This article explains different categories of mutual funds: equity (stock) funds, bond funds, hybrid mutual funds, money market funds, and other mutual funds. These categories are further divided into subcategories.

This article does not include every type of mutual fund, but it covers the most common ones.

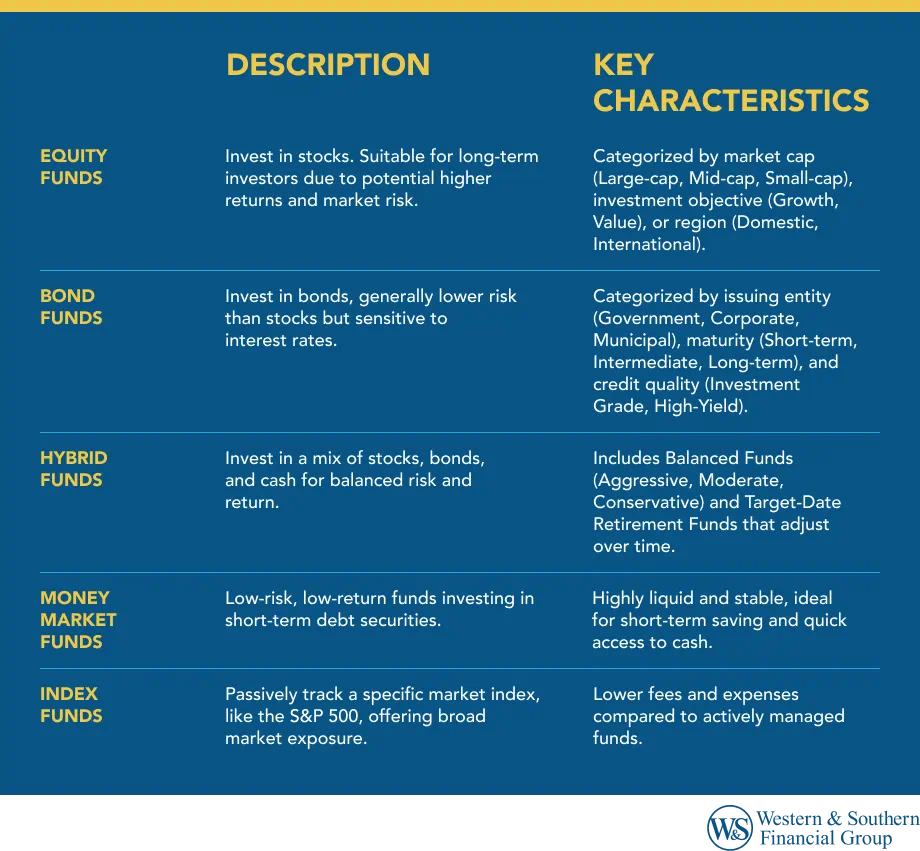

Equity Funds

Although equity funds are made up of stocks, mutual funds and individual stocks are not the same.

Equity funds, also called stock mutual funds, are often used by long-term investors with at least a five-year time horizon, and often 10 years or more. A longer holding period may be helpful because stock mutual funds have historically offered higher returns, along with higher market risk, compared with many other investments.

Market Capitalization

Equity funds may be grouped by market capitalization, or market cap. Market cap is the total value of a company’s outstanding shares. It is calculated by multiplying a stock’s price by the number of shares available.

- Large-cap stocks: Market capitalization greater than $10 billion

- Mid-cap stocks: Market capitalization between $2 billion and $10 billion

- Small-cap stocks: Market capitalization between $300 million and $2 billion

Investment Objective

Funds may also be grouped by their main goal, such as growth, value or income, or a mix of these.

Country or Region

Funds may be grouped by where the companies are based. Stock funds are often either domestic (U.S. stocks) or international (non-U.S. stocks).

Economic Sector

Some funds focus on specific parts of the economy, such as healthcare, technology, or real estate.

Large-Cap Funds

Large-cap funds invest in stocks of the largest companies by market cap. These stocks still carry market risk, but they have historically been more stable than mid-cap and small-cap stocks.

Mid-Cap Funds

Mid-cap funds invest in medium-sized companies. These stocks usually carry more risk than large-cap stocks but less risk than small-cap stocks. They may appeal to investors looking for a balance between growth and risk.

Small-Cap Funds

Small-cap funds invest in smaller companies that may not be widely known. These stocks have historically offered strong growth but tend to come with higher market risk than larger companies.

International Funds

International funds invest in companies outside the United States. These investments can add variety to a portfolio, but they often come with added risks such as political changes, currency shifts, and differences in accounting standards. These risks can be greater in emerging markets.

Growth Funds

Growth funds invest in companies expected to grow faster than the overall market. These funds tend to carry higher risk compared with other stock funds.

Income Funds

Income funds, also called dividend funds, invest in companies that pay dividends. Some focus on companies with a history of increasing their dividend payments. Dividends are not guaranteed.

Value Funds

Value funds invest in companies that appear to be priced lower than their actual worth. Investors often look for these opportunities as potential bargains.

Sector Funds

Sector funds focus on a single part of the economy, such as healthcare or technology. While some sectors may perform well at times, concentrating investments in one area can increase risk.

