For any individual retirement accounts (IRAs) you hold, you have been asked to name a beneficiary. This person or entity inherits your account after you pass away. Your choice can affect how the account is taxed based on who you name as your IRA beneficiary. Planning ahead matters, especially after the SECURE Act changed tax rules for non-spouse beneficiaries.

Here is what to expect based on the type of IRA you have and who you choose as your beneficiary.

IRA Required Minimum Distributions

One of the key benefits of a traditional IRA is tax-deferred growth on contributions and earnings. However, taxes cannot be delayed indefinitely. Required minimum distribution (RMD) rules determine when withdrawals must begin.

As the original account holder, you generally must start taking RMDs at age 73 (age 72 before 2023).1 The IRS provides a schedule based on life expectancy to calculate how much must be withdrawn each year. If the full balance is not withdrawn before death, the beneficiary follows their own RMD schedule.

Previously, IRA beneficiaries could spread withdrawals over their life expectancy to manage taxes over time. The SECURE Act of 2020 changed this. Many beneficiaries must now withdraw the full balance within 10 years of inheriting the account.

Types of IRA Beneficiaries

As mentioned above, you have several options when naming a beneficiary for an IRA. Here are the main types to consider.

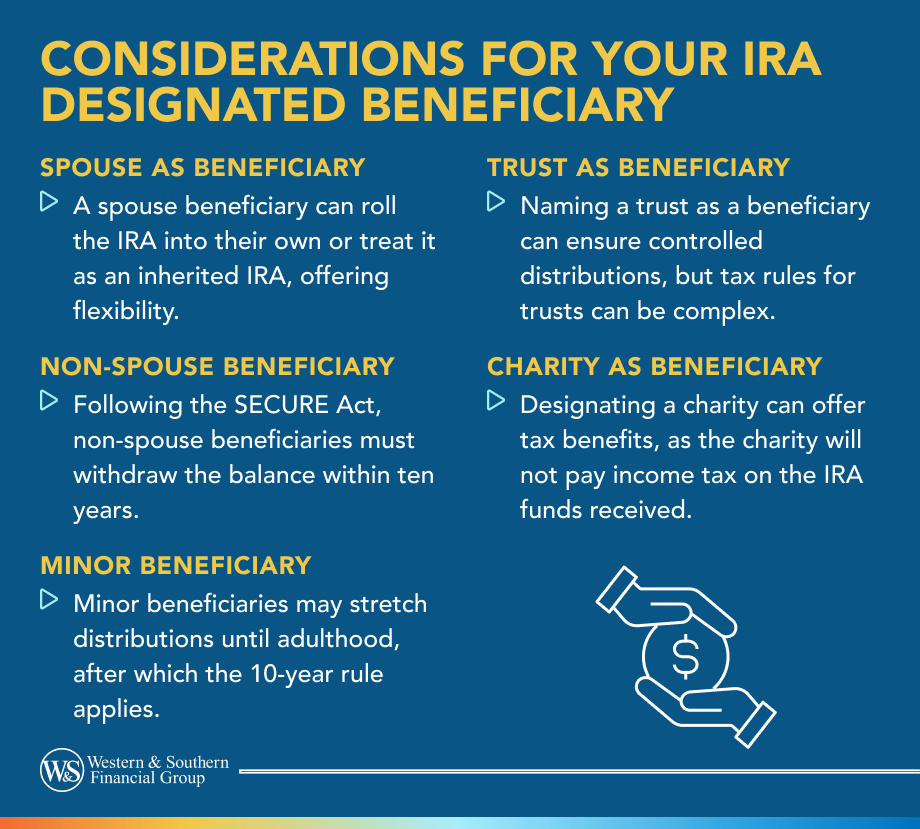

Spouses

Spouses have the most flexibility when managing an inherited IRA. They can transfer the funds into their own IRA, 401(k), or another retirement plan.2 They may also name themselves as the account owner and continue contributions. These options are not available to non-spouse beneficiaries.

