Understanding Wills

A will is a legal document outlining how you want your assets distributed after death. It also allows you to name a guardian for minor children and an executor to manage your estate.1

The key benefits include simplicity in setup, clear direction for the distribution of assets, and the ability to nominate guardians. However, limitations involve going through the probate process, which can be time-consuming and costly, and the public nature of probate, which lacks privacy for the estate's details.

Understanding Trusts

A trust is a legal arrangement in which a third party (trustee) holds and manages assets on behalf of beneficiaries, offering a way to control when and how your assets are distributed.2

Trusts can take different forms, such as:

- Living trusts are created while you are alive.

- Testamentary trusts are created through your will after death.

- Revocable trusts can be changed during your lifetime.

- Irrevocable trusts generally cannot be changed once established.

Key benefits include avoiding probate, providing for minors or special needs beneficiaries, and potentially reducing estate taxes. However, limitations include the complexity and cost of setting up and maintaining a trust and the irrevocable nature of certain trusts, which limits flexibility in changing the trust terms or beneficiaries after it is established.

Several types of trusts are commonly used as estate planning tools, including charitable trusts (charitable remainder trust, charitable lead trust), special needs trusts, spendthrift trusts, and life insurance trusts. The type of trust right for you will depend on your wishes and financial priorities.

Key Differences Between a Will vs Trust

When comparing a will and a trust, several differences affect how each is used:

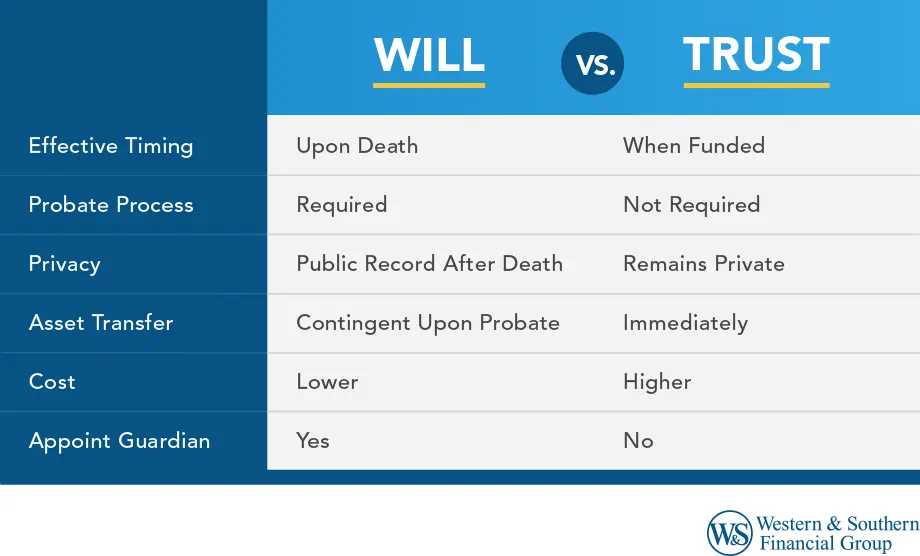

- Effective Timing: A will takes effect only after your death, while a trust can take effect as soon as you create and fund it.

- Probate Process: Assets distributed through a will must go through probate court, which is a public and often lengthy legal process that can be costly. Trusts allow assets to bypass probate, offering a more private and faster way to manage and distribute assets.

- Privacy: Wills become public records once they enter probate, which means the details of the estate are accessible to anyone. Trusts remain private documents, and their terms and assets are not made public through court proceedings, such as family businesses and real estate holdings.

- Control Over Distribution: Trusts offer more flexibility and control over how and when assets are distributed to beneficiaries. Wills provide a one-time distribution after probate is complete, with less ability to set conditions over time.

- Complexity and Cost: Creating and funding a trust is usually more complex and may cost more upfront than creating a will. However, avoiding probate may reduce costs and delays later on.

- Guardianship: Only a will can appoint guardians for minor children, which makes it an important document for parents, even if they also have a trust.

- Types of Assets Covered: Trusts only control assets that have been formally transferred into the trust. A will can cover any property that is solely in the deceased person's name at the time of death.

- Tax Implications: Wills do not usually provide direct tax advantages. Certain types of trusts may help reduce estate or inheritance taxes.

