Risk Management Foundation

One of the most important aspects of overseeing a fixed income portfolio is managing risk. We believe it is the foundation for long-term investment success and plays a central role in shaping our culture of how we deliver alpha to our clients.

Management and awareness of risk are central to Fort Washington’s process and philosophy. This involves:

- Monitoring and managing forward looking risk.

- Ensuring risk exposures are within established portfolio guidelines.

- Incorporating risk-adjusted relative value analysis for both sectors and securities.

A well-defined approach to managing risk aids in dealing with uncertainty, particularly during times of distress, while seeking to maximize returns relative to risk.

Key Drivers of Returns

There are two key drivers of returns within fixed income portfolios – interest rates and credit spreads. Understanding exposures to these two factors provides valuable insight into how a portfolio might perform in different economic environments.

Interest rate risk can be measured and managed using traditional measures of duration. However, we believe traditional measures of credit risk (e.g. nominal weights, credit quality, spread duration, option adjusted spread) fall short in quantifying portfolio risks. As such, Fort Washington has implemented a proprietary and dynamic process that more fully quantifies a variety of risks, both intended and unintended, resulting in a comprehensive and intuitive assessment of risk.

Budgeting Risk Through a Cycle

At the core of Fort Washington’s risk management framework is the use of a risk budget. The risk budget is a tool used to determine the range of potential risk within a portfolio and how much of that risk to utilize at any given time. This allows Fort Washington to explicitly manage the level of risk within the portfolio over a market cycle to maximize returns with a keen focus on capital preservation.

There are two key components of a risk budget:

- Total risk budget - The range of potential risk within a strategy.

- The limits are determined by each portfolio’s risk tolerance and guidelines.

- Risk budget utilization - How much risk to assume at any given time within the risk budget.

- Determined based on two variables: economic outlook and asset prices.

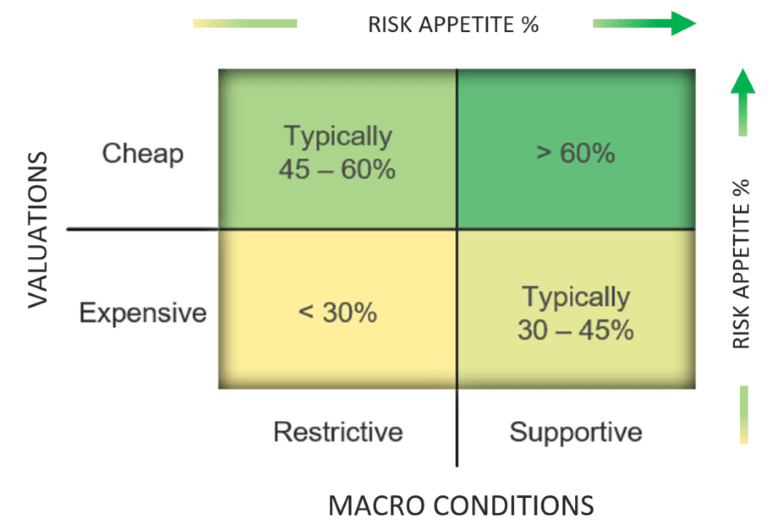

A portfolio’s targeted risk level within the budget is a function of our macroeconomic view and valuations. When the economy is growing and valuations are cheap, we would be inclined to move toward the higher end of a portfolio’s risk budgeting range, whereas the opposite would be true if growth was slowing and valuations were expensive. Actively managing our risk budget up and down over a market cycle has been a meaningful driver of excess returns.

The economic side of the analysis is both qualitative and quantitative, focused on assessing growth and inflation – the underlying fundamental backdrop for all sectors. Continuous discussions among senior leadership and our investment teams provide input for our outlook.

There are many ways to assess relative value, but it often starts with evaluating where current spreads are compared to historical observations (i.e. spread percentiles) and downside risk. Importantly, these quantitative measures are combined with a bottom-up fundamental assessment conducted by sector specialists.

While joining these two concepts is particularly intricate, a simplification of this logic is depicted in the table below.

Introduction to Index-Equivalent Spread Duration

The risk budgeting process for Fort Washington is fundamentally based on managing spread risk. Due to the shortcomings of traditional measures of spread risk, we’ve implemented a proprietary measure that is used throughout the portfolio management process - Index-Equivalent Spread Duration (IESD). IESD is a modified version of spread duration that measures a portfolio’s sensitivity to changes in spread relative to a market equivalent. However, as IESD is the primary risk metric used within the risk budget process, we enhanced it to adjust for two factors that increase the forecasting accuracy of the metric:

- The tendency for riskier bonds to experience larger spread moves.

- The tendency for shorter maturity bonds to experience more spread volatility than longer bonds.

