After years of public service or non-profit work, your 457(b) plan is a crucial retirement asset. Its rules, especially for distributions after separation from service, differ from 401(k)s or 403(b)s. Grasping these differences is vital for a smooth transition.

What Makes 457(b) Plans Different in Retirement

A 457(b) is a deferred compensation plan. Traditionally, contributions are pre-tax, meaning funds and earnings are taxed upon withdrawal in retirement. Many plans now also offer a Roth 457(b) option, where contributions are after-tax, allowing for potentially tax-free qualified distributions in retirement.

Governed by Section 457 of the Internal Revenue Code, the Internal Revenue Service provides guidelines for both traditional and Roth 457(b) options.

There are two main types of 457(b) plans:

- Governmental 457(b) Plans: Offered by state/local governments. Assets are held in trust, offering more flexibility and protection. Can include traditional and Roth 457(b) options.

- Non-governmental 457(b) Plans (Tax-Exempt Plans): For non-profits. Assets remain employer property until paid and are subject to employer creditors, making plan sponsor stability a key concern. These are often unfunded.

Throughout your career, you've made contributions (pre-tax or Roth), possibly with Employer contributions (always pre-tax). An individual contribution limit (covering both traditional and Roth) is set annually by the Internal Revenue Service, sometimes with a separate employer contribution limit. Catch-up contribution provisions may also be available near retirement.

Accessing Your 457(b) Funds When You Retire

Accessing your 457(b) plan funds typically requires separation from service from your plan sponsor.

Distribution Options

A key feature of 457(b) plans is penalty-free distributions upon separation from service, regardless of age (unlike the 10% early withdrawal penalty before 59 ½ in many other plans). This applies to both traditional and Roth 457(b) funds. Traditional distributions are taxed as ordinary income tax rates; qualified Roth distributions are tax-free.

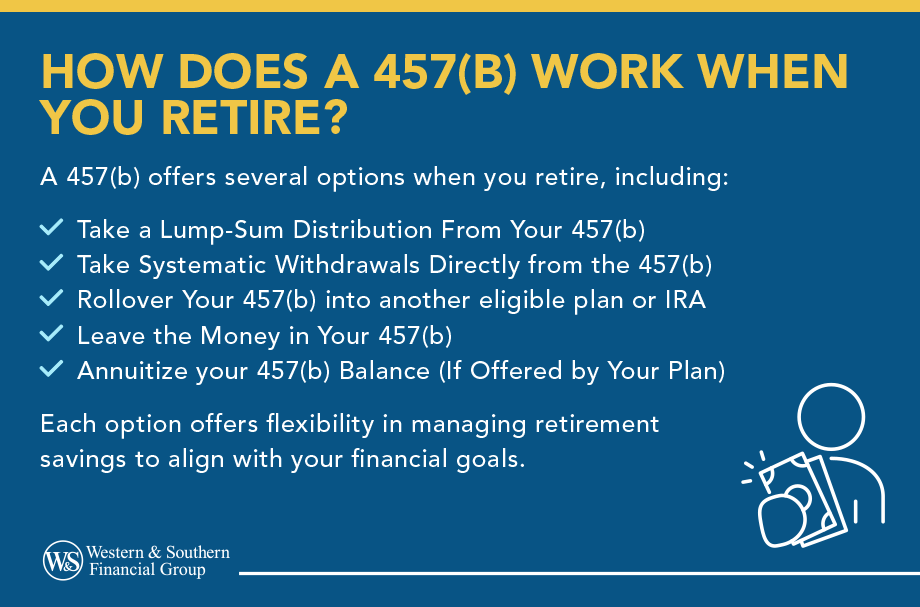

Common distribution methods for your 457(b) when you retire:

- Lump-Sum Distribution: Take all funds at once.

- Traditional: Can cause significant income tax impact.

- Roth: Tax-free if qualified.

