Table of Contents

Table of Contents

Critical illness insurance and disability income insurance can both help to provide money when you're dealing with health issues. Whether you stop working temporarily or face high out-of-pocket expenses, these policies might play an important role — but they work differently. So, what's the difference between critical illness and disability income insurance, and when might it make sense to buy these policies?

Critical Illness vs. Disability Income Insurance

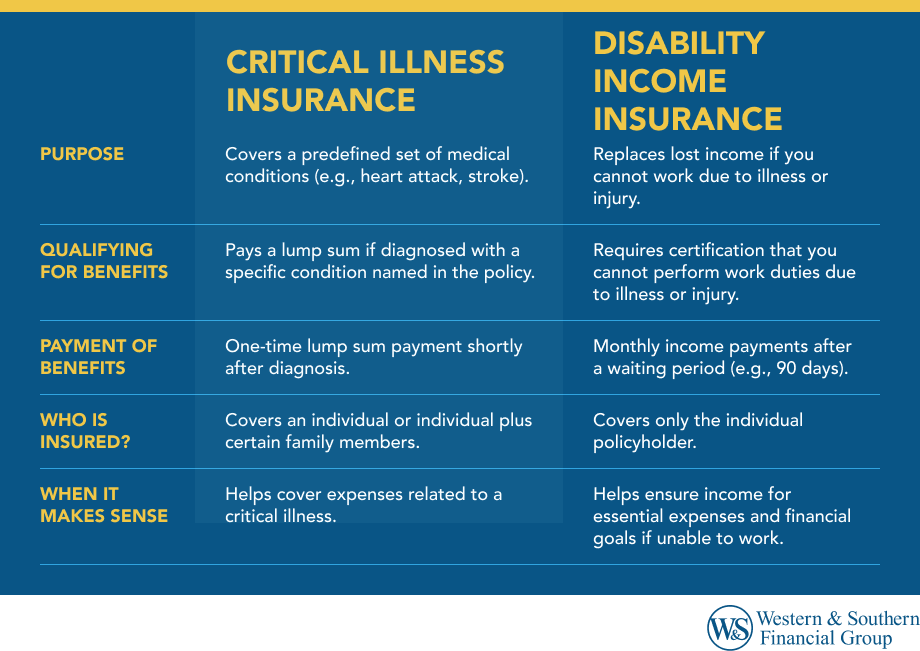

Critical illness insurance covers a specific, predefined set of medical conditions. Disability income insurance helps provides benefits to insureds who are disabled as a result of injury or illness and cannot perform normal work duties. There are several key differences between these two types of insurance.

Qualifying for Benefits

Critical illness insurance policies pay out if you are diagnosed with a specific condition named in your policy. Common examples include heart attack, cancer and stroke. These can vary quite a bit, and not all conditions are listed here.

With disability income insurance, you qualify for benefits if you're unable to perform certain duties required to earn an income. The specifics vary from policy to policy, but the idea is that you receive payouts if you can't work — whether the cause is illness, injury or other factors. A physician typically must certify that you're unable to work.

Payment of Benefits

Critical illness insurance is often a lump sum benefit, so you receive a relatively large amount up front. That payment might arrive shortly after you receive your diagnosis.

Disability income insurance typically pays benefits to you monthly, similar to the income from work that you're replacing. You may need to satisfy a waiting period before you receive payments (90 days, for example).

Who Is Insured?

Critical illness insurance might cover an individual or an individual plus certain family members. If any of the covered people are diagnosed with a specified condition, you could potentially receive benefits.

Disability income insurance policies generally cover only one person.

Prepare for unexpected medical expenses with critical illness insurance. Get My Free Financial Review

When Might Critical Illness Insurance Make Sense?

Critical illness insurance covers specific conditions that can be expensive and disruptive, so you might consider this form of insurance if you are concerned about how incurring such a condition might impact you and your loves ones financially.

As you evaluate critical illness insurance, consider reviewing your existing health coverage. Medical expenses that are related to your illnesses may already be covered at least in part. But you may also have additional out-of-pocket costs (for copays and medications, among other things), expenses related to necessary home modifications or caregivers, and more.

Critical illness insurance is not comprehensive health insurance coverage (often referred to as "major medical coverage") and does not replace it, but it can help provide funds to help pay for health care.

When Might Disability Income Insurance Make Sense?

Disability income insurance helps protect you from losing your income. If you or your family rely on your income, you might consider managing the risk of losing that with disability income insurance. For example, would you be able to pay for housing, food and other essential expenses after losing your income? And for how long? Also, losing your ability to work could interfere with saving for financial goals like retirement or education.

Two common types of disability income insurance are own-occupation and any-occupation. Own-occupation insurance specifically covers conditions that prevent you from performing your current job. Any-occupation covers conditions that prevent you from performing any work that you are otherwise able to perform.

Long-term disability policies can help provide monthly income for several years or longer. They typically do not replace 100% of your income, but they can help provide resources to reduce the impact of an injury or illness that keeps you from working.

When Could Both Types of Insurance Make Sense?

Critical illness and disability income insurance both help provide money when health conditions necessitate it, but they work differently. As a result, using both types of policies might help you maximize coverage: You could receive a lump sum if you suffer from specific conditions, and you could receive monthly income if you're unable to work, if your condition qualifies for both. Buying both forms of coverage could make sense if you have the cash flow available to pay both premiums and you want to help reduce risk.

However, there is no guarantee that you will encounter a health condition covered by both policy types. For example, if you can't work due to an injury (as opposed to a specific illness), critical illness insurance will not pay benefits. Alternatively, you might have a critical illness that does not prevent you from working. In this case, the lump sum from a critical illness policy can help cover costs, while a disability policy might not pay anything.

Managing What's Meaningful to You

You can manage the financial impact of illness and injury in several ways. When you understand the difference between critical illness and disability income insurance, you can choose which risks are most concerning to you and pick the coverage that makes the most sense. You might consider speaking with a financial representative to help identify the best path for you.

Critical illness and disability income insurance offer tailored support for health-related income needs. Get My Free Financial Review