from excluding the BAT in the tax bill would be on the order of two trillion dollars. (Note: The Republican plan to replace Obamacare also contained tax reductions such that CBO estimated the budgetary savings to be on the order of $350 billion.)

The goal of achieving meaningful tax reform that is deficit neutral, therefore, appears increasingly difficult, if not impossible. In addition, the President and Congressional Republicans must agree on tax cuts for individuals. The biggest difference in the two approaches is the House Republican plan would broaden the tax base by eliminating most personal deductions, whereas the Trump campaign tax plan would do far less to broaden the tax base.

The bottom line is that while the President and House Republican leadership are committed to lower corporate and personal tax rates, they are far apart in how to pay for the tax cuts while also funding increased spending on the military and infrastructure. According to President Trump, the problem will take care of itself, as tax cuts will spur economic growth and revenues will follow suit. However, the same was said during the Reagan Administration, when “supply side” tax cuts were combined with spending increases and the budget deficit rose to then record levels. At that time, moreover, demographics were favorable as the retirement expenses associated with baby boomers were decades away. Today, by comparison, boomers already are retiring and in the absence of policy changes the Congressional Budget Office anticipates significant increases in the federal budget deficit relative to GDP in the next two decades.

Market Uncertainties Are Bound to Increase

Thus far, market participants have adopted a “wait and see” approach, and volatility in financial markets has stayed surprisingly low even in the face of the healthcare fiasco and political problems the President is facing. While the presumption appears to be that tax reform will prove easier to enact than healthcare reform, the reality is that it is always easier for politicians to agree on giveaways to the public than on takeaways. Therefore, we believe the odds favor passage of tax cuts for corporations and individuals rather than tax reform.

In that event, the Republican Congressional leadership will face the following dilemma: Should they scale back the magnitude of corporate tax rate cuts, say to 25%-28%, which would disappoint equity investors? Or, should they stick with a 20% tax rate and allow the budget deficit to grow significantly over time, which would likely result in higher bond yields?

One possibility is that failure to reach an agreement could result in tax legislation being delayed until 2018. In that event, the Trump rally would likely suffer a major blow, as it would raise questions about the ability of President Trump and the Republican Party to govern. At this juncture, however, it is too early to be confident about the outcome.

Investment Implications

Weighing these considerations, we are mindful about policy uncertainty in the United States and political uncertainty in Europe, especially with upcoming elections in France, Germany, and Italy that carry important implications for the European Union. Therefore, we recognize that market volatility is likely to increase in the balance of this year.

At the same time, the weight of evidence suggests the U.S. economy and those abroad are experiencing the first synchronized expansion since the start of this decade. Financial conditions also remain favorable for growth and risk assets, even with the Federal Reserve raising interest rates.

Accordingly, we are continuing to maintain overweight positions in corporate bonds — both investment grade and high yield — relative to treasuries in fixed income portfolios. With respect to U.S. equities our view is that valuations do not leave a significant margin for safety. Therefore, we continue to upgrade the overall portfolio quality while maintaining normal cash holdings.