Remarks delivered at the New Jersey Institute of Technology Economic Conference on November 3rd.

One of the hallmarks of Donald Trump’s theme of America First is the need to restore lost jobs in manufacturing owing to unfair foreign competition. During the presidential campaign Trump criticized NAFTA and the Trans Pacific Partnership (TPP), and he threatened to impose heavy duties on imports from China, Mexico, and other countries that are deemed to harm American workers. This stance raised alarm bells among investors who were concerned it could lead to protectionism. However, most have adopted a wait-and-see posture, presuming that Trump’s harsh rhetoric is a ploy to negotiate more favorable trade arrangements for the United States.

This note begins by considering factors that contributed to ballooning U.S. current account deficits since the early 1980s. We next examine the extent to which declines in U.S. manufacturing jobs can be linked to U.S. trade imbalances. We find there is no connection between U.S. jobs losses and NAFTA, and that most of the job declines occurred following China’s entry into the World Trade Organization (WTO) in 2000. This coincided with a massive build-up in foreign exchange reserves of China and other Asian economies.

We conclude by considering policies that are intended to narrow global payments imbalances. The Trump administration’s approach to negotiate bilateral trade arrangements will likely prove ineffective, and protectionist measures would invite retaliation. The challenge U.S. policymakers face is how to wean Asian economies away from their export-dependence on the USA without resorting to protectionism that could unsettle financial markets.

Origins of Chronic U.S. Trade Deficits in the 1980s

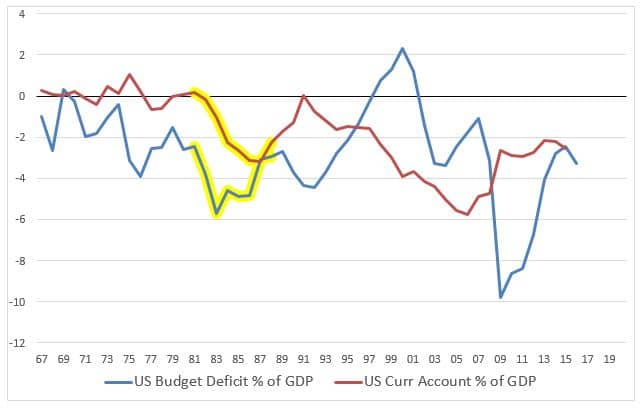

To understand the impact that international trade may have on U.S. jobs, one must first consider the factors that caused a dramatic shift in the U.S. status from the world’s largest creditor nation to its biggest borrower. This transition occurred during the 1980s, and it coincided with the United States running persistent large budget deficits that averaged 3% of GDP during the Reagan and Bush administrations (Figure 1).

Figure 1: U.S. Budget & Current Account Deficits (% of GDP)

Source: Bureau of Economic Analysis, Dept. of Commerce.

Source: Bureau of Economic Analysis, Dept. of Commerce.

The Japanese government contended the trade imbalances were attributable to lax U.S. fiscal policy that resulted in the USA having “twin deficits.” According to this view (which European officials and many prominent U.S. economists also espoused), the best way to reduce the U.S. current account imbalance would be to reduce the budget deficit. By doing so, aggregate demand would be lower and imports would shrink. Also, a smaller budget deficit would help to reduce bond yields, and thereby cause the dollar to soften as capital inflows from Japan and other countries would moderate.

U.S. officials countered that the bilateral trade imbalance was mainly the result of the Japan authorities intervening in currency markets to keep the yen undervalued against the dollar. The U.S. government, therefore, pressed the Japanese authorities to refrain from intervening in currency market. Moreover, they pressured Japan to implement “voluntary” export restraints (or quotas) on car shipments to the USA, which it did.

Because the U.S. government did not tackle its budget imbalance until the early-1990s, the burden of adjustment for narrowing the trade imbalance was relegated to the yen/dollar exchange rate: The yen appreciated steadily from 1985 to 1994 and confounded attempts by the Japanese government to counter deflationary pressures that emanated after Japan’s real estate and stock market bubble burst. Indeed, in 1993-1994 Treasury Secretary Lloyd Bentsen maintained the yen was undervalued, when it reached a record high of Y80/$ – a cumulative appreciation of more than three-fold from the beginning of 1980.

Impact of a Global Savings Glut

One of the priorities of the Clinton administration was to reverse the direction of U.S. fiscal policy, and it did so through a combination of defense spending cuts and tax rate increases for high-income earners. The economy also proved to be robust during the tech boom era, when it sustained annualized economic growth of 4%. This helped to generate revenues that brought the federal budget into surplus during the period from fiscal 1998 to 2001, the only surplus years after 1969.

