Table of Contents

Macro Insights

Records, Rates, and ResilienceU.S. equities advanced again in May, extending April’s sharp rally and lifting the major indices to new record highs. The S&P 500 gained 5.3%, while the Nasdaq rose 8.4% behind continued strength in large-cap Technology and AI-related shares. The Dow added 2.8%, and the Russell 2000 gained 4.4%, reflecting positive but more measured participation outside the market’s largest growth companies. While risk appetite remained firm, performance was shaped by a relatively narrow set of companies tied to compute demand, semiconductor supply, and the broader AI capital spending cycle. |

Technology remained the clear standout. Semiconductor and memory stocks continued their strong year-to-date run, while Software shares built on their recent recovery as investors reassessed the potential for AI to support productivity gains and future revenue growth. Hardware, Networking, and Communications-related companies also performed well, benefiting from demand tied to infrastructure buildouts. The earnings backdrop provided additional support, with first-quarter results coming in well ahead of expectations. S&P 500 earnings growth was the strongest since late 2021, though the gap between the largest Technology companies and the rest of the market remained meaningful.

Geopolitical risk remained an important but less disruptive market factor. The U.S.–Iran conflict persisted through the month, though several flare-ups failed to meaningfully unsettle equities. By month-end, reports of a potential memorandum of understanding and an extended ceasefire helped reinforce expectations that a negotiated path may be emerging. Oil prices declined as a result, with WTI moving back below $90 per barrel, easing fears that energy costs would become a more significant drag on growth or corporate margins.

The macro picture continued to present crosscurrents, with higher interest rates again a central market focus. Treasury yields have risen sharply in recent months, reflecting both an earlier move higher in inflation expectations—which has since moderated—and growing conviction that the Fed will be unable to lower rates over the foreseeable horizon. We explore the dynamics driving the move in rates further in this month’s Spotlight.

In May, yields moved modestly higher, particularly at the front end, as investors weighed firmer inflation data and a Fed that appears reluctant to pivot toward easing. Consumer spending remained broadly resilient, but affordability pressures and signs of greater caution among lower-income households became more visible. The leadership transition at the Fed also moved into focus as Kevin Warsh replaced Jerome Powell as Chair.

Looking ahead, the market remains supported by solid earnings, strong AI-related investment, and some moderation in geopolitical and energy risks. These factors continue to underpin our moderate overweight risk positioning. At the same time, the recent rise in rates bears watching, as persistent inflation and limited scope for policy easing could pressure valuations and rate-sensitive segments of the market. Following two strong months of gains, markets may be more vulnerable to shifts in sentiment, particularly if AI enthusiasm or expectations for a diplomatic resolution to the Iran conflict are challenged. Still, strong earnings growth has been the primary driver of returns this year, providing important fundamental support for risk assets.

Tech Outperforming, Valuation Premium Narrowing

Technology has seen its valuation premium to the market narrow despite outperforming, thanks to very strong earnings growth.

Forward PE Ratio of S&P 500 IT Sector Relative to S&P 500 Index

What to Watch

Developments surrounding the conflict with Iran will remain a focus due to their impact on energy prices and overall inflation. Assuming the labor market remains stable, investors will be watching all aspects of inflation, including direct impacts on consumer energy prices as well as second-round effects. Consumer spending will also be in focus as tax refunds support household spending, partially offset by rising energy prices. The AI/compute buildout will remain a key theme supporting growth.

|

Monthly Spotlight

The Story Behind Higher Rates

The recent rise in Treasury yields is often described—and may appear on the surface—as inflation driven. That reaction is understandable given the conflict in Iran and investor anxiety around inflation since 2022. Energy prices have risen sharply, and investors continue to reassess the path of near-term price pressures. But inflation alone does not explain the recent move. Increasingly, the backup in nominal rates reflects a broader repricing of growth, monetary policy, and market structure.

The largest driver has been stronger real growth expectations, as real yields have moved higher across the curve. The consumer is the largest component of U.S. growth, and spending has held up better than many expected, supported by higher-income households and accommodative fiscal policy. At the same time, corporate profitability remains near record levels, and business surveys have improved, with PMIs pointing to a U.S. economy that continues to expand. AI-related capital spending also remains an important source of investment, while many investors continue to anticipate eventual productivity gains from the technology. Together, these forces have created meaningful tailwinds for the U.S. economy and helped push long-dated real yields to levels rarely seen over the past two decades.

A second driver of higher nominal yields is the expectation that sticky inflation will keep the Fed from cutting policy rates in the near term. Inflation had been moderating coming into the year, but the rise in energy prices has forced investors to recalibrate their near-term forecasts. Core inflation remains well above the Fed’s 2% target, creating a difficult environment for rate cuts while the labor market remains stable and growth continues at a reasonable pace.

Another key driver has been changing market dynamics, or technicals, including a rising term premium. Fiscal deficits and elevated Treasury supply increase the compensation investors demand to hold longer-maturity bonds. At the same time, investor positioning and hedging demand related to near-term oil and inflation risks may be putting pressure on the front end of the curve. Global bond markets are also interconnected, and higher yields abroad have pulled U.S. rates higher. These dynamics, along with sizable Investment Grade issuance—particularly from companies funding AI infrastructure—have added upward pressure to different parts of the Treasury curve.