After the transfer, the spouse follows the required minimum distribution (RMD) rules for their own account.

If the account holder died in 2020 or later before the required beginning date, a spouse has several options. They can keep the account as an inherited IRA and delay RMDs until the year the account holder would have turned 72 or 73. They can take distributions based on their own life expectancy, follow the 10-year rule, or roll the funds into their own IRA. Some may choose to delay withdrawals to allow more time for tax-deferred growth.

If the account holder died in 2020 or later after the required beginning date, a spouse can keep the account as an inherited IRA and take distributions based on their own life expectancy or roll it into their own IRA. These options provide more control over timing and how long the funds remain invested.

Beneficiaries Not More Than 10 Years Younger Than You

If you name someone within 10 years of your age as a beneficiary, they also have added flexibility with IRA RMDs. This could include a sibling, cousin, partner, or another person close in age.

When they inherit the IRA, they can spread RMDs over their own life expectancy. This may help reduce the yearly tax impact. For example, if you pass away at 45 and your brother inherits the account at 43, he may be able to delay some taxes until later in life. They may also choose to withdraw all funds within 10 years of inheriting the IRA.

Beneficiaries More Than 10 Years Younger Than You

If your designated beneficiary is more than 10 years younger than you, such as a niece or nephew, they have fewer options. They must withdraw all funds within 10 years of inheriting the IRA. Before the SECURE Act, these beneficiaries could take withdrawals over their lifetime. Now, they must withdraw the full balance and pay any taxes owed within that 10-year period.

Minor Children

A minor is someone under the age of majority in their state, usually 18 or 21. Minors cannot manage inherited property. If you name a minor as a beneficiary, a guardian manages the account and withdrawals until the child reaches the age of majority.

Most minor beneficiaries must withdraw all funds within 10 years. An exception applies if the beneficiary is your child. Withdrawals are then based on the child’s life expectancy using IRS tables, which often results in smaller amounts. Once the child reaches the age of majority, the 10-year rule begins, and the remaining balance must be withdrawn within that period.1

For example, if your 8-year-old daughter inherits your IRA, she can take RMDs based on her life expectancy until age 18. She then has 10 years to withdraw the remaining funds, meaning the account must be fully withdrawn by age 28.

One concern is whether a young adult will manage the money responsibly. In some cases, a trust may be worth considering.

Beneficiaries Who Are Chronically Ill or Disabled

You can name a beneficiary who is chronically ill or disabled. These individuals may take distributions over their lifetime instead of following the 10-year rule. This allows more time to manage and use the funds. They may also choose to withdraw the full balance within 10 years.

One concern is that receiving an inheritance could affect eligibility for certain government programs, such as Medicaid or Supplemental Security Income (SSI). These programs often limit how many assets a person can have. For example, SSI generally requires assets below $2,000.3 To help address this issue, you may consider setting up a special needs trust.

Trust Funds

A trust is a legal arrangement that holds assets for a beneficiary. You can name a trust as the beneficiary of your IRA. After your death, the trust receives the IRA funds and distributes them based on your instructions.

A trust can help manage how and when assets are distributed. It may also offer protection in situations such as divorce or legal claims. For minors or beneficiaries who may spend funds quickly, a trust allows you to set clear rules. A special needs trust may also help preserve eligibility for certain government benefits.

There are different types of trust funds, and the tax treatment depends on the structure and the beneficiary. A legal professional can help determine which option fits your situation.

Charities

You can name a charity as the beneficiary of your IRA. Because charities are tax-exempt, they do not pay income tax on withdrawals from the account. This approach can affect how assets are passed on. For example, you may leave IRA funds to a charity while leaving other assets, such as life insurance, to your family.

Estates

Your estate includes your assets at death minus any debts. Your will outlines how these assets are distributed, and the probate court oversees the process. Naming a beneficiary for your IRA usually helps the account avoid probate, so funds can be received more quickly.