Each tool has its place in an estate strategy, and many people use both to address different needs and types of assets so their wishes are clearly carried out.

When to Choose a Will or Trust?

Scenarios Where a Will Is Sufficient

A will can be a straightforward option for estate planning, especially when your needs are simple and your goals are clear. In many cases, it provides enough structure without added complexity.

Here are situations where a will may be enough:

- Smaller estates: If your estate falls below your state’s probate threshold, a will may be all you need. Some states offer simplified probate for smaller estates, which can make the process easier and less costly.

- Direct and simple bequests: If you plan to leave everything to a spouse or divide assets equally among children, a will can handle this without the added structure of a trust.

- Nomination of Guardians for Minor Children: For individuals or couples with minor children, a will is required for appointing guardians. This is one of its most important functions and cannot be done through a trust alone.

- Individuals with Limited Assets: If you have a smaller estate and want to pass along personal items or modest amounts of money, a will can clearly outline those wishes.

- Situations that Benefit from Probate Oversight: Probate court oversight can help when disputes are likely or when the executor needs clear authority to act. A will provides a structured process for resolving these issues.

- Preference for Simplicity and Lower Upfront Cost: A will is generally easier and less expensive to create than a trust. This may appeal to those who want a simple approach.

- Clear Debt Situations: If your estate includes debts, probate can help manage creditor claims in an orderly way before assets are distributed to heirs.

Situations Where a Trust is Preferable

A trust may be a better fit when your estate involves more complexity or when you want greater control over how assets are managed and distributed.

Here are common scenarios where a trust may be more suitable:

- Avoiding Probate: Assets held in a trust pass directly to beneficiaries without going through probate. This can speed up the distribution process and reduce delays.

- Privacy Concerns: A will becomes public during probate, while a trust remains private. This can help keep details about your estate confidential.

- Managing Assets for Minor Beneficiaries: A trust allows you to set terms for how and when assets are distributed, such as releasing funds at certain ages or milestones.

- Owning Property in Multiple States: A trust can help avoid separate probate proceedings in each state where property is owned, which can simplify the process.

- Planning for Incapacity: A trust allows a successor trustee to manage your assets if you become unable to do so, without court involvement.

- Tax Considerations: Certain trusts can help reduce federal estate taxes for larger or more complex estates.

- Providing for a Beneficiary with Special Needs: A special needs trust can support a beneficiary with disabilities while helping preserve eligibility for government benefits.

- Protection from Creditors or Divorce: Trusts can offer a level of protection by limiting access to assets, which may help shield them from creditors or division in a divorce.

- Complex Family Situations: Trusts can provide more control in blended families or when you want to set specific conditions for inheritance.

- Business Succession Planning: A trust can help transfer business ownership smoothly, helping reduce delays that could affect operations.

Choosing between a will and a trust depends on your goals, the size and structure of your estate, and how much control you want over asset distribution. Consulting an estate planning professional can help you decide which approach fits your situation.

Can You Use Both a Will & Trust?

In many cases, using both a will and a trust can create a more complete estate plan. Each serves a different purpose and can work together to cover important details.

A trust helps manage and transfer assets efficiently:

- Allows assets to pass more quickly

- Helps avoid probate

- Supports ongoing management of assets if needed

A will addresses areas a trust does not cover:

- Naming guardians: A will lets you choose legal guardians for minor children

- Executor appointment: You name someone to handle your estate

- Unassigned assets: A pour-over will directs any assets not placed in the trust to be transferred after your death

- Specific instructions: You can outline funeral wishes or leave personal items to certain individuals

How They Work Together

A well-structured estate plan often includes both a revocable living trust and a pour-over will. This combination helps your assets transfer smoothly, including financial or retirement accounts that may not have been moved into the trust during your lifetime.

Working with an estate planning attorney can help you choose the right approach. They can review your situation and build a plan that reflects your goals, whether that includes a will, a trust, or both.

Conclusion

Estate planning gives you control over how your assets are handled. Understanding how wills and trusts work can help you make informed decisions about your legacy. Whether you choose one or both, taking steps now can help your wishes be carried out as intended.

Sources

- American Bar Association - Introduction to Wills. https://www.americanbar.org/groups/real_property_trust_estate/resources/estate-planning/intro-wills/.

- Legal Information Institute, Cornell Law School - Trust. https://www.law.cornell.edu/wex/trust.