If you're looking for a way to transfer assets, manage your estate, and provide for your loved ones, trusts can be a useful tool for individuals, families, and businesses. Trusts can serve different purposes, such as avoiding probate, reducing estate taxes, and supporting minors or individuals with disabilities.

What Are The Four Main Types of Trusts?

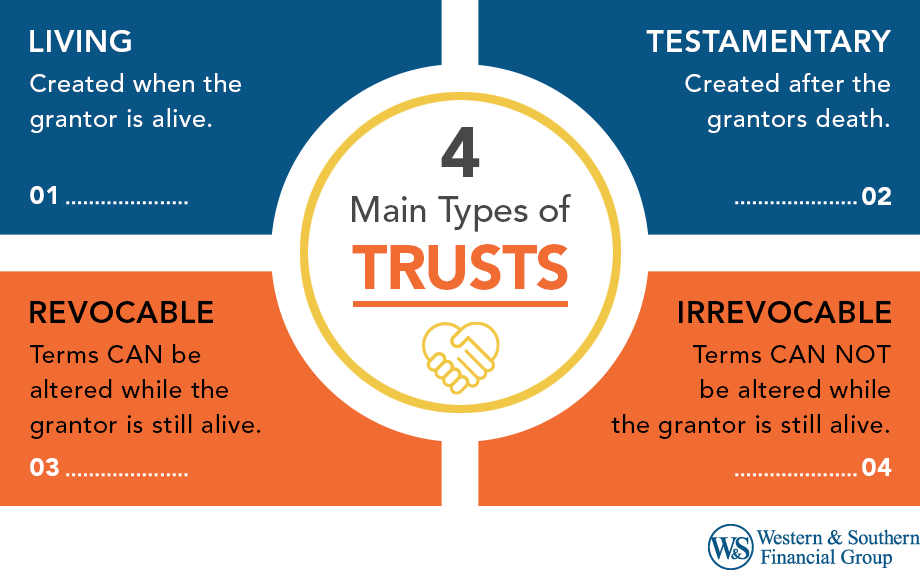

To understand the different types of trusts, it helps to compare the four main categories.

Living Trust vs. Testamentary Trust

Every trust can be classified as either a living trust or a testamentary trust based on when it is created.

Living Trust: Also called an inter vivos trust, a living trust is created while the grantor (the person setting up the trust) is still alive.

Testamentary Trust: A testamentary trust is created after death based on the grantor’s last will and testament. Its terms can be changed before the grantor passes away because they are written in the will.

Revocable Trust vs. Irrevocable Trust

All trusts are either revocable or irrevocable.

Revocable Trust: A revocable trust is created during the grantor’s lifetime and can be changed or canceled while the grantor is still alive.

Irrevocable Trust: Once an irrevocable trust is created, its terms generally cannot be changed or canceled by the grantor.

What Are The Different Types of Trusts?

There are many types of trusts. Understanding how they work can help you choose one that fits your estate needs.

AB Trusts

An AB Trust, also called a marital trust, is used by married couples to help manage estate taxes. When one spouse passes away, the trust splits into two parts. The “A” trust supports the surviving spouse. The “B” trust holds assets up to the estate tax exemption and passes them to heirs. This setup may help reduce or eliminate federal estate taxes.

Asset Protection Trusts

An asset protection trust is designed to protect assets from future creditors or legal claims. When assets are placed into an irrevocable trust, they are no longer legally owned by you. These trusts are often created in locations with laws that favor asset protection.

Blind Trusts

A blind trust allows an independent trustee to manage assets without input from the owner. The owner does not know how the assets are handled. This can help avoid conflicts of interest. Public officials often use blind trusts.

Bypass Trusts

A bypass trust, also known as a credit shelter trust, is an irrevocable trust used by couples to reduce estate taxes. It helps protect assets for beneficiaries while still supporting the surviving spouse.

Charitable Trusts

A charitable trust is an irrevocable trust set up to simultaneously benefit you, your beneficiaries, and a qualified charitable organization under IRS rules. There are two primary types of charitable trust:

- Charitable Lead Trust: Also called a charitable lead annuity trust (CLAT), this trust is set up to provide financial support through an annuity to the chosen charity or charities for a specified period of time. The remaining assets eventually go to the beneficiaries.

- Charitable Remainder Trust: Also called a charitable remainder annuity trust (CRAT), this trust works like the opposite of a CLT. A CRAT can create an income stream for you and beneficiaries with an annuity for a specified period of time, with the remainder of the assets going to charity.

Constructive Trusts

A constructive trust is a legal remedy that can be used to correct unjust enrichment. It is imposed by a court when one person has obtained or holds legal title to property that they should not have or when they have broken a fiduciary duty. Constructive trusts can protect many assets, including real estate, bank accounts, and investments.

