If you've been in the workforce for any period, you've likely heard of retirement funds. Not everyone wants to contribute to an employer-sponsored plan. And if you're one of 9 million people who are self-employed, you don't even have access to an employer-sponsored retirement plan.1

What is an IRA?

The good news is there are plenty of options. There's a lot you could do today to save for retirement - starting with looking into individual retirement accounts (IRAs). An IRA is a type of retirement savings account you can open on your own. These accounts are designed to help you save for retirement - usually through investment vehicles - while giving you some potential tax advantages along the way.

You're eligible to open a traditional IRA as long as you have taxable compensation or self-employment income and are not turning 70 1/2 this year. According to the Internal Revenue Service (IRS), the maximum amount you can contribute to a traditional IRA each year is $7,500. If you're 50 or older, you can contribute up to $8,600.2

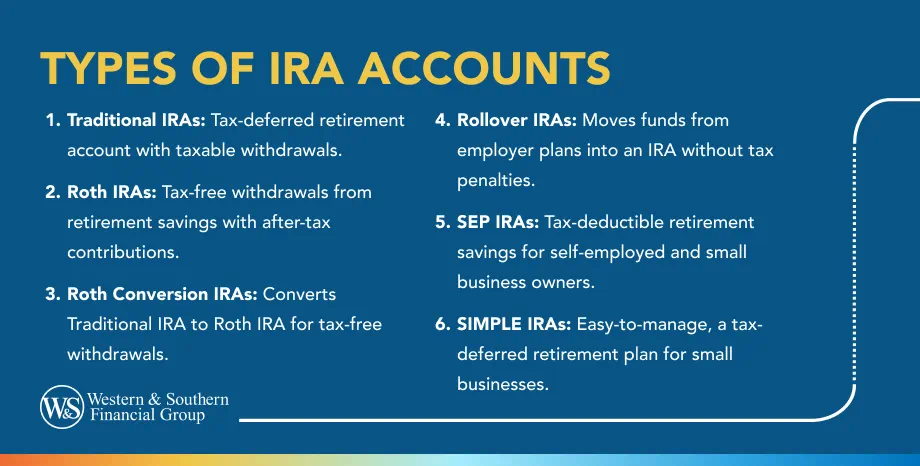

A traditional IRA lets you contribute without having to worry about taxes until you withdraw. You can also subtract your contributions from your annual gross income to decrease your tax liability.

Keep in mind that withdrawals of taxable amounts before reaching age 59 1/2 are subject to ordinary income tax and a 10% IRS penalty, with some exceptions.3

Roth IRAs

A Roth IRA is similar to a traditional IRA, with one significant difference: You pay taxes now instead of later. Some people prefer to take this route so they don't have to pay income tax later on in life when they withdraw.

Maximum Roth IRA Contributions

Roth Conversion IRAs

A Roth conversion IRA refers to the process of converting a traditional IRA into a Roth IRA. Those who choose this route do so because they don't want to worry about taxes later in life. To do the conversion, you must report the traditional IRA funds as income and pay taxes on them. (This may put you into a higher tax bracket for the year you report it as income.)

Rollover IRAs

A rollover IRA is when an employee chooses to roll over their former employer-sponsored plan into an IRA when they either change jobs or retire. This rollover is usually done with 401(k)s, 403(b)s or assets from a profit-sharing plan.

Many people choose to do this so their assets can maintain their tax-deferred status. People who open this type of account can also move their rollover IRA funds into a new employer's retirement plan.

SEP IRAs

A simplified employee pension (SEP) IRA is a type of IRA available for self-employed individuals and has its own contribution limits. Your contributions as a self-employed individual to a SEP IRA cannot exceed the lesser of 25% of your business profit or $72,000 for 2026.4 In addition, your contributions are tax-deferred until you withdraw them in retirement.

Some business owners decide to do a combination of a Roth IRA and SEP IRA. The Roth IRA handles current taxes, while the SEP IRA allows you to contribute more and deduct those current contributions from your taxes. Those who choose this route are usually either sole proprietors or have only one other employee. Freelancers and consultants may also decide to open a SEP IRA.

SIMPLE IRAs

A savings incentive match plan for employees (SIMPLE) IRA allows employers and employees to contribute to traditional IRAs. SIMPLE IRAs are used by employers who don't offer an employer-sponsored plan to their employees but want to give them some way to save.

Small-business owners, for example, may choose to offer a SIMPLE IRA. This IRA allows the owners to contribute and get tax advantages while also giving their employees an additional incentive to stick around.

Choose an IRA that fits your retirement plan and maximizes your savings. Start Your Free Plan

Sources

- The Employment Situation. https://www.bls.gov/news.release/pdf/empsit.pdf

- 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500.

- Retirement Topics - Exceptions to Tax on Early Distributions. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-tax-on-early-distributions.

- The 2026 Retirement Plan Contribution Limits. https://www.whitecoatinvestor.com/retirement-plan-contribution-limits/.