Table of Contents

Macro Insights

Mixed Month Caps a Very Strong QuarterU.S. equities were mixed in June as leadership rotated beneath the surface, capping a very strong second quarter in which the S&P 500 gained roughly 17%. For June, the Dow gained 2.5% and the Russell 2000 rose 3.6%, while the S&P 500 declined 1.1% and the Nasdaq fell 2.8% after both indices posted fresh record highs earlier in the month. Notably, the equal-weighted S&P 500 outperformed the cap-weighted index, reflecting a broader market advance outside the largest growth companies. Industrials, Healthcare, and Financials led sector performance, while Communication Services, Consumer Discretionary, Technology, and Energy lagged. |

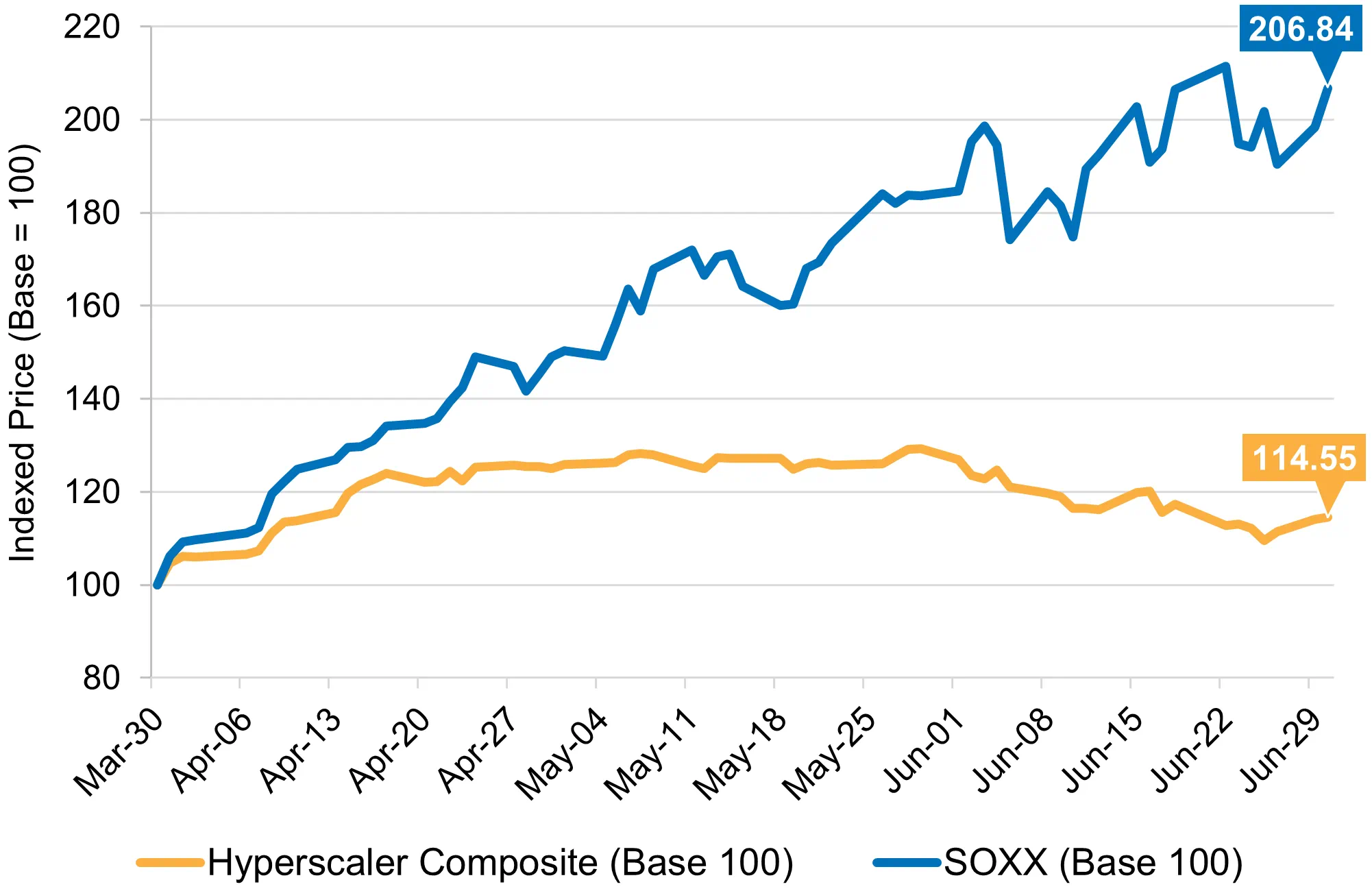

The AI trade became more discriminating. Semiconductors and memory stocks were standout performers, supported by strong demand, positive earnings commentary, and continued investment in compute infrastructure. At the same time, the largest Technology platforms came under pressure as investors drew a sharper distinction between the companies receiving AI-related capital spending and those funding it (see nearby chart). Some of this weakness reflected rotation and profit-taking, but it also highlighted growing scrutiny around AI monetization, rising infrastructure costs, and the potential for equity issuance to finance future investment. The result was not a rejection of the AI theme but a more selective market in which beneficiaries tied to infrastructure and supply constraints outperformed the largest CapEx spenders.

Geopolitical risks eased materially after the U.S. and Iran signed a ceasefire agreement, reopening the Strait of Hormuz (SoH) and creating a 60-day window for further negotiations. Oil prices fell sharply as flows through the strait improved, with WTI declining more than 20% for the month and returning to near pre-war levels. While setbacks are likely and the path to a lasting agreement remains uncertain, markets appear increasingly convinced that a diplomatic solution is ultimately on the horizon. As a result, equities are likely to be less sensitive to periodic flare-ups unless they materially threaten energy supplies or the negotiating process.

The macro backdrop remained resilient, even as markets priced in a more restrictive policy path. Payrolls, manufacturing and services activity, retail sales, and business surveys all pointed to continued economic expansion. At the same time, Chair Warsh struck a more hawkish tone at his first Fed meeting, emphasizing price stability and removing forward guidance from the policy statement, a subject we explore further in this month’s Spotlight. Futures markets moved to price in roughly 1.5 additional 25-basis-point rate hikes by year-end, pushing front-end yields higher. However, inflation expectations declined alongside oil prices, suggesting much of the move reflected a more hawkish posture from the new Chair rather than a meaningful reassessment of the fundamental backdrop. The yield curve flattened sharply, with short-term yields rising while long-term yields declined.