Implications for investors are more nuanced. Rising interest rates driven by strong economic fundamentals elicit a different reaction than rates rising for “bad” reasons, such as unanchored inflation expectations, concerns about fiscal sustainability, or the Fed cutting rates before inflation is contained. The key question is not just whether rates are higher, but why they are higher—and whether the economy can continue to absorb them. The evidence so far suggests that higher rates remain manageable, particularly while growth expectations are firm and risk assets continue to perform. Still, the reason rates are rising matters. A growth-driven increase in yields can be absorbed; a confidence-driven increase is much harder to digest. Investors should focus less on the level of yields alone and more on the message embedded in the move.

Chart sources: Bloomberg and Macrobond.

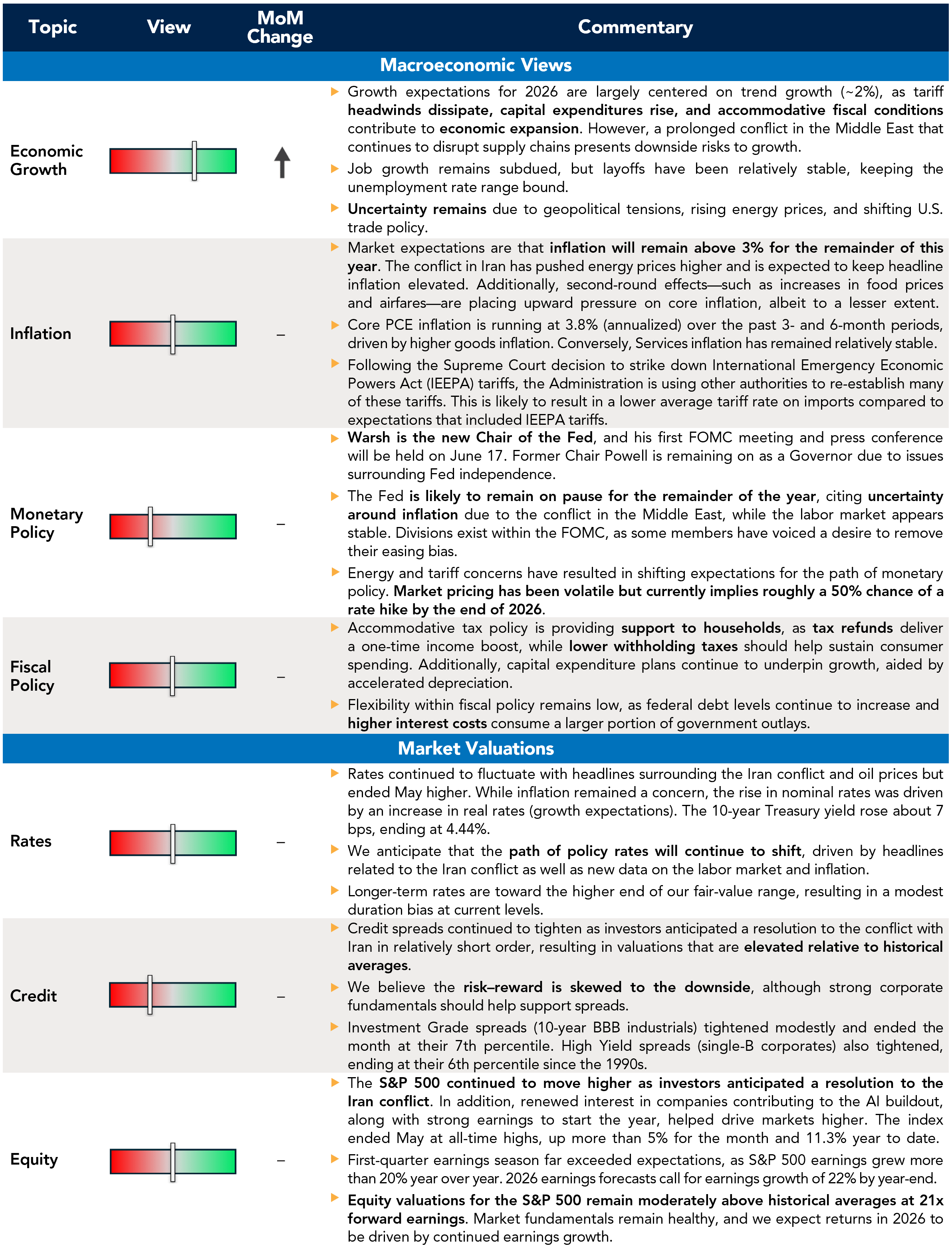

Current Outlook

Market Data & Performance

As of 05/31/2026

Source: Fort Washington and Bloomberg. *Returns longer than 1 year are annualized. Past performance is not indicative of future results.

Download Monthly Market Pulse – June 2026

Download Monthly Market Pulse – June 2026