What Are 403(b) & 457(b) Retirement Plans?

Both 403(b) and 457(b) retirement savings plans serve as tax-advantaged retirement savings vehicles designed for specific employee groups, but they operate under different Internal Revenue Service regulations and offer varying benefits.

403(b) Plans: Nonprofit and Education Emphasis

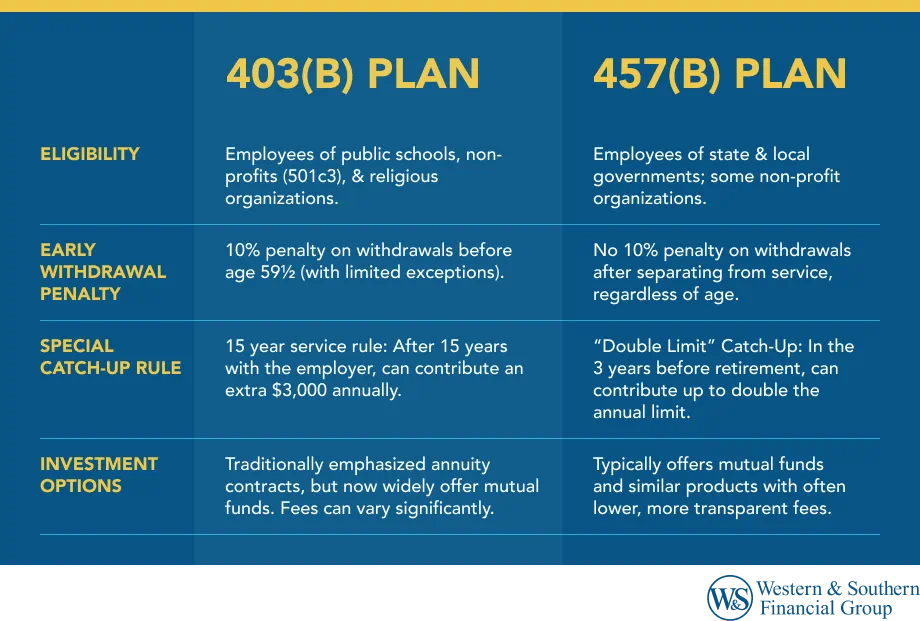

403(b) plans cater specifically to employees of public educational institutions, certain nonprofit organizations, and religious organizations exempt from federal income tax. These retirement accounts, sometimes called Tax-Sheltered Annuities (TSAs), have served educators and nonprofit workers for decades.

Named after Section 403(b) of the tax code, these plans traditionally offered annuity contracts and mutual funds as primary investment options, though modern 403(b) plans have expanded their investment menu significantly.

457(b) Plans: Government Employee Focus

A 457(b) plan primarily serves employees of state and local government entities, including municipalities, school districts, and certain tax-exempt organizations. These retirement plans allow participants to defer compensation into investment products while receiving immediate tax benefits.

The plan derives its name from Section 457(b) of the Internal Revenue Code. Unlike traditional 401(k) plans, 457(b) plans may offer added withdrawal flexibility, which can be beneficial during certain career transitions.

Non-governmental 457(b) plans have different (and often less favorable) rules, and funds are subject to the employer's creditors.

Key Similarities Between Both Plans

It's worth noting the substantial overlap between these retirement plans:

Tax Treatment: Both plans offer tax-deferred growth, meaning pre-tax contributions reduce your current taxable income while investments grow without immediate tax consequences.

Contribution Limits: For 2025, both plans share the same basic contribution limit of $23,500 annually, with identical catch-up contribution provisions for participants over age 50.

Employer Matching: Many employers offer matching contributions for both plan types, though the specifics vary significantly by organization.

Investment Growth: Both plans shelter your investments from annual taxation, allowing compound growth to work more effectively over time.

Critical Differences: Where These Plans Diverge

Eligibility Requirements

The most fundamental difference lies in who can participate. 457(b) plans exclusively serve government employees and workers at qualifying tax-exempt organizations. Meanwhile, 403(b) plans focus on educational institutions, certain nonprofits, and religious organizations.

This distinction matters because it determines which plan you'll encounter based on your career path. Teachers typically access 403(b) plans, while city workers usually participate in 457(b) arrangements.

Early Withdrawal Rules: A Game-Changing Distinction

Perhaps the most significant operational difference involves early withdrawal penalties. This distinction can profoundly impact your financial flexibility.

457(b) Advantage: One major benefit of a 457(b) plan is that early withdrawals typically aren’t subject to the standard 10% IRS penalty that applies to most other retirement accounts. If you leave your employer, you can usually access your funds without paying that early withdrawal penalty, regardless of your age. However, regular income taxes will still apply to the amount you withdraw.

403(b) Limitation: Like 401(k) plans, 403(b) accounts typically subject early withdrawals to a 10% penalty if you're under age 59½, unless you qualify for specific exceptions.

This difference makes 457(b) plans particularly attractive for workers considering early retirement or career changes before traditional retirement age.

Investment Options and Fees

The investment landscape differs notably between these plans:

403(b) Plans: Traditionally emphasized annuity contracts, including fixed annuities, variable annuities, and indexed annuities. Modern 403(b) plans typically offer mutual funds alongside annuity options, though vendor fees can vary significantly.

457(b) Plans: Generally provide broader investment menus focused on mutual funds and similar investment products. These plans often negotiate better fee structures due to their governmental oversight.

Fee Considerations: Both plans can carry substantial fees and expenses, but 403(b) plans historically struggled with higher costs due to their annuity focus. However, recent regulatory changes have improved fee transparency and competition.

Special Catch-Up Provisions

Both plans offer catch-up contributions for older participants, but they handle these differently:

Standard Catch-Up: Participants over 50 can contribute an additional $7,500 annually to either plan type.

403(b) Special Rule: Some 403(b) participants with 15+ years of service can contribute an extra $3,000 annually beyond standard limits, potentially reaching $26,500 in total contributions before age 50. You cannot use both the 15-year rule and the age 50+ catch-up in the same year

457(b) Double Limit: In the three years before normal retirement age, 457(b) participants might contribute up to double the annual limit under specific circumstances.

Tax Implications & Withdrawal Strategies

Current Tax Benefits

Both plans provide immediate tax relief by reducing your current-year taxable income. If you contribute $10,000 to either plan and you're in the 22% tax bracket, you'll save approximately $2,200 in current taxes.

Future Tax Considerations

Your retirement tax rate becomes crucial for both plans. If you expect to be in a lower tax bracket during retirement, these traditional tax-deferred accounts can provide significant long-term tax savings.

However, both plans require minimum distributions starting at age 73, potentially pushing you into higher tax brackets during retirement years.

Cash Withdrawal Strategies

403(b) Restrictions: Early access typically requires hardship provisions or separation from service after age 55, limiting flexibility compared to 457(b) arrangements.

457(b) Flexibility: The absence of early withdrawal penalties makes 457(b) plans valuable for bridge strategies between early retirement and traditional retirement account access.

Common Pitfalls to Avoid

Vendor Fee Traps: Both plans can involve high fees, particularly 403(b) plans. Always review fees and expenses before committing to investment options.