- Periodic Payments (often referred to as a Systematic Withdrawal Plan): Receive funds in installments (monthly, quarterly, annually).

- Traditional: Creates a taxable income stream.

- Roth: Tax-free if qualified periodic payments.

- Rollovers: Move assets to another eligible retirement plan.

- Traditional Governmental 457(b): To traditional IRA, 401(k), 403(b), or another governmental 457(b).

- Roth Governmental 457(b): To Roth IRA, Roth 401(k), or Roth 403(b).

- Non-governmental 457(b) (typically pre-tax): Highly restricted; usually only to another non-governmental 457 plan.

- Leave Funds in the Plan: Potentially allow funds to continue growing (tax-deferred for traditional, tax-free for Roth). Subject to Required Minimum Distribution (RMD) rules (verify current RMD rules for Roth 457(b)s, as they may differ for owners).

- Annuitization: Convert some or all of your account balance into a guaranteed stream of income payments for a set period or for life by purchasing an annuity. Availability depends on the specific 457(b) plan.

- Traditional: Annuity payments from pre-tax funds are generally fully taxable as ordinary income.

- Roth: If the Roth 457(b) funds used to purchase the annuity were from a qualified Roth account and the distribution rules are met, a portion or all of the income payments may be tax-free. Specific tax rules for Roth annuity payouts should be verified.

The "No Early Withdrawal Penalty" Advantage

The absence of the 10% early withdrawal penalty on 457(b) distributions after separation from service (before age 59 ½) is a major benefit. If you retire at 55, you can access these funds without this extra penalty.

How Your 457(b) is Taxed in Retirement

Tax implications for your 457(b) when you retire depend on whether funds are traditional pre-tax or Roth 457(b).

Traditional Pre-Tax 457(b) Funds:

- Ordinary Income Tax: Contributions were pre-tax, so all distributions (contributions and earnings) are taxed as ordinary income in the year received, added to other income sources.

Roth 457(b) Funds:

- Tax-Free Qualified Distributions: After-tax contributions mean qualified distributions are tax-free. Conditions:

- Five-year holding period (starts Jan 1st of your first Roth contribution year to that plan).

- Distribution after age 59 ½, disability, or death.

- Non-Qualified Distributions: Earnings portion is taxable as ordinary income and may face a 10% penalty if taken before 59 ½ (though 457(b) separation from service rules might still waive the penalty on early withdrawals; earnings would still be taxed if non-qualified, verify with an advisor). Your Roth contributions are always withdrawn tax-free.

Required Minimum Distributions (RMDs)

- Traditional Pre-Tax 457(b): RMDs generally start by April 1st of the year after you turn 73.

- Roth 457(b): Recent legislation (like SECURE 2.0 Act) suggests RMDs may not be required for original owners during their lifetime, similar to Roth IRAs. Verify current RMD rules with your plan sponsor or advisor. Beneficiaries have their own RMD rules.

Making Your 457(b) Work Harder for You

Integrate your 457(b) when you retire (traditional or Roth) with your overall financial strategy.

- Coordinating with Other Retirement Accounts: Align 457(b) withdrawals with other retirement accounts (401(k)s, IRAs) and Social Security. If you have both traditional and Roth 457(b) funds, strategic withdrawals can manage taxable income. The no-penalty rule upon separation from service offers flexibility for early retirees.

- The Role of Financial Advisors: Financial advisors can help navigate 457(b) complexities, especially with Roth options and tax rules, optimizing withdrawal strategies.

- Special Considerations for Non-Governmental 457(b) Plans: Assets in a non-governmental 457(b) plan are subject to employer creditors until distributed. These are typically pre-tax with limited rollover options.

The "Age 50 Catch-Up" vs. "Special 457(b) Catch-Up"

These increase contributions (combined traditional/Roth) near retirement:

- Age 50 Catch-Up: For those 50+, allows extra contributions above the standard individual contribution limit.

