Understanding these distinct employer-sponsored retirement plans is key to securing your income in retirement. They represent different philosophies for building wealth, and knowing their ins and outs helps empower your investment decisions for a truly comprehensive retirement plan.

Pension Plan Defined

A pension plan, or defined benefit plan, is a traditional retirement vehicle promising a specific monthly pension income in retirement.1 Your employer commits to providing a predictable payment for life after you've dedicated a significant part of your entire career and reached retirement age.

Typically, employer-funded, the employer manages investments and assets to meet these future obligations. Your annual pension benefit is usually calculated via a formula based on salary history, years of service, and retirement age.

This plan helps offer security and a steady income stream in retirement, independent of daily market fluctuations. While less prevalent in the private sector today, pensions remain vital for many.

| Pros of Pension Plans | Cons of Pension Plans |

|---|---|

| Predictable income for life. | Low portability if you change jobs. |

| Mainly employer-funded and managed. | Potential for underfunding (PBGC protection applicable). |

| No direct investment decisions for employees. | No employee control over investments. |

| Often include spousal benefits. | Benefits may not keep pace with inflation without COLAs. |

403(b) Plan Defined

A 403(b) plan is a defined contribution plan available to employees of public schools, non-profits, and religious institutions.2 Unlike a pension's fixed promise, a 403(b)-type tax-deferred retirement account puts you more in control.

You (and potentially your employer via matching) contribute to a retirement account. You then typically select investments (e.g., mutual funds, annuities). Your retirement fund balance depends on contributions and market returns.

The Internal Revenue Service (IRS) sets annual contribution limits, and these plans offer significant tax advantages. Contributions are usually pre-tax, reducing current taxable income and allowing tax-deferred growth. Some offer Roth 403(b) options (after-tax contributions, tax-free qualified withdrawals), creating a valuable separate retirement income stream.

| Pros of 403(b) Plans | Cons of 403(b) Plans |

|---|---|

| Highly portable | Bears investment risk |

| Employee control over investment decisions within the options available in the plan. | Savings depend heavily on contribution discipline |

| Potential for higher market returns (with higher risk) | Investment fees can impact returns |

| Significant tax advantages | Requires active management and informed investment decisions |

| Employer matching boosts your retirement fund |

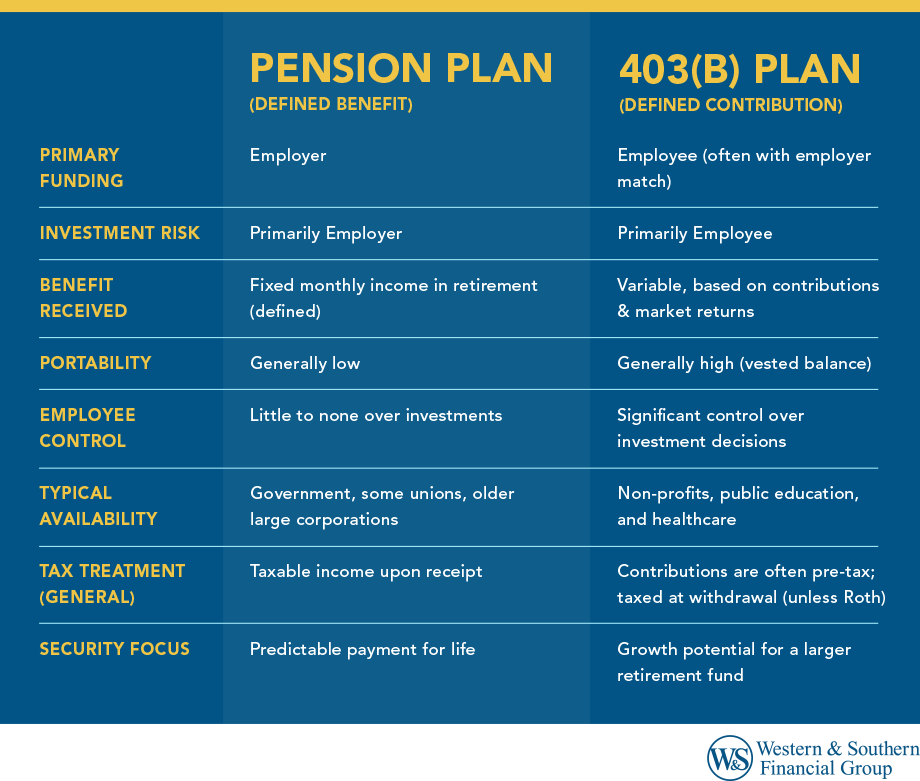

Pension & 403(b) Comparison

Understanding their core differences:

| Feature | Pension Plan (Defined Benefit) | 403(b) Plan (Defined Contribution) |

|---|---|---|

| Primary Funding | Employer | Employee (often with employer match) |

| Investment Risk | Primarily Employer | Primarily Employee |

| Benefit Received | Fixed monthly income in retirement (defined) | Variable, based on contributions & market returns |

| Portability | Generally low | Generally high (vested balance) |

| Employee Control | Little to none over investments | Significant control over investment decisions within the options available in the plan. |

| Typical Availability | Government, some unions, older large corporations | Non-profits, public education, and healthcare |

| Tax Treatment (General) | Taxable income upon receipt | Contributions are often pre-tax; taxed at withdrawal (unless Roth) |

| Security Focus | Predictable payment for life | Growth potential for a larger retirement fund |

403(b) Plans: Contributions, Investments, & Withdrawals

Helping you make the most of your 403(b) as part of your guide to retirement means understanding its key features.