Looking ahead, the broadening of market leadership is encouraging and suggests the rally is becoming less dependent on a narrow group of mega-cap stocks. Strong economic data and solid earnings fundamentals remain supportive for risk assets, particularly if lower oil prices help ease inflation pressures. Still, a more hawkish Fed posture, renewed scrutiny of AI economics, and an unresolved geopolitical backdrop could contribute to continued volatility. We remain constructive, but June’s rotation highlights the importance of selectivity as market leadership evolves.

CapEx Spenders Materially Lag CapEx Recipients

The hyperscalers rolled over in June as semiconductor stocks continued their exceptionally strong run, benefiting from continued CapEx spending against a backdrop of limited supply, expanding revenue, and widening margins.

What to Watch

With oil prices back down to the low $70s, the conflict with Iran will likely begin to take a back seat, provided the Strait of Hormuz remains open. With the labor market stable and the Fed turning its focus back to prices, investors will be watching all aspects of inflation closely. Consumer spending will also remain in focus as markets assess households’ ability to sustain spending through the second half of the year. Meanwhile, the AI and compute buildout will remain a key theme supporting growth.

|

Monthly Spotlight

The New Federal Reserve

The June FOMC meeting was notable not for what the Fed did, but for how it communicated what may come next. The Committee left the policy rate unchanged, as expected, but the broader message differed meaningfully from prior meetings. In Kevin Warsh’s first meeting as Chair, the Fed presented itself as more focused on restoring inflation credibility, less willing to provide explicit forward guidance, and more comfortable allowing markets to form their own expectations about the path of policy.

The most immediate takeaway was that this was a hawkish hold. Rates were unchanged, but the statement was shorter, simpler, and more direct than investors have grown accustomed to. It also removed language that had previously suggested a bias toward lower rates, helping anchor market expectations. Warsh emphasized that the Fed remains committed to price stability and acknowledged that inflation has been above the Fed’s 2% objective for too long. That matters because the Fed appears to be shifting the center of its reaction function back toward inflation, particularly while growth remains resilient and the labor market appears stable. In that environment, the bar for rate cuts appears higher, and the risk of additional tightening is no longer negligible.