Crummey Trusts

A crummey trust is an irrevocable trust that allows the transfer of assets to beneficiaries without consuming the lifetime gift tax exemption by providing the beneficiaries a short-term withdrawal right, usually within 30 to 60 days, over the contributions made to the trust.

Discretionary Trusts

A discretionary trust is an estate planning tool that gives the trustees the power to decide how and when to distribute the trust assets and income to the beneficiaries. The trustees have complete discretion over the trust assets, meaning beneficiaries do not possess an automatic right to receive any.

Dynasty Trusts

A dynasty trust is an irrevocable trust designed to transfer wealth across generations without incurring estate or generation-skipping transfer taxes, enabling wealth to grow long-term and benefit multiple generations.

Family Trusts

A family trust, also commonly known as an AB Trust, is a type of Bypass Trust that ensures wealth is managed, protected, and transferred across generations effectively, aligning with the family’s financial goals and objectives. It's commonly used for wealth distribution, estate planning, and tax benefits. The trust provides a mechanism to control and protect assets, ensuring they are distributed according to the grantor's wishes.

Funeral Trusts

A funeral trust sets aside money to cover burial and funeral costs. The funeral home sometimes serves as the trustee. Funeral trusts are typically funded with cash, bonds, or the proceeds from a life insurance policy. This arrangement not only provides peace of mind to the individual but also ensures that funeral expenses are covered, reducing the financial burden on loved ones after their passing.

Generation-Skipping Trusts

As the name suggests, a generation-skipping trust is designed to transfer assets to a beneficiary who is two or more generations younger than the grantor (the person who creates the trust). A Generation Skipping Trust is subject to the Generation-Skipping Transfer Tax with certain exemptions.

Grantor Retained Annuity Trusts

A grantor retained annuity trust (GRAT) is an irrevocable trust set up for a certain period to minimize taxes on large financial gifts to family members or other beneficiaries. The grantor pays the taxes on the assets when the trust is established and receives an annual annuity payment for the term of the GRAT. When the established term ends, the beneficiaries receive the remaining assets.

Land Trusts

A land trust allows you to transfer ownership (title to real property) to a legal entity that holds the land for the benefit of a beneficiary. Land trusts can provide anonymity, protect land from development, provide for future generations, avoid probate, and protect assets from creditors and lawsuits.

Life Insurance Trusts

An irrevocable life insurance trust (ILIT) is designed to hold and manage a life insurance policy, keeping the policy proceeds outside of the insured's taxable estate. Irrevocable life insurance trusts (ILIT) can provide estate tax benefits, protect the proceeds from creditors, and offer more control over how the funds are utilized for beneficiaries.

Qualified Personal Residence Trusts

A qualified personal residence trust (QPRT) is a type of irrevocable trust that allows you to transfer your primary residence to the trust for a specific period of time. During the trust term, you retain the right to live in the home and pay for its upkeep. When the Qualified Personal Residence Trust term ends, the home is transferred to the beneficiaries without going through probate.

Qualified Terminable Interest Property Trusts

A qualified terminable interest property trust (QTIP) is set up to provide income for a surviving spouse and for the grantor to control assets after the death of a spouse. QTIPs may be useful when beneficiaries exist from a previous marriage and the grantor dies before the subsequent spouse.

Pet Trusts

A pet trust provides for the care and financial support of one's pets after the owner's death or incapacity. It specifies a designated caregiver for the pets and provides funds for their ongoing needs. A Pet Trust ensures that pets receive the intended care and attention throughout their lifetime.

Special Needs Trusts

A special needs trust is designed to benefit individuals with disabilities without jeopardizing their eligibility for government benefits. Assets held in this trust are not counted for means-tested programs like Medicaid or Supplemental Security Income. The trust funds are used to pay for supplementary expenses that enhance the beneficiary's quality of life without replacing government assistance.

Spendthrift Trusts

A spendthrift trust is designed to protect the assets of a trust from the beneficiaries' creditors and to restrict the beneficiaries' access to the trust principal. This type of trust prevents beneficiaries from recklessly spending their inheritance, as distributions are made at the trustee's discretion. A Spendthrift Trust is particularly useful for beneficiaries who might be financially irresponsible or face potential legal judgments.

Totten Trusts

A totten trust, also known as a payable-on-death (POD) account, is a type of informal revocable trust where a depositor establishes an account in their name with the intent for the funds to be transferred to a named beneficiary upon the depositor's death. It allows for the easy transfer of bank or investment accounts without going through probate. The depositor retains full control over the funds during their lifetime, including the ability to change the beneficiary or withdraw the funds.

Bottom Line

A trust can help manage and transfer assets while offering certain advantages. However, trusts can be complex and may not fit every situation. It may help to speak with an estate planning attorney to review your options and decide what works for your needs.