The recent rise in Treasury yields is often described—and may appear on the surface—as inflation driven. That reaction is understandable given the conflict in Iran and investor anxiety around inflation since 2022. Energy prices have risen sharply, and investors continue to reassess the path of near-term price pressures. But inflation alone does not explain the recent move. Increasingly, the backup in nominal rates reflects a broader repricing of growth, monetary policy, and market structure.

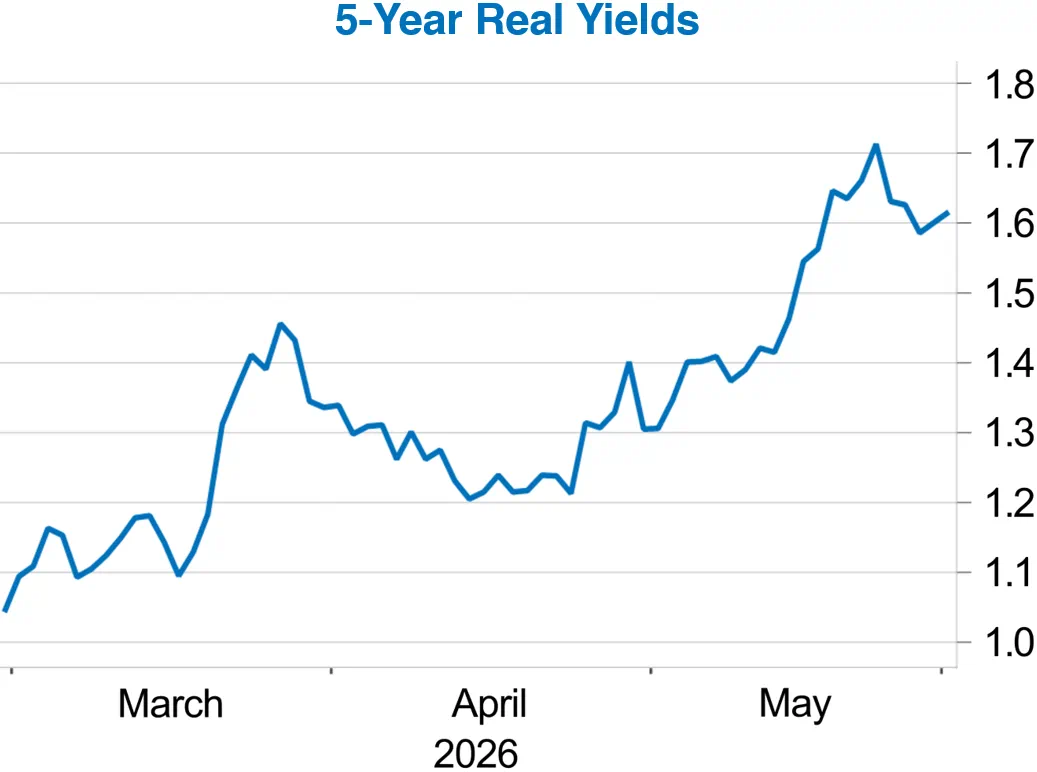

The largest driver has been stronger real growth expectations, as real yields have moved higher across the curve. The consumer is the largest component of U.S. growth, and spending has held up better than many expected, supported by higher-income households and accommodative fiscal policy. At the same time, corporate profitability remains near record levels, and business surveys have improved, with PMIs pointing to a U.S. economy that continues to expand. AI-related capital spending also remains an important source of investment, while many investors continue to anticipate eventual productivity gains from the technology. Together, these forces have created meaningful tailwinds for the U.S. economy and helped push long-dated real yields to levels rarely seen over the past two decades.

A second driver of higher nominal yields is the expectation that sticky inflation will keep the Federal Reserve (Fed) from cutting policy rates in the near term. Inflation had been moderating coming into the year, but the rise in energy prices has forced investors to recalibrate their near-term forecasts. Core inflation remains well above the Fed’s 2% target, creating a difficult environment for rate cuts while the labor market remains stable and growth continues at a reasonable pace.

Another key driver has been changing market dynamics, or technicals, including a rising term premium. Fiscal deficits and elevated Treasury supply increase the compensation investors demand to hold longer-maturity bonds. At the same time, investor positioning and hedging demand related to near-term oil and inflation risks may be putting pressure on the front end of the curve. Global bond markets are also interconnected, and higher yields abroad have pulled U.S. rates higher. These dynamics, along with sizable Investment Grade issuance—particularly from companies funding AI infrastructure—have added upward pressure to different parts of the Treasury curve.

Implications for investors are more nuanced. Rising interest rates driven by strong economic fundamentals elicit a different reaction than rates rising for “bad” reasons, such as unanchored inflation expectations, concerns about fiscal sustainability, or the Fed cutting rates before inflation is contained. The key question is not just whether rates are higher, but why they are higher—and whether the economy can continue to absorb them. The evidence so far suggests that higher rates remain manageable, particularly while growth expectations are firm and risk assets continue to perform. Still, the reason rates are rising matters. A growth-driven increase in yields can be absorbed; a confidence-driven increase is much harder to digest. Investors should focus less on the level of yields alone and more on the message embedded in the move.

Chart sources: Bloomberg and Macrobond.