When considering if your retirement savings are enough, there are few clear answers. Comparing your savings to coworkers, friends, or family can make it harder to gauge where you stand. It can be difficult to tell if you're on track or falling behind.

One way to check your progress is by comparing your savings to average retirement savings by age. While many guidelines and tips can help you stay on track, they may not tell the full story. Your situation may differ from your neighbors and friends. Even so, comparing your numbers to average savings provides helpful context.

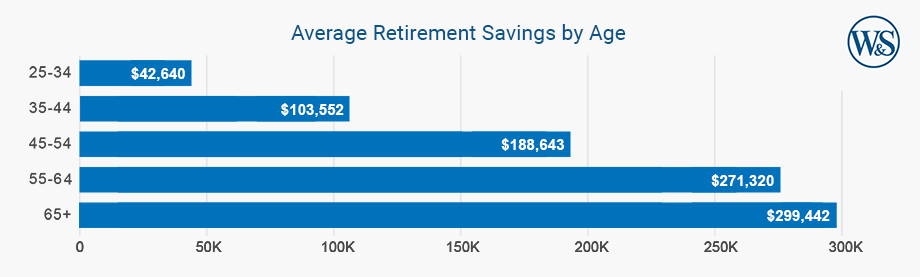

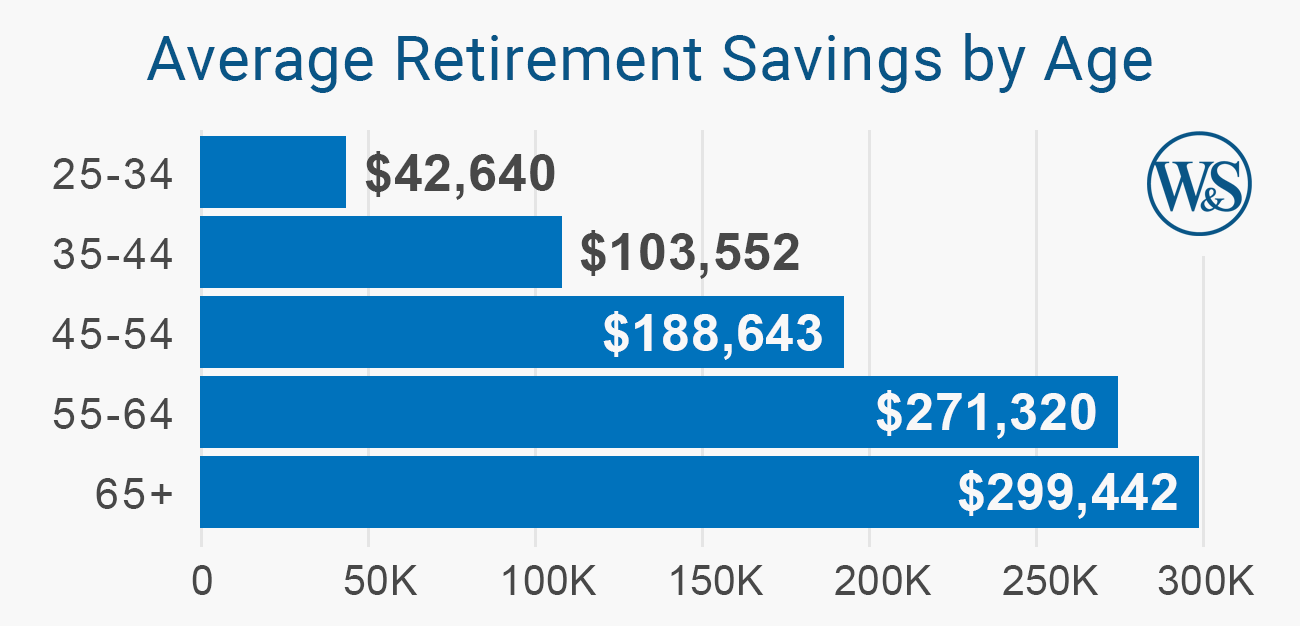

Here is how average retirement savings by age breaks down across each decade.

Retirement Savings When You're in Your 20s

A common guideline is to have the equivalent of your annual salary saved by age 30.¹ Here's how that may look:

- Median Income (Early 20s): $41,1842

- Target by Age 30: $41,184 in retirement savings

Average Retirement Savings in Their 20s

| Age Range | Average Savings3 |

|---|---|

| Under 25 | $6,899 |

| 25-34 | $42,640 |

In your 20s, you're just starting your career and living on your own. You have decades before retirement, which gives you time to learn about personal finance, save for retirement and pay off debt. In particular, reducing student loan debt is a common goal for people in this age group, as carrying significant debt can hinder your ability to save down the road.

At this stage of life, having anything saved is better than nothing. Build your budget and stick to it.

Retirement Savings When You're in Your 30s

Many guidelines suggest having three times your annual salary saved by age 40.1 Here's how that may look:

- Median Income for a 35-Year-Old: $69,2642

- Target by Age 40 (Income x 3): roughly $207,792 in savings

- Average Retirement Savings for Ages 35 to 44: $103,5523

This is where suggested targets and actual savings levels often differ. Many people find it hard to save as much as recommended. Regardless, you can still make progress.

In your 30s, focus on increasing your 401(k) contributions. If your employer offers a match, contribute enough to receive the full amount. Continue paying down debt and reviewing your budget.

You still have many working years ahead. That may allow your savings more time to grow through compounding. Keep in mind that growth is not guaranteed and will vary with market conditions.

Retirement Savings When You're in Your 40s

It's often recommended to have six times your annual salary saved by age 50.1 Here's how that may look:

- Median Income for a 45-Year-Old: $71,5522

- Target by Age 50 (Income x 6): roughly $429,312 in savings

- Average Retirement Savings for Ages 45 to 54: $188,6433

Many people reach their highest earning years in their late 40s and early 50s. This makes it a key time to take control of spending and increase savings.

If possible, build strong saving habits before reaching your 40s to avoid needing to catch up later. During this decade, focus on contributing as much as you can to your retirement accounts.

Retirement Savings When You're in Your 50s & Beyond

General guidelines suggest having eight times your annual salary saved by age 60.1 Here's how that may look:

- Median Income for a 55-Year-Old: $67,7042

- Target by Age 60 (Income x 8): roughly $541,632 in savings

- Average Retirement Savings for Ages 55 to 64: $271,3203

Your retirement age is often based on when you qualify for full Social Security benefits. This falls between ages 65 and 67, depending on birth year. As retirement gets closer, review your savings strategy and how your money's invested. You may want to adjust your portfolio to lower risk while continuing to support long-term growth.

By the Time You Retire

Suggested guidelines often recommend saving about 10 times your annual salary by full retirement age.1 Here's how that may look:

- Median Income for a 65-Year-Old: $63,5442

- Target by Full Retirement Age (Income x 10): roughly $635,440 in savings if you plan to retire at 65

- Average Retirement Savings for Over 65: $299,4423

Final Thoughts

If you're not where you want to be yet, don't panic. What matters most is knowing where you stand and focusing on what you can control. Small, consistent steps help improve your situation over time. With steady effort, you may even move ahead of average savings levels in the years to come.

Sources

- Here’s how much money you should have saved at every age. https://www.cnbc.com/select/savings-by-age/.

- Average Salary By Age. https://www.forbes.com/advisor/business/average-salary-by-age/.

- How America Saves 2025. https://workplace.vanguard.com/insights-and-research/report/how-america-saves-2025.html.