A second important change is the Fed’s apparent retreat from forward guidance. For much of the post-financial-crisis period, investors relied on Fed communication to help anchor policy expectations. Warsh seems less comfortable with that approach, underscored by his decision not to submit his own projections for the Summary of Economic Projections. His comments suggest that when markets simply reflect what policymakers have already said, the Fed loses a useful source of independent information. Instead, he appears to want markets to react more freely to incoming data and develop their own distribution of likely outcomes. That shift may be healthy over the long run, but it changes the near-term market dynamic. Less guidance means more uncertainty surrounding individual data points, Fed speeches, and inflation releases, which could create greater volatility at the front end of the curve.

Warsh also announced five task forces focused on reviewing communications, the balance sheet, data quality, productivity and jobs, and the inflation framework. These reviews do not necessarily imply immediate policy changes, but they do signal a broader reassessment of Fed operations. Importantly, Warsh made clear that reviewing the inflation framework does not mean abandoning the 2% goal.

The near-term implication for investors is likely to be higher interest rate volatility. A Fed that is more focused on credibility and less focused on guidance could ultimately improve the quality of market signals. However, the transition may be bumpy. A less predictable Fed may become more credible over time, but markets may demand compensation for that uncertainty in the near term, creating opportunities for tactical investors. As this new regime develops, we will pay close attention to Fed communication, incoming inflation data, and any signs of how the policy path and communications framework may evolve.

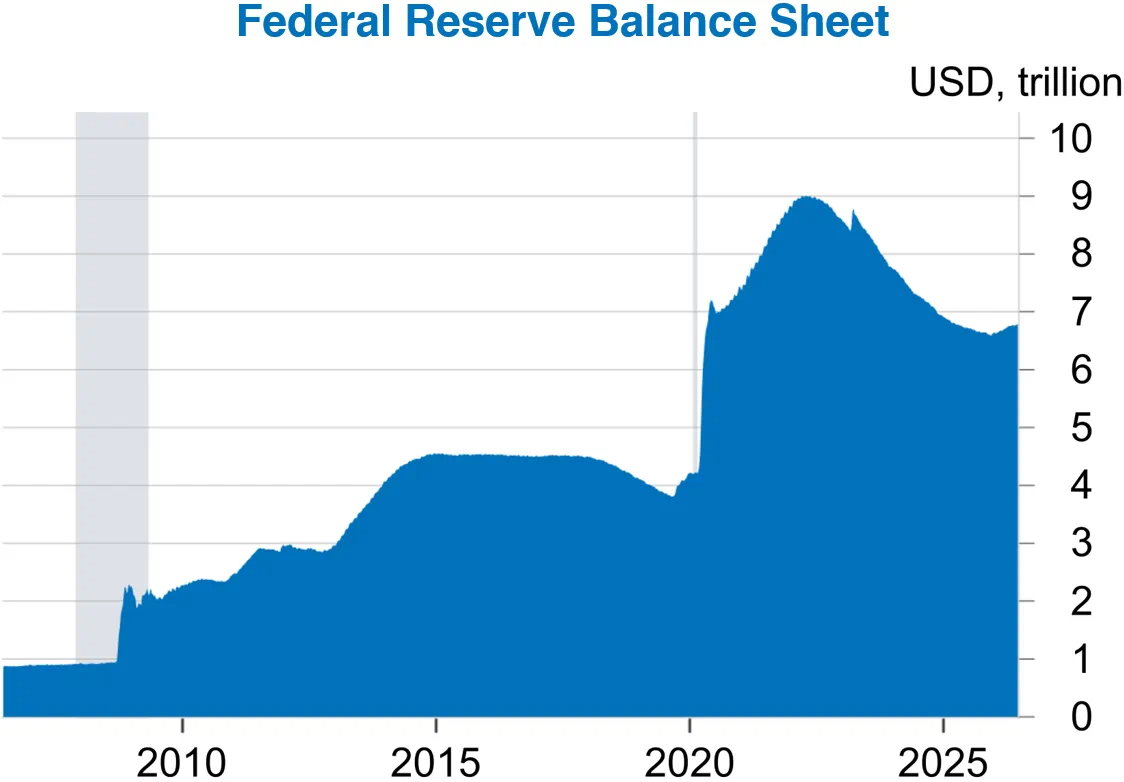

Chart sources: Federal Reserve and Macrobond.