The tendency of riskier bonds to experience larger spread moves was first demonstrated by Arik Ben Dor et al. at Lehman Brothers through their publication of DTS (Duration Times Spread) in the Journal of Portfolio Management during the Winter of 2007. Ben Dor et al. found that changes in spreads are not parallel but rather linearly proportional to the level of spread, whereby bonds trading at wider spreads experience larger spread changes. These findings mean that compared to an investment grade bond, a high yield bond with a higher spread typically encounters more volatility. An adjustment for riskier bonds is made by starting with spread duration and multiplying it by the absolute spread level (OAS). This resulting metric is commonly referred to as duration times spread (DTS).

However, the issue with DTS is that it can be challenging to consistently interpret and compare across different sectors or portfolios. As a result, Fort Washington subsequently applies an adjustment to DTS by dividing it by the spread on a basket of securities, or "index-equivalent." Within our investment grade portfolios that basket of securities is a group of BBB-rated securities within the Bloomberg US Credit Index (the US HY Corporate B-Rated Index is used for below investment grade strategies). This modification results in all securities being indexed to the same spread level, allowing for easy comparisons across sectors and among portfolios. Typically referred to as spread beta, this alteration is similar in concept to equity beta relative to a broad index such as the S&P 500.

The tendency of short maturity bonds to demonstrate more spread volatility than long maturity bonds is not addressed by either spread duration or duration times spread (DTS). However, as observed through historical analysis, shorter bonds tend to experience larger spread moves, especially on a percentage basis, than longer bonds. To further increase the efficacy of our IESD, we also adjust the spread duration of each bond by applying a maturity beta. Securities are indexed to a 10-year spread volatility, similar to the adjustment made for the level of spread risk above. A progression of OASD to Fort Washington's Index-Equivalent Spread Duration is below.

| IxDur = OASDBond X BSpread X BMaturity |

| where |

| OASDBond = OASD of bond |

| BSpread = Spread beta for bond |

| BMaturity = Maturity beta for bond |

The Value of Index-Equivalent Spread Duration

In summary, IESD adds many valuable benefits to a well-defined risk management framework:

- Improves upon traditional measures of credit risk, resulting in greater efficacy in managing portfolios.

- Provides an explicit measure of aggregate risk, which is utilized within the risk budgeting process.

- Allows for an apples-to-apples comparison of spread risk across individual securities, sectors, and portfolios.

- Intuitive, easy to comprehend metric expressed in years, similar to duration.

Our improved IESD metric allows portfolio managers, sector specialists, and analysts to analyze and discuss risk in the same single metric. In addition, IESD also allows our risk management process to be utilized from multiple viewpoints. Fort Washington enables portfolio managers to analyze this metric from a top-down view while sector analysts simultaneously view it from a bottom-up perspective. This framework puts risk management on the forefront, and desktop, of each investment professional’s mind throughout the investment process ensuring completeness and constant monitoring.

Operationalizing Index-Equivalent Spread Duration

Importantly, empirical evidence supports the use of IESD. Historical back testing is constantly used to confirm that our improvements for spread, and maturity continue to produce their intended impact. For the Bloomberg US Aggregate and the US Credit Indices, actual spread returns compared to the forecasted spread return by our index-equivalent spread duration have a correlation of 95% and 99%, respectively, over the last decade. This increased precision is most apparent during periods of heightened volatility which we believe is a time when risk management is most important.

Implementing IESD across our fixed income platform was and continues to be a significant investment in process and technology. The index-equivalent spread duration is calculated and updated on about 24,000 securities daily and available for consumption every morning. This process provides our investment team with a daily assessment of risk we can rely on consistently.

Complementing the Risk Budgeting Process

Our risk management framework utilizes IESD to also measure potential downside. Scenario modeling provides expected returns across different market conditions, such as a recessionary environment. These shocks allow portfolio managers to explicitly monitor total return across different stress environments in absolute terms and relative to benchmarks. This scenario analysis provides insight into the impact that different exposures and correlations, intended and unintended, have on portfolios.

Separately, this analysis can provide an additional input of relative value. Sector analysts can apply this concept across individual securities by comparing their upside return expectations to the downside scenarios. The analysis presents a risk versus reward metric for each security, allowing the investment team to monitor holdings for positions with outsized risk compared to return potential. This provides guidance into what sectors or issuers deserve increased scrutiny.

This downside analysis is used to further enhance our overall risk management process by supplementing our unique risk budgeting process.

Enhancing Returns Through Risk Management

Understanding the total risk of a fixed income portfolio can be cumbersome. It is important to know where to focus and understand the strengths and weaknesses of different risk measures and approaches. Fort Washington has spent much time and effort incorporating our proprietary risk budgeting process, made more efficient through IESD, into managing portfolios. These two unique practices have enabled us to consistently manage risk across various fixed income strategies and market environments, ultimately leading to highly competitive returns relative to benchmarks and peers.

At Fort Washington, helping our clients achieve their goals is our highest priority. A strong risk management approach, coupled with our experienced fixed income team, offers a reliable platform for investment success.