Yet, despite this dramatic improvement in the budgetary picture, the U.S. current account deficit relative to GDP increased steadily from the mid-1990s to the mid-2000s, when it reached a peak of 6% of GDP. A level this high is generally considered to be unsustainable, because it implies a build-up in external debt that is considerably faster than GDP. This forced economists to reassess what was happening, and in 2005 Ben Bernanke, then a Governor of the Federal Reserve, put forth an explanation that the growing U.S. current account deficit was mainly the result of a “global saving glut.”1

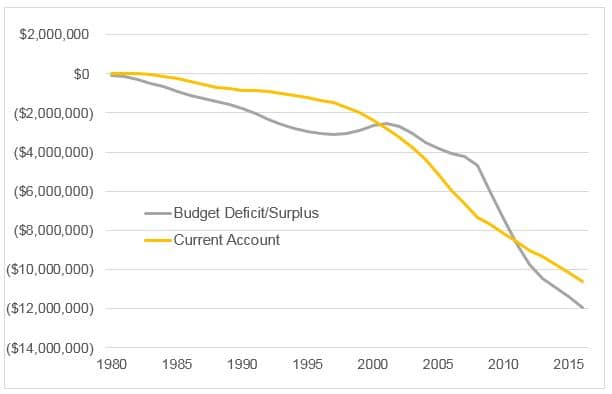

Bernanke’s argument is that many of the emerging economies in Asia were devastated by the 1997-98 crisis, in which their currencies depreciated by record amounts, ranging between nearly 20% for Singapore to more than 70% for Indonesia. This gave them a strong competitive advantage, which enabled them to boost exports while contracting imports. In addition, countries in the region responded by accumulating foreign exchange reserves in the ensuing years to lessen their vulnerability to currency crises in the future. Consequently, they amassed large current account surpluses, mainly with the United States, which in turn experienced a significant increase in its current account deficit. Thus, during this period at least the expansion in the U.S. current account deficit was primarily due to an increase in saving outside the United States, rather than due to a deterioration in the U.S. fiscal stance (Figure 2).

Figure 2: Cumulative U.S. Budget & Current Account Deficits, 1980 to 2017

Source: U.S. Treasury & Department of Commerce.

Role of International Capital Flows

The main takeaway is that international capital flows have been the principal driver of both trade balances and exchange rates since the breakdown of the Bretton Woods system in the early 1970s. According to Robert Aliber, the key distinction is whether a shortage of U.S. saving “crowded-out” some foreign borrowers or instead whether excess foreign saving “crowded into” the American market and displaced American saving. The conventional view among economists is the former one, but Aliber maintains the latter force has prevailed: “This inflow (of foreign capital) has led to a higher price for the U.S. dollar, a sharp decline in employment in U.S. manufacturing, a U.S. consumption boom, and a larger fiscal deficit.”2

My own assessment is that both sets of forces have been at play over the past four decades. The initial bout of chronic U.S. trade imbalances in the 1980s mainly stemmed from the shift to large U.S. budget deficits. When combined with tight monetary policy, they generated record high real interest rates that induced foreign capital inflows – mainly from Japanese life insurance companies and banks – that caused the dollar to appreciate steadily in the first half of the decade.

Since the mid-1990s, however, the main factor contributing to the increase in the U.S. current account deficit has been excess foreign saving, mainly from Asian countries. In this context, much of the capital inflows are the result of direct purchases of U.S. securities by foreign central banks, sovereign wealth funds and government-sponsored entities. A noteworthy example is China, whose holdings of foreign exchange reserves reached a peak of $4 trillion in 2014, largely as a result of purchases of dollar-denominated securities.

This experience raises the issue of why the adjustment mechanism has not worked as expected in the context of floating exchange rates. The explanation is two-fold: First, because the U.S. dollar is the world’s key reserve currency, the USA is not subject to the same balance-of-payments constraints that other deficit countries confront. Second, the world’s largest surplus countries – mostly in Asia as well as Germany – are not compelled to alter their domestic policies as long as they hold their excess savings in U.S. dollars. Given this predicament, there is no reason for global current account imbalances to change if the respective domestic policies do not change in the USA or the surplus countries.