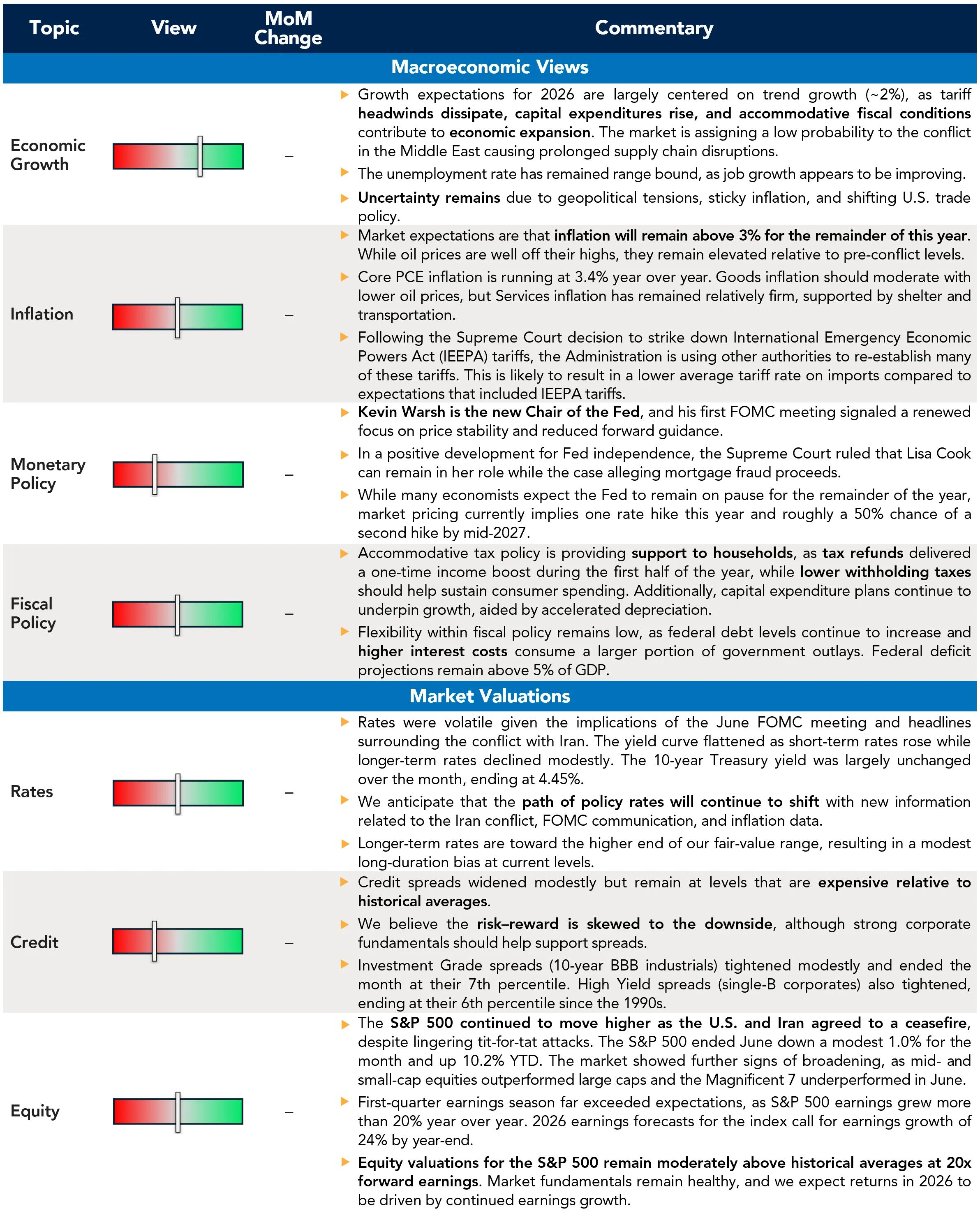

Current Outlook

Market Data & Performance

As of 06/30/2026

Source: Fort Washington and Bloomberg. *Returns longer than 1 year are annualized. Past performance is not indicative of future results.

Download Monthly Market Pulse – July 2026

Download Monthly Market Pulse – July 2026