Attractive Entry Point on Discount-Priced RMBS

The securities we are focused on are seasoned non-agency RMBS trading at a discount, often in the $80–$90 price range. These bonds typically carry lower coupons—around 3.5% on average—compared to newly-issued RMBS with coupons closer to 5.5%. Importantly, they are priced based on the assumption of persistent, slow prepayment speeds—meaning the market does not expect borrowers to refinance or move anytime soon, reflecting today’s environment of low housing turnover.

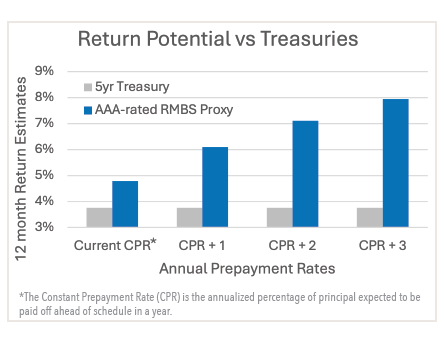

However, this conservative pricing creates an asymmetric return profile, where upside return is larger than downside risk. If housing turnover picks up or mortgage rates decline—leading to faster-than-expected mortgage prepayments—we stand to receive principal back at par more quickly than the market is currently anticipating, despite purchasing at a discount. With housing turnover already near historic lows, we view further declines as unlikely. Taking both upside and downside into account, we believe the upside outweighs the downside potential.

Spread Relative Value Remains

From a spread perspective, non-agency RMBS remain attractive, while spreads for most other fixed income sectors are near their tightest decile relative to history. We believe there is room for spread tightening, and positive excess return, especially for investors who are selective in security choice and credit quality.

High Credit Quality and Embedded Structural Protection

We are focusing on AAA and AA rated tranches, where we believe the risk vs reward is most compelling today. These bonds sit at the top of the capital structure and offer substantial protection against credit losses. Beyond structural seniority, these securities are also backed by seasoned mortgages that have benefited from two powerful tailwinds:

|

Together, these dynamics further insulate our positions against potential home price volatility or economic softening.

Attractive and Upside Optionality

Even in a scenario where spreads, rates, and home prices remain stable, these bonds offer attractive carry relative to comparable agency RMBS. The combination of strong income, credit protection, and upside optionality (via faster-than-expected paydowns or spread tightening) makes this segment of the market particularly appealing in today’s environment.

Download Why We See Value in Discount Non-Agency RMBS Securities Today

Download Why We See Value in Discount Non-Agency RMBS Securities Today