How Per Stirpes Works

Per stirpes is a legal term used in estate planning and inheritance law. It refers to a method of distributing an estate in which assets are divided equally among family branches.1

Under the per stirpes approach, if a beneficiary dies before the testator (the person who created the will), that beneficiary’s share of the inheritance is not lost. Instead, it's divided equally among their descendants.

This distribution method helps a deceased beneficiary’s descendants receive their intended share while maintaining the inheritance structure originally outlined by the testator.

A per stirpes designation can apply to several areas of estate planning, including wills and trusts.

Example Comparing Per Stirpes Vs. Per Capita Inheritance

Sheila has three children: Brian, Chloe and Daniel.

- Brian has two children: Emma and Frank

- Chloe has no children

- Daniel has one child: Grace

Sheila names Brian, Chloe, Daniel, Emma, Frank, and Grace as beneficiaries. Before Sheila passes away, Daniel dies.

Per Stirpes Distribution

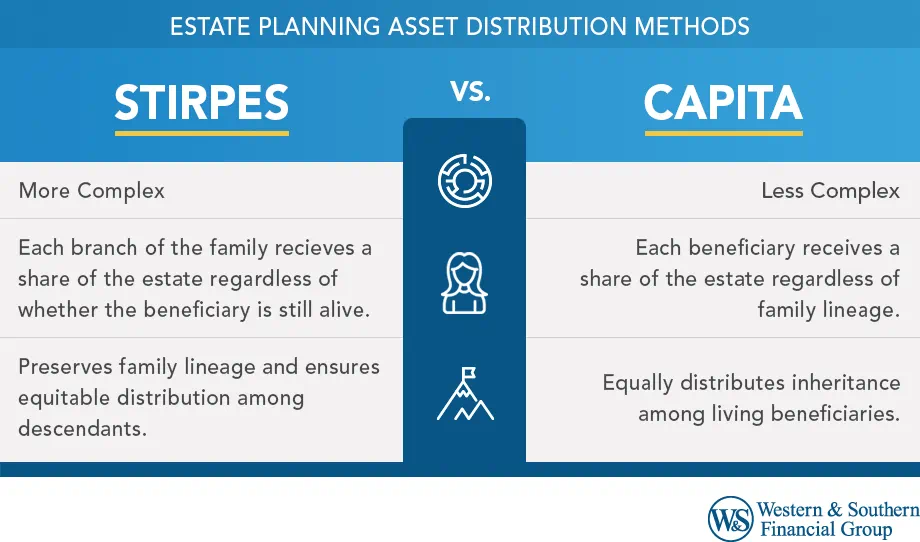

Per stirpes is a Latin phrase meaning “by the roots” or “by the branch.” It's a method of inheritance distribution that passes assets through family lines if a beneficiary dies before the person leaving the estate.2 This method focuses on keeping each branch of the family represented.

Here is how the distribution works.

Sheila’s estate is first divided into three equal shares for her children: Brian, Chloe and David.

| Beneficiary | their children | Per Stirpes Distribution |

|---|---|---|

| Brian | Emma and Frank | 1/3 of estate goes to Brian |

| Chloe | None | 1/3 of estate goes to Chloe |

| David | Grace | 1/3 of estate goes to Grace |

Since David predeceased Sheila, his distributions would then go to his children. Since he has only one child, Grace, she would receive the distribution from Sheila’s estate. Emma and Frank, who are Brian’s children, would not receive a direct share from Sheila’s estate.

Per Capita Distribution

Per capita is a Latin phrase meaning “by the head” or “per person.” This method divides the estate equally among the surviving named beneficiaries, regardless of family branch.2 It's generally simpler to administer than per stirpes distribution.

Here is how the distribution works:

Sheila originally named six beneficiaries: Brian, Chloe, Daniel, Emma, Frank, and Grace.

| Beneficiary | Relationship to Sheila | Per Capita Distribution |

|---|---|---|

| Brian | Child | 1/5 of the estate |

| Chloe | Child | 1/5 of the estate |

| Daniel | Child | Doesn't receive share |

| Emma | Daniel's child | 1/5 of the estate |

| Frank | Brian's child | 1/5 of the estate |

| Grace | Brian's child | 1/5 of the estate |

Since Daniel passed away before Sheila, the estate is divided among the five surviving beneficiaries. Daniel’s share is not passed directly to Grace. Instead, it is redistributed equally among the remaining beneficiaries.

Key Differences

Under per stirpes distribution, the estate follows family branches, so Daniel’s share passes to his child, Grace.

Under per capita distribution, the estate is divided equally among the surviving beneficiaries. As a result, Brian, Chloe, Emma, Frank, and Grace each receive the same share.

Does Per Stirpes Include the Spouse?

No, per stirpes distribution does not generally include the surviving spouse. This is because per stirpes distribution mainly focuses on passing assets through the deceased person's family line, including children, grandchildren, and other direct descendants.

The surviving spouse is not considered a lineal descendant. Instead, they are usually treated as a separate heir under intestate succession laws or the terms of a will. Their inheritance is often handled separately from the per stirpes distribution to help them receive the share of the estate they are entitled to.

Does Per Stirpes Include Stepchildren?

