You’ve reached retirement, your working years are behind you, and you’re no longer covered by an employer policy. So, do you still need life insurance? The answer depends on your goals, your financial responsibilities, and how much you want to leave behind.

Life insurance for retirees isn’t just about replacing income. It can help cover final expenses, help protect your estate from taxes, support a surviving spouse, or leave a legacy. With the right policy, you can help ease potential financial burdens on your loved ones.

What Is Life Insurance for Retirees?

At its core, life insurance for retirees is coverage designed to pay a death benefit to your beneficiaries after you're gone. But it can do more than that. It can serve as a financial safety net, an estate planning tool, or even a strategic method for tax planning depending on how it’s structured.

Common Uses:

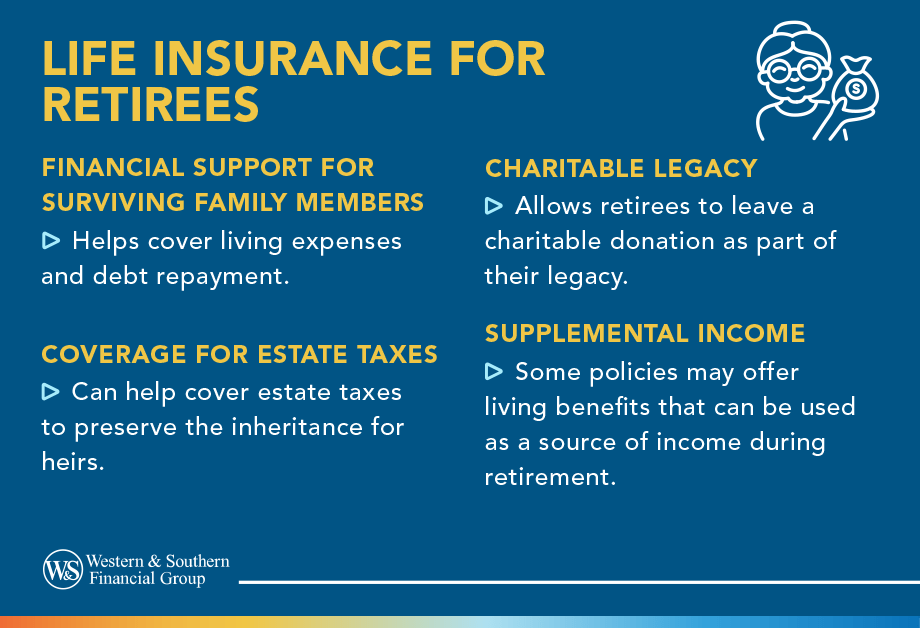

- Pay for final expenses, such as funeral costs, medical bills, and outstanding debts

- Leave an inheritance or charitable gift to a family member or organization

- Cover estate taxes or create liquidity for illiquid assets like real estate or collectibles

- Replace spousal income, especially important if a surviving spouse relies on your Social Security or pension

- Avoid forcing heirs to sell off assets in a market downturn just to settle debts or taxes

Why It’s Different After 65

By the time you retire, your mortgage might be paid off, your kids are likely grown, and your major financial obligations have changed. But the need for a life insurance policy may remain—especially if you want to protect your retirement accounts or avoid burdening your loved ones.

Types of Life Insurance for Retirees

Term Life Insurance

Term policies provide coverage for a set number of years (10, 15, or 20 years). These are often less expensive but expire if you outlive the term.

Best for: Retirees seeking temporary, affordable coverage, often to bridge a gap until other assets are sufficient or to cover remaining debts.

| Pros | Cons |

|---|---|

| Lower monthly premium than permanent coverage | No cash value accumulation |

| Simple, straightforward death benefit | Coverage ends at term expiration (many insurers set cutoffs around age 80–85) |

Whole Life Insurance

A permanent life insurance policy with guaranteed cash value growth and a fixed death benefit.

Best for: Retirees with long-term goals, such as wealth transfer, charitable giving, or ensuring that heirs receive a guaranteed lump sum.

| Pros | Cons |

|---|---|

| Coverage lasts your entire life | Higher premium payments |

| Builds cash value that you can borrow against or use later in life. Loans or withdrawals should only be taken in emergency situations and will reduce the death benefit. | Less flexibility if your income changes in retirement |

| Offers surrender value if canceled |

Universal Life Insurance

More flexible than whole life, this option allows you to adjust your premium payments and death benefit.

Best for: Retirees who want permanent insurance but prefer to have options for adjusting coverage as needs change.

| Pros | Cons |

|---|---|

| Lifetime coverage with adjustable features | Requires active management to avoid policy lapse |

| Builds cash value tied to interest rates or market indexes | Growth may slow if interest rates are low or if market performance is poor |

| Greater flexibility for those with variable income streams |

Final Expense Policies

Also known as burial insurance, these basic life insurance plans are small ($5K to $50K) and designed to cover funeral and medical bills.