- Special 457(b) Catch-Up ("Last Three Years"): In the three years before normal retirement age (defined by your plan sponsor), allows potentially even larger contributions (lesser of twice the annual limit, or the basic limit plus prior unused amounts). You can't use both catch-ups in the same year; choose the one allowing a larger contribution.

Maximizing these catch-up contribution options can significantly boost retirement savings.

Pros & Cons of Your 457(b) in Retirement

| Feature | Pros | Cons |

|---|---|---|

| Withdrawal Flexibility | No 10% early withdrawal penalty after separation from service, regardless of age (applies to both traditional and Roth 457(b)). | Traditional distributions taxed as ordinary income tax rates. Non-qualified Roth distributions may have earnings taxed. |

| Tax Treatment | Qualified Roth 457(b) distributions are tax-free. Traditional 457(b) offers tax-deferred growth. | Traditional distributions are fully taxable. Roth 457(b) contributions offer no upfront tax deduction. |

| Contribution Limits | "Special 457(b) Catch-Up" allows higher contributions (combined traditional/Roth) before retirement. | Employer contributions less common than in 401(k)s; always pre-tax. |

| Rollover Options | Governmental 457(b)s (traditional/Roth) roll to respective IRAs or similar employer plans. | Non-governmental 457(b) plans have very limited rollover options. Roth 457(b) typically only in governmental plans. |

| Asset Protection | Governmental 457(b) assets generally held in trust. | Non-governmental 457(b) assets are subject to employer's creditors until paid. |

| Early Retirement | Key income source if retiring before 59 ½ without penalties. | Requires careful planning for taxable income (traditional) and Roth qualified distribution rules. |

| Plan Sponsor Dependence | Investment/distribution options governed by plan sponsor. | Investment choices may be more limited than in an IRA or if you had direct control via a self-directed brokerage account linked to your plan sponsor. |

Conclusion

Your 457(b) plan offers advantages that can significantly enhance your retirement security when properly understood and utilized. The penalty-free withdrawal feature makes these plans especially attractive for government employees and eligible nonprofit workers, offering flexibility that aligns with their financial needs.

Whether you have a governmental plan with maximum flexibility or a non-governmental plan with specific limitations, the key lies in understanding your options and planning accordingly. Take time to review your plan documents, understand your distribution choices, and consider how your 457(b) fits into your broader retirement income strategy.

Actionable Insights:

- Review Your Plan Documents: Well before retirement, get a copy of your 457(b) plan's summary plan description. Understand if a Roth 457(b) option is available, the specific distribution options for both traditional and Roth accounts, any fees, and the "normal retirement age" defined by your plan sponsor.

- Estimate Your Retirement Income Needs: Determine how much income you'll need in retirement and how your 457(b) (both traditional and any Roth 457(b) savings) fits into that picture alongside Social Security, pensions, and other savings.

- Consider Your Tax Situation: Model how different distribution strategies (lump sum vs. periodic payments from traditional vs. Roth 457(b) funds) will impact your taxable income now and in retirement.

- Seek Professional Advice: Don't hesitate to consult with financial advisors or tax professionals. They can provide personalized guidance on your 457(b) when you retire, including strategies for managing traditional and Roth 457(b) accounts, and help integrate it into your overall retirement planning.

Discover optimal strategies for your 457(b) when you retire. Start Your Free Plan

Sources

- IRC 457(b) deferred compensation plans - Internal Revenue Service (IRS). http://www.irs.gov/retirement-plans/irc-457b-deferred-compensation-plans

- Publication 575, Pension and Annuity Income – Internal Revenue Service. https://www.irs.gov/publications/p575

- Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs) (Helpful for understanding Roth distribution rules, which have similarities) – Internal Revenue Service. https://www.irs.gov/publications/p590b

- 457(b) and 403(b) Plans - For Investors - U.S. Securities and Exchange Commission. http://www.investor.gov/additional-resources/retirement-toolkit/employer-sponsored-plans/403b-and-457b-plans