If no beneficiary is named, the IRA becomes part of your estate. This can also happen if the estate is listed as the beneficiary or if the primary beneficiary has passed away and no contingent beneficiary is named.

When an IRA goes through the estate, probate can delay access to funds. The account may also be subject to creditor claims for outstanding debts.

The estate has limited withdrawal options. If you pass away before starting RMDs at age 72 or 73, the full balance must be withdrawn within 10 years. If you pass away after starting RMDs, withdrawals must follow your remaining life expectancy based on IRS calculation.

Tax Rules for Different IRA Types

The taxes owed depend on the type of IRA passed on. Here is what you and your beneficiaries may expect.

Traditional IRAs

If you funded a traditional IRA with pre-tax contributions, you will owe income tax on all withdrawals when you take money out. The same applies to your beneficiary when they inherit the account. If they must withdraw all funds within 10 years, this could raise their total taxable income.

They will owe income tax on withdrawals, and the added income may push them into a higher tax bracket. This can increase the taxes they owe on other income. It may also affect their eligibility for certain benefits. For example, their income could exceed the limits for contributing to a Roth IRA.

If you plan to leave a traditional IRA, talk through the tax impact with your designated beneficiary. This matters even more if the beneficiary is not your spouse.

Roth IRAs

With a Roth IRA, you fund the account with after-tax dollars. You do not receive a tax deduction for contributions. In return, withdrawals, including investment gains, are usually tax-free. To qualify, the account must be open for at least five years, and you must be age 59½ or older.

Your beneficiary receives the same tax treatment. If you owned the account for less than five years before your death, your beneficiary must wait until the five-year period is met before taking tax-free earnings. They can withdraw your contributions at any time without taxes.

Beneficiaries still need to follow required minimum distribution rules based on their category. However, withdrawals generally do not increase taxable income if the account meets the five-year rule.

Rollover IRAs

A rollover occurs when you move an IRA from one provider to another. This only changes who manages the account. If you move funds between the same type of accounts, the tax rules stay the same for you and your beneficiary. For example, moving a traditional IRA to another traditional IRA or a Roth IRA to another Roth IRA does not change the tax treatment.

Tax treatment changes if you convert a traditional IRA to a Roth IRA. This is known as a Roth conversion. You will owe income tax on the amount converted in the year of the transfer. After that, earnings can grow tax-free, and the account will follow Roth IRA rules for your beneficiary.

If you are able to cover the tax cost, this approach may help reduce the tax impact for your beneficiary later.

Inherited IRAs

If you inherited an IRA from someone else, your beneficiary becomes a successor beneficiary. They inherit an account that has already been passed down. Their withdrawal timeline depends on when you inherited the IRA and their beneficiary type.

If you inherited the IRA before the SECURE Act took effect in January 2020, your successor beneficiary has 10 years from the date of your death to withdraw the funds.

If you inherited the IRA after the SECURE Act took effect, the rules depend on the beneficiary category. Certain beneficiaries, such as a spouse, someone within 10 years of your age, a disabled person, or a minor child, have more flexibility. In many cases, they have up to 10 years from the date they inherit the account.

Other beneficiaries must follow the original 10-year schedule. For example, if you pass away five years into your withdrawal period, your successor beneficiary would have five years left to withdraw the remaining balance.

The Bottom Line

As you can see, IRA beneficiary rules are complicated and may change as tax laws are updated. However, with a well-designed strategy, they can give you and your beneficiaries more control over how taxes are handled.

For more help with your IRA beneficiary strategy, consider meeting with a financial professional who can review your situation and provide guidance tailored to your needs.

Sources

- Retirement plan and IRA required minimum distributions FAQs. https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs.

- Retirement topics - Beneficiary. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-beneficiary.

- SPOTLIGHT ON RESOURCES -- 2025 Edition. https://www.ssa.gov/ssi/spotlights/spot-resources.htm.