Job Losses in Manufacturing

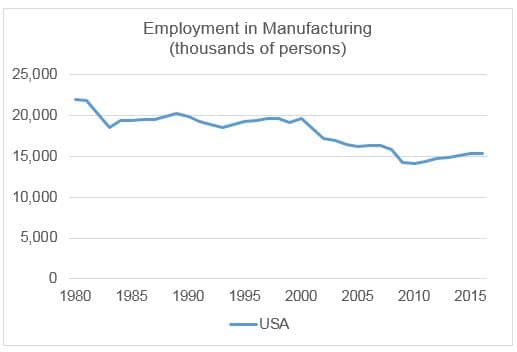

We now turn to the issue raised at the outset: Namely, to what extent are U.S. trade deficits linked with job losses in manufacturing. As shown in Figure 3, U.S. manufacturing jobs reached a peak of 19.5 million in 1979, and they have since fallen by 7 million to the current level of 12.5 million, which is where they stood at the onset of World War II. The initial decline of approximately two million workers occurred in the early 1980s in the context of a super-strong dollar, which created incentives for U.S. multinationals to increase production outside the USA. Thereafter, manufacturing jobs held fairly steady until the 2000-2009 period.

Figure 3: U.S. Manufacturing Jobs

Source: Bureau of Labor Statistics.

Source: Bureau of Labor Statistics.

The chart also reveals there is no evidence to support populist rhetoric that NAFTA, which came into play at the beginning of 1994, created significant job losses. In fact, the decade of the 1990s was one of the best periods for job creation in U.S. history, thanks to strong economic growth that accompanied the boom in technology. Economic studies that have investigated the issue in depth conclude the effect of NAFTA on U.S.jobs is marginal. Among the leading experts of trade agreements are Professor Gary Clyde Huffbauer of Georgetown University and Jeffrey J. Schott with the Peterson Institute for International Economics. They wrote a report during the 2008 presidential campaign in response to claims by then Senator Barack Obama, who cited estimates of one million job losses based on an analysis by union-funded economists.3 Their response is that NAFTA’s bad rap is mainly the result of “sound bites and bumper stickers versus real facts and statistics.”

By comparison, there is stronger evidence that U.S. job losses in manufacturing are linked to the widening in the U.S. current account deficit in the past decade, when Asian trade surpluses mushroomed. During this period, U.S. job losses in manufacturing totaled close to five million. The steepest declines occurred in the early part of the decade following China’s entry into the WTO and at the end of the end of the decade during the Global Financial Crisis.

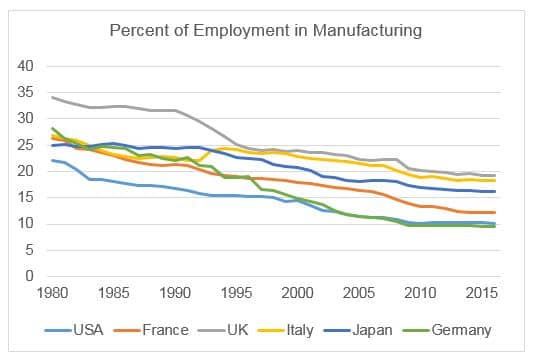

It should be noted that this phenomenon is not unique to America: Most industrial countries have experienced job losses in manufacturing, including Germany and Japan, which traditionally have run large trade surpluses (Figure 4). Consequently, many economists view the decline in manufacturing jobs as an integral part of a transition advanced economies undergo when they shift to become more service-sector oriented and knowledge-based. The pace of this transition is based on the rate of technological change; consequently, workers who lack technical skills are often the victims.

Figure 4: Share of Manufacturing in Total Output for Key Industrial Countries

Source: OCED.

Source: OCED.

Of the leading industrial economies, Germany has fared the best in sustaining its manufacturing base. When the country was unified in the early 1990s, there was a significant rise in unemployment in the former East Germany, because workers were less productive than their counterparts in West Germany and a 1:1 conversion rate was set between the deutschemark and ostmarks. However, conditions eventually stabilized, and the German economy benefitted from labor market reforms that were undertaken in the mid-2000s, which introduced greater wage flexibility into the system. In addition, Germany’s reliance on small and mid-sized firms and its unique system of on-the-job training has enabled it to meet the challenge from foreign competition.

The main takeaway is that while advanced countries have become more service-oriented and knowledge-based as they develop, some have done a better job at sustaining manufacturing jobs. The key to success is having flexible labor markets and on-the-job training.

Policies to Tackle Payments Imbalances

While the link between job losses and trade deficits is ambiguous, there is widespread agreement among economists and policymakers that the U.S. current account deficit and surpluses in Asia and Germany are too large. One concern is they could be de-stabilizing if they were to result in rapid debt accumulation by deficit countries. Another concern is they may contribute to protectionism. Therefore, it is important to consider what policies should be pursued to narrow global payments imbalances that will not unsettle financial markets.

