President Biden’s $1.9 trillion COVID stimulus plan has been greeted enthusiastically by investors as the U.S. stock market has set record highs. The attitude of many appears to be “the more stimulus, the better.” The reason: They see stronger economic growth boosting corporate profits.

Several prominent economists, however, have noted that U.S. budget deficits have now reached levels associated with a wartime economy. If this persists, their concern is the U.S. economy could overheat at some point and generate higher inflation and interest rates.

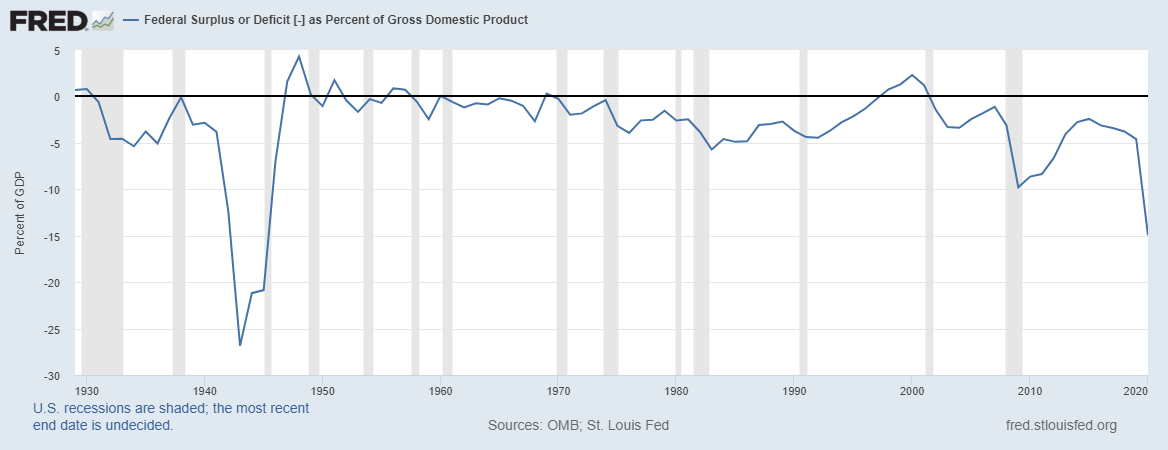

Source: Federal Reserve Bank of St. Louis. Chart is showing the Federal Budget deficit as a percent of GDP.

Source: Federal Reserve Bank of St. Louis. Chart is showing the Federal Budget deficit as a percent of GDP.

This view is enunciated in detail by Michael Bordo and Mickey Levy, who have studied the relationship between expansionary fiscal policies and inflation for over two centuries. Following the 2008-09 Global Financial Crisis (GFC) many investors concluded expansionary policies did not lead to inflation and the apparent link had been severed. The standard explanation is Federal Reserve actions to increase its balance sheet generated excess reserves in the banking system that were never put to work.

Bordo and Levy note that a key difference today is the money supply has surged as a result of excess saving associated with COVID transfer payments. They believe Biden’s plan will generate additional excess saving. Meanwhile, the surge in federal debt outstanding has created a situation of “fiscal dominance” in which the Fed is compelled to keep interest rates low for the foreseeable future to keep the government’s debt service costs manageable.

This perspective is not limited to fiscal conservatives: Former Treasury Secretary Lawrence Summers, who argued the federal response to the GFC was too small, claims the opposite is true today.

Summers notes that the $800 billion package enacted in 2009 offset only one half of the output shortfall then. By comparison, he estimates the $1.9 trillion plan along with the prior $900 billion relief package in December is three times the size of the output shortfall this year. Accordingly, one risk he sees is “macroeconomic stimulus on a scale closer to World War II levels than normal recession levels will set off inflationary pressures of a kind we have not seen in a generation.”

Some economists, however, are not convinced. Jim Glassman of J.P. Morgan Chase argues context matters (Weekly Insights on Markets & the Economy, February 8). He contends the current economic weakness is fundamentally different from traditional business cycles. Shutdowns of businesses during the onset of the COVID pandemic resulted in the steepest decline in output in the post-war era, and federal assistance provided a necessary lifeline to the economy. Glassman argues the assistance then has been spent, and he sees safety valves that should keep inflation contained. The safety valves include: (i) unemployment compensation likely will decline as the economy improves; (ii) globalization likely will temper inflation pressures and (iii) the Federal Reserve likely will normalize its posture as the economy approaches full employment.

My own take is the threat of inflation is not imminent with both core and headline CPI only at 1.4% over the last 12 months and the U.S. economy operating well below its potential. However, the economy will likely be much stronger in the second half of this year when COVID vaccines allow businesses to reopen and the impact of increased federal spending is felt. By year’s end, it should be near where it would have been before COVID struck.

Normally, such an outcome would be associated with rising bond yields. The increase to date has been muted due to uncertainty about how quickly COVID vaccines will be disseminated. The yield curve has steepened somewhat, however, and this is likely to continue in the second half. One reason is inflation expectations may edge higher as the economy strengthens. Another is real (inflation-adjusted) yields are likely to turn positive at some point.

As the economy approaches its potential, the outlook for inflation will largely be dictated by how the Federal Reserve responds.

The implicit assumption of those who see higher inflation is the Fed will be slow to react, as was the case in the late 1960s. They point to the change in the Fed’s policy framework to target an average inflation rate of 2% per annum. This means the Fed is prepared to allow an overshoot above that level when the target is not met. The big unknown is by how much and how long an overshoot will be tolerated.

By comparison, those who believe inflation will be contained think the Fed will act in time to maintain its credibility as an inflation fighter. After the Fed battled to bring inflation under control in the 1980s, they do not believe it will allow inflation to gain a foothold now.

My own take is the Fed has earned its stripes as an inflation fighter and is not likely to risk losing its credibility. That said, its track record in combatting asset bubbles has been much poorer, and this is the greater risk today.

Finally, there is widespread agreement that the U.S. government must do all it can to end the pandemic. By the same token, it is important that government programs be targeted to those who are truly needy rather than to provide broad stimulus for an economy that is on the road to recovery.

A version of this article was posted to Forbes.com on February 16, 2021.