Bond Funds

Bond mutual funds can be grouped into several main categories and subcategories.

Issuing Entity

Bond funds are often grouped by who issues the bonds. Issuers may include governments, municipalities, or corporations. Some funds also invest in bonds from other countries.

Maturity or Duration

Bonds are grouped by how long they take to mature:

- Short term

- Intermediate term

- Long term

Credit Rating/Risk

Bond funds are also grouped by the credit quality of their holdings. Credit ratings help show the likelihood that a bond issuer will repay its debt.

Bonds with higher ratings, such as AAA, tend to have lower risk and lower yields. Lower-rated bonds, often called high-yield or junk bonds, tend to offer higher yields but come with more risk.

Bond funds can combine several of these features. For example, a fund may include long-term corporate bonds with lower credit ratings, or intermediate-term municipal bonds with high ratings.

Interest rate changes can also affect bond funds. When interest rates rise, bond prices usually fall. Longer-term bonds are generally more sensitive to these changes than shorter-term bonds.

Government Bond Funds

Government bond funds invest in bonds issued by the U.S. government. These are generally considered lower-risk investments. They may include short-, intermediate-, or long-term bonds. Some funds invest in bonds issued by other countries, which may offer higher yields but also carry more risk.

Municipal Bond Funds

Municipal bond funds invest in bonds issued by state or local governments. The interest earned is often exempt from federal taxes and may also be exempt from state taxes.

Corporate Bond Funds

Corporate bond funds invest in bonds issued by companies. These bonds usually offer higher yields than government bonds but carry more risk because repayment depends on the company’s financial strength.

Short-Term Bond Funds

Short-term bond funds invest in bonds that mature in less than five years. They tend to have lower risk and lower returns compared with longer-term bond funds.

Intermediate-Term Bond Funds

Intermediate-term bond funds invest in bonds that mature in five to ten years. They often offer a balance between risk and return.

Long-Term Bond Funds

Long-term bond funds invest in bonds with maturities greater than ten years. They may offer higher returns but are more sensitive to interest rate changes.

High-Yield Bond Funds

High-yield bond funds invest in lower-rated corporate bonds. These funds may offer higher returns but come with higher risk including the potential to default on their obligations.

Foreign & Emerging Markets Bond Funds

These funds invest in bonds issued by governments or companies outside the United States. Emerging markets include countries such as China, India, Brazil, and Russia. These investments may offer higher returns due to economic and political factors but also carry the potential to default on their obligations.

Hybrid Mutual Funds

Hybrid mutual funds invest in a mix of asset types, such as stocks, bonds, and cash. Common types include balanced funds, target-date funds, and lifestyle funds.

Balanced Funds

Balanced funds contain a mixed set of investments based on a stated goal, such as growth or income. Here a common types of balanced funds:

- Aggressive Allocation Balanced Funds: These funds hold a large portion in stocks, often 80% to 90%, with a smaller portion in bonds.

- Moderate Allocation Balanced Funds: These funds hold a mix of stocks, usually 50% to 70%, along with bonds and a small amount of cash.

- Conservative Allocation Balanced Funds: These funds focus more on bonds, often 40% to 60%, with a smaller portion in stocks and some cash.

Target-Date Retirement Funds

Target-date funds are managed portfolios designed around a specific retirement year. The mix of investments shifts over time, moving from higher stock exposure to more bonds as the target date approaches.

For example, a target retirement fund with a 2050 date may hold about 80% in stocks and 20% in bonds. Over time, the mix shifts toward fewer stocks and more bonds.

Target date funds combine stocks, bonds, and other investments and gradually become more conservative as the target retirement date approaches and passes. Principal is not guaranteed at any time, including at or after the target date.

Lifestyle Funds

Lifestyle funds are designed to match a specific goal, such as income or growth. They typically contain a mixture of stocks, bonds and cash.

Money Market Funds

Money market funds invest in cash and short-term debt, including certificates of deposit and U.S. Treasury bills. They aim to maintain a stable value and generate income through dividends. These funds are known for low volatility and easy access to cash.

You could lose money by investing in a money market fund. The share price can fluctuate, so your shares may be worth more or less than what you paid when you sell them. The fund may charge a fee when you sell shares or temporarily suspend redemptions if liquidity falls below required minimums due to market conditions or other factors. These funds are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The fund’s sponsor is not required to provide financial support, and you should not expect support at any time.

Other Mutual Funds

Two additional types of mutual funds include index funds and actively managed funds.

Index Funds

Index funds are designed to track a market index. They typically have lower fees because they follow a set strategy rather than active decision-making. Indices are unmanaged measures of market conditions. It is not possible to invest directly into an index.

Actively Managed vs. Passively Managed Funds

Mutual funds can be actively or passively managed. Passively managed funds, like index funds, follow a market index closely. Actively managed funds are guided by managers who select investments based on research and market conditions.

You could lose money by investing in a money market fund. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the fund is not a bank account and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Conclusion

There are many types of mutual funds, which can make it a challenge to choose the right funds for your needs. Understanding how funds are grouped can help you build a portfolio that aligns with your goals. Working with a financial professional can also help guide your decisions.