The approach the Trump administration is pursuing emphasizes bilateral trade balances. Thus, the Department of Commerce under Secretary Wilbur Ross is focusing on countries with the largest bilateral trade imbalances with the United States, and it then disaggregates the imbalances further on product by product basis. The intent is to pressure surplus countries into reducing their exports to the USA or to increase their imports.

The problem with this approach is that it fails to consider the macro forces at play that are the critical drivers of trade imbalances and exchange rates. Two prominent economists and former policymakers, George Shultz and Martin Feldstein, state the flaws with the administration’s approach as follows:4

If a country consumes more than it produces, it must import more than it exports. That’s not a rip-off; that’s arithmetic. If we manage to negotiate a reduction in the Chinese trade surplus with the United States, we will have an increased trade deficit with some other country.

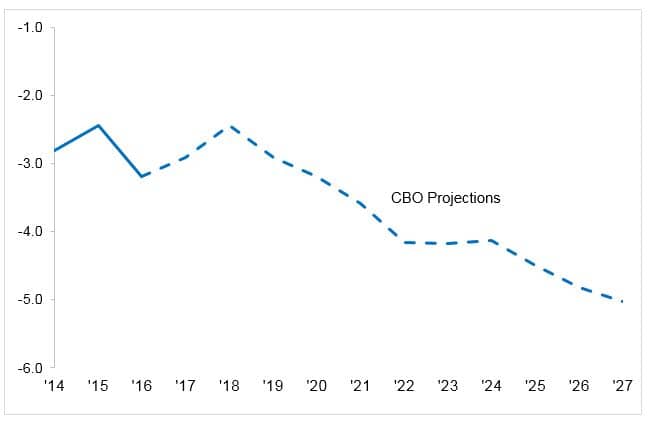

The argument that Shultz and Feldstein advance in essence is the “twin deficit” view that was discussed previously. It concludes the United States will continue to run large trade deficits as long as the federal budget deficit remains large. According to CBO, in the absence of any policy changes the U.S. budget deficit will balloon in the coming decade as aging baby boomers add to costs of entitlement reforms (Figure 5). One way the Trump administration can lower the trade deficit is to reduce the size of the budget deficit; however, prospective tax cuts are likely to cause it to expand.

Beyond this, it is also relevant to consider what can be done to encourage surplus countries to increase domestic spending. This has proved to be a challenge throughout the period of flexible exchange rates. In the 1980s, for example, the U.S. government conceived a “locomotive strategy” in which the leading surplus countries – Japan and Germany – would boost government spending to stimulate economic growth. When this did not materialize, the U.S. government subsequently pressured Japan to restrain its exports to the USA and to allow the yen to appreciate steadily. Yet, the huge appreciation of the yen during the 1980s and 1990s had little effect on Japan’s current account surplus.

The situation today is equally daunting, with China and emerging Asian economies also running persistent large surpluses. These countries followed Japan’s example and based their development strategies on promoting strong export growth, as American consumers became hooked on cheap imports.

Since the mid-2000s U.S. policymakers have pressed the Chinese authorities to refrain from purchasing dollars to keep the yuan artificially cheap, and Chinese foreign exchange reserves have fallen by about one trillion dollars in recent years. This suggests they have acted to limit the depreciation of the yuan against the dollar, and the argument that China is manipulating its currency to weaken it no longer applies. While the Trump administration has not brought trade sanctions against China thus far, the main reason is it is trying to incent the Chinese government to use its influence on North Korea to lessen geo-political tensions. However, the administration could change its stance at any time if it deems the Chinese government is not doing enough to restrain the government of North Korea or to reduce US-China trade imbalances. Consequently, the risk of protectionism and retaliation remains a risk to the outlook.

Figure 5: CBO Projections of Future Budget Deficits

Source: Congressional Budget Office.

Source: Congressional Budget Office.

1Ben S. Bernanke, “The Global Saving Glut and the U.S. Current Account Deficit,” Board of Governors of the Federal Reserve, April 14, 2005.

2Robert Z. Aliber commentary, July 3, 2017.

3Gary Glyde Huffbauer and Jeffrey J. Schott, “NAFTA’s Bad Rap,” The International Economy, summer 2008.

4George P. Shultz and Martin Feldstein, “Everything you need to know about trade economics in 70 words,” Washington Post, May 5, 2017.