Per stirpes distribution excludes stepchildren unless the testator legally adopts them because stepchildren are not legally recognized as the testator’s lineal descendants. Lineal descendants, such as children, grandchildren, and great-grandchildren, are directly descended from the testator.

Pros: Benefits of Per Stirpes Distribution

Per stirpes distribution in estate planning offers several benefits:

- Consistency Across Generations: Per stirpes helps make sure that a deceased beneficiary's descendants still receive a share of the estate. This approach maintains consistency by helping each branch of the family receive its intended portion of the estate, even if the original beneficiary has passed away.

- Prevents Disinheritance of Grandchildren: In cases where a beneficiary, such as a child of the deceased, dies before the testator, per stirpes helps prevent the unintentional disinheritance of that beneficiary’s children, who may be the testator’s grandchildren. It allows the deceased beneficiary’s share to pass to their descendants.

- Reflects the Testator's Wishes After Death: Per stirpes helps carry out the testator’s wishes as closely as possible, even if the family structure changes because of a beneficiary’s death.

- Simplifies Estate Planning for Large Families: For testators with large families, per stirpes provides a straightforward way to divide an estate without needing constant updates to a will or trust as family circumstances change, such as births, deaths, or marriages.

- Reduces Conflicts Among Heirs: Per stirpes may help reduce conflicts among heirs by clearly explaining how assets will be distributed if a beneficiary dies before the testator. The distribution rules are based on family lineage and are clearly outlined.

- Flexibility in Estate Distribution: Per stirpes allows the distribution of assets to adjust automatically based on the living descendants of the original beneficiaries. This approach may be helpful in changing family situations.

Overall, per stirpes distribution can help support an equitable division of an estate, reflect the testator’s wishes, reduce potential family conflicts, and provide clarity and simplicity in estate planning, especially for complex family structures.

Cons: Drawbacks of Per Stirpes Distribution

While per stirpes distribution in estate planning has benefits, it also has certain drawbacks:

- Potential for Unequal Distributions: Per stirpes can lead to unequal distributions among grandchildren. For example, if one beneficiary has more children than another, the deceased beneficiary's share may be divided into smaller portions for each child compared to cousins whose parents had fewer or no additional children.

- Complexity in Large Families: Per stirpes can become complicated in families with many descendants, especially when multiple generations are involved. Tracking family lineage and dividing the estate correctly can be difficult.

- May Not Reflect Current Relationships: Per stirpes does not consider the relationship between the testator and their descendants. A grandchild the testator never knew or had a close relationship with could inherit a large portion of the estate, while closer family members may receive less.

- Inflexibility With Changes in Family Dynamics: Although per stirpes provides a clear structure, it does not easily adapt to changes in family relationships or the testator's wishes after a will or trust is created.

- Possibility of Minor Beneficiaries: Per stirpes can result in minors inheriting property, which may require trusts or guardianships to manage the assets. This can increase administrative responsibilities and costs.

- Not Suitable for All Estate Plans: Per stirpes may not work well for every estate plan, especially when the testator wants to distribute assets based on personal relationships or individual needs instead of family lineage.

Understanding these drawbacks can help individuals decide whether per stirpes distribution matches their goals and family situation when creating an estate plan.

Is Per Stirpes Distribution Right for You?

Determining whether per stirpes distribution is a good idea involves considering several factors:

- Family Structure and Size: Per stirpes is often suitable for those with a clear family tree and a desire to keep the estate within the family line. If you have multiple children and grandchildren, per stirpes can help make sure each family branch is treated equally.

- Generational Concerns: If you expect your children's needs or circumstances to vary greatly and want to help make sure the surviving descendants of a deceased child are not left out, per stirpes may be a good option.

- Relationship Dynamics: Consider your relationships with potential beneficiaries, as per stirpes may not work well if you want to distribute your assets unevenly among individuals.

- Future Changes in the Family: Consider future changes such as births, deaths, and marriages. Per stirpes can simplify estate matters during these changes because it automatically adjusts to the family structure at the time of your passing.

- Administrative Simplicity: While per stirpes can simplify distribution, it may become more complex in large families. Consider whether your estate executor can manage this type of distribution.

- Legal and Tax Implications: Understand the legal and tax implications of a per stirpes distribution, as it may affect estate taxes or the creation of trusts for minor beneficiaries.

- Your Estate Goals: Think about your overall goals for your estate. If equal distribution across family branches is important to you, per stirpes may be a suitable option.

- Consultation With Professionals: Speak with estate planning attorneys and financial professionals. They can provide guidance about your situation and help determine whether per stirpes aligns with your estate goals.

Final Thoughts

Ultimately, deciding whether per stirpes distribution is right for you depends on your family circumstances and estate goals. It's a decision that should be made after careful consideration and consultation with a qualified estate planning attorney. This can help make sure your estate is distributed according to your wishes and supports your heirs in the way you intend.

Sources

- American Bar Association - Glossary of Estate Planning Terms. https://www.americanbar.org/groups/real_property_trust_estate/resources/estate_planning/glossary/#P.

- Per Stirpes vs. Per Capita in a Will: Understanding the Distinction. https://www.plannedgiving.com/per-stirpes-vs-per-capita-in-a-will-understanding-the-distinction/.