Best for: Retirees who have no existing policy and want to make sure their final expenses don’t fall on loved ones.

| Pros | Cons |

|---|---|

| Simplified underwriting (some don't require a medical exam) | Limited coverage amount |

| Fast approval | Higher cost per dollar of death benefit |

| Specifically tailored to cover end-of-life costs |

Group Life Insurance for Retirees

Some employers offer optional life insurance or No Reduction policies that extend into retirement. These may reduce the death benefit over time or cease entirely at a certain retirement date.

Best for: Retirees with limited options or who want supplemental coverage in early retirement years.

| Pros | Cons |

|---|---|

| Continuity of coverage from employment | Coverage reductions are common |

| Usually requires no medical exam | Not portable if you switch employers before retirement |

Key Considerations After Retirement

Health & Age (Age 65+)

As you age, insurance gets more expensive. However, there are insurers who cater specifically to seniors with simplified issue policies. Some even offer guaranteed issue plans for those with serious health issues.

Estate Planning Goals

If your estate is likely to be taxed or your heirs could face liquidity issues, a life insurance policy can act as a planning tool. Work with a financial planner or estate attorney to evaluate the need.

Life insurance may help address potential estate planning concerns, such as liquidity or balancing asset distribution. Consult an estate attorney for specific guidance.

Retirement Income & Expenses

Many retirees live on a fixed budget from retirement accounts and Social Security. Adding a high monthly premium can strain finances. Look for balance:

- Avoid excessive insurance coverage

- Make use of cash value from existing policies if needed

Tax Considerations

Life insurance proceeds are generally not subject to federal income tax. However:

- Policies classified as modified endowment contracts (MECs) may incur taxes on withdrawals

- State rules regarding estate taxes can differ significantly

When Might You No Longer Need Life Insurance?

As you transition deeper into retirement, your financial situation may change to the point where life insurance is no longer necessary. It's a question worth asking periodically: Do I still need this coverage?

You might not need life insurance if:

- Your debts are fully paid, including mortgages, personal loans, and credit cards

- You have ample liquid assets to cover final expenses such as funeral and medical costs

- Your surviving spouse has sufficient income from retirement accounts, Social Security, or pensions

- Your children are financially independent and don’t rely on your support

- You have no dependents with special needs or long-term care requirements

- You no longer have a desire to leave a lump sum or legacy to heirs or a charitable organization

- Your estate is unlikely to be subject to estate taxes, or you have other tools in place to manage estate planning

Actionable Steps to Take Now

- Review Existing Policies

- Do you have term life insurance expiring soon? Review expiration dates and explore conversion options to permanent coverage before it’s too late.

- Is there unused cash value in an old whole life policy? Consider borrowing from or cashing out if the policy no longer serves its original purpose.

- Assess Needs with an Insurance Calculator

- Calculate how much coverage you need by adding up debts, burial costs, income replacement for your spouse, and any intended gifts or estate needs.

- Don’t forget to subtract your existing assets—your goal is to cover the gap, not duplicate coverage.

- Compare New Policies

- Look into senior-friendly life insurance options, such as final expense policies or guaranteed issue policies for those with medical concerns.

- Get quotes from multiple carriers to compare premium rates, coverage duration, and underwriting requirements.

- Use online tools to compare features side by side and estimate costs.

- Check Retiree Benefits

- Contact your former employer's HR or benefits department to learn if any optional life insurance, group life insurance, or travel assistance is still available to you as a retiree.

- If you’re eligible for No Reduction life insurance policies, make sure you understand how benefits will change over time.

- Update Beneficiary Designations

- Major life changes like divorce, remarriage, or the death of a loved one should trigger a beneficiary review.

- Keep retirement accounts, insurance policies, and transfer on death accounts aligned with your estate plan to avoid probate complications.

- Explore 1035 Exchange Opportunities

- If you have an older, expensive policy, a 1035 exchange lets you transfer cash value into a new, more cost-effective policy without triggering taxes.

- Great option for consolidating multiple small policies or switching to more flexible options like universal life insurance.

- Work With a Financial Professional

- A licensed financial advisor can help ensure your coverage aligns with your broader retirement and estate planning goals.

- They can also help determine if you're underinsured, overinsured, or paying too much for too little benefit.

- Consider Alternative Protection

- If you find that traditional life insurance no longer meets your needs, consider other protective options such as:

- Long-term care insurance

- Deferred annuities

- Living benefits riders that allow early access to the death benefit

- If you find that traditional life insurance no longer meets your needs, consider other protective options such as:

By taking a proactive approach now, you can avoid overpaying for coverage you no longer need, or worse, leaving your loved ones without the protection they may count on. Payment of Accelerated Death Benefits, if not repaid, will reduce the death benefit and may affect policy values. These benefits may be taxable or impact eligibility for government programs. Consult your tax advisor.

Final Thoughts

Life insurance for retirees isn’t one-size-fits-all. It depends on your financial situation, estate plans, and legacy goals. For some, insurance is no longer needed. For others, it may still play an important role in your financial strategy during retirement.

Take time to review your existing policies, estimate your needs, and speak with a financial advisor. Whether you're planning to leave a lump sum legacy or just want to cover your final expenses, there's likely a policy that fits.

Choose life insurance to protect your family from unforeseen financial strains. Get a Free Life Insurance Quote