The June Federal Open Market Committee (FOMC) meeting was notable not for what the Federal Reserve (Fed) did, but for how it communicated what may come next. The Committee left the policy rate unchanged, as expected, but the broader message differed meaningfully from prior meetings. In Kevin Warsh’s first meeting as Chair, the Fed presented itself as more focused on restoring inflation credibility, less willing to provide explicit forward guidance, and more comfortable allowing markets to form their own expectations about the path of policy.

The most immediate takeaway was that this was a hawkish hold. Rates were unchanged, but the statement was shorter, simpler, and more direct than investors have grown accustomed to. It also removed language that had previously suggested a bias toward lower rates, helping anchor market expectations. Warsh emphasized that the Fed remains committed to price stability and acknowledged that inflation has been above the Fed’s 2% objective for too long. That matters because the Fed appears to be shifting the center of its reaction function back toward inflation, particularly while growth remains resilient and the labor market appears stable. In that environment, the bar for rate cuts appears higher, and the risk of additional tightening is no longer negligible.

A second important change is the Fed’s apparent retreat from forward guidance. For much of the post-financial-crisis period, investors relied on Fed communication to help anchor policy expectations. Warsh seems less comfortable with that approach, underscored by his decision not to submit his own projections for the Summary of Economic Projections. His comments suggest that when markets simply reflect what policymakers have already said, the Fed loses a useful source of independent information. Instead, he appears to want markets to react more freely to incoming data and develop their own distribution of likely outcomes. That shift may be healthy over the long run, but it changes the near-term market dynamic. Less guidance means more uncertainty surrounding individual data points, Fed speeches, and inflation releases, which could create greater volatility at the front end of the curve.

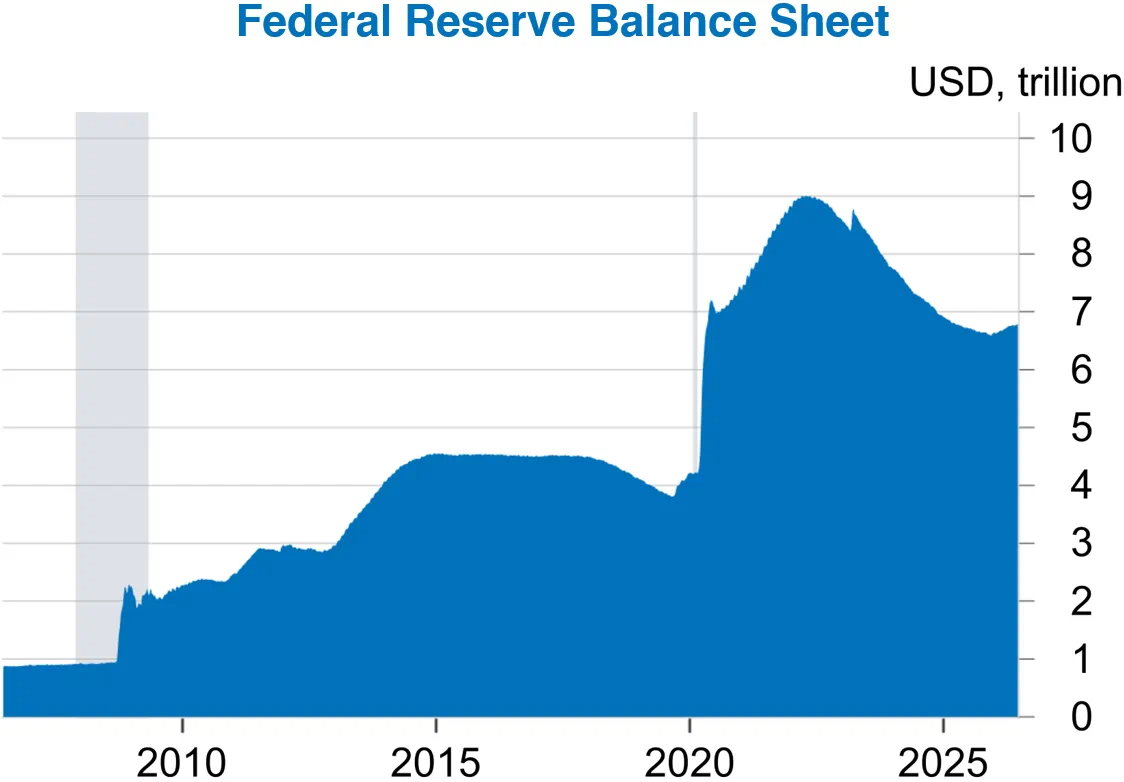

Warsh also announced five task forces focused on reviewing communications, the balance sheet, data quality, productivity and jobs, and the inflation framework. These reviews do not necessarily imply immediate policy changes, but they do signal a broader reassessment of Fed operations. Importantly, Warsh made clear that reviewing the inflation framework does not mean abandoning the 2% goal.

The near-term implication for investors is likely to be higher interest rate volatility. A Fed that is more focused on credibility and less focused on guidance could ultimately improve the quality of market signals. However, the transition may be bumpy. A less predictable Fed may become more credible over time, but markets may demand compensation for that uncertainty in the near term, creating opportunities for tactical investors. As this new regime develops, we will pay close attention to Fed communication, incoming inflation data, and any signs of how the policy path and communications framework may evolve.

Chart sources: Federal Reserve and Macrobond.