Contribution Limits: The IRS sets annual limits.3 For 2026, the general employee elective deferral limit is $24,500.

- Age 50+ Catch-Up: If you are age 50 or over, you can contribute an additional $8,000.

- Age 60-63 Catch-Up: Thanks to the SECURE 2.0 Act, individuals aged 60, 61, 62, or 63 can make an even higher catch-up contribution limit of $11,250 in 2026 (instead of the standard $8,000 for this age group).

- 15-Year Rule (Special Catch-Up): Some employees with 15 or more years of service with certain qualifying employers (like public schools, hospitals, home health service agencies, or churches) who have, on average, contributed less than $5,000 per year previously, may be eligible for an additional special catch-up.

This can be up to $3,000 per year, with a lifetime maximum of $15,000 for this specific catch-up. This contribution is separate from and in addition to the age-based catch-ups, but specific ordering rules apply if eligible for multiple types.

Investment Options: Typically include annuities and mutual funds.

Vesting Schedules: Your contributions are always yours. Employer contributions often require a vesting period (working a set time) before they are fully yours.

Withdrawal Rules: Penalty-free withdrawals usually start at age 59 ½. Earlier withdrawals may incur a 10% penalty plus income tax (check IRS "Retirement Topics - Exceptions"). Required Minimum Distributions (RMDs) generally start after age 73 (this RMD start age is scheduled to increase to 75 for individuals who turn 74 after December 31, 2032, due to the SECURE 2.0 Act).

Pension Payouts: Calculating Your Benefit

For those with a pension plan, understanding payout options is crucial for planning your income in retirement.4

Pension benefit calculation: Your annual pension benefit often uses a formula: Years of Service x Percentage Multiplier x Final Average Salary.

The specific pension calculation should be documented in your pension plan documentation and maintained by your employer.

Payout Options:

- Single Life Annuity: Highest monthly payment, ends at death.

- Joint and Survivor Annuity: Lower monthly payment, continues to the surviving spouse.

- Lump-Sum Payment: Some plans offer a one-time payout, giving you control and full investment responsibility.

The Role of the PBGC: The Pension Benefit Guaranty Corporation (PBGC) insures many private pension funds if a plan becomes insolvent, offering a safety net up to certain limits. Public pensions are not PBGC-insured.

The Shifting Tides: The Future of Retirement Plans

The retirement landscape has largely shifted from traditional retirement pensions towards defined contribution plans like 401(k)s and 403(b)s, placing more savings and investment decision responsibility on individuals.

- Understanding the plan sponsor's financial health is key for those with pensions.

- For 403(b)-type tax-deferred accounts, staying updated on IRS rules (like the 2026 contribution limits and SECURE 2.0 Act changes) and investment strategy is vital for a comprehensive retirement plan.

Proactive planning throughout your career is essential for a sustainable income in retirement. Consulting with a qualified financial advisor is recommended.

Final Thoughts

Whether you prioritize security or flexibility, understanding the difference between a pension and a 403(b) is crucial to shaping your retirement strategy.

Pensions offer a defined benefit plan and payment for life; 403(b)s offer a flexible contribution plan with growth potential via market returns. The right fit depends on your career, risk tolerance, and life goals.

Actionable Insights:

- Understand Your Plans: Review details of any current employer-sponsored retirement plan, including the latest contribution rules if applicable.

- Assess Needs: Consider desired income in retirement and retirement costs. Start with a retirement savings calculator to quickly assess if your savings and income are sufficient for retirement.

- Diversify: If possible, combine plan types or supplement with individual retirement accounts.

- Seek Guidance: A financial advisor can help align with your overall financial picture and investment decisions.

Understanding the unique traits of a pension and 403(b) allows you to build a more robust retirement fund and comprehensive retirement plan.

See which retirement plan could work best for you. Start Your Free Plan

Sources

- General FAQs About PBGC - Pension Benefit Guaranty Corporation. https://www.pbgc.gov/about/faq/pg/general-faqs-about-pbgc

- IRC 403(b) tax-sheltered annuity plans - Internal Revenue Service (IRS). https://www.irs.gov/retirement-plans/irc-403b-tax-sheltered-annuity-plans

- 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

- Retirement Plans Benefits and Savings - U.S. Department of Labor. https://www.dol.gov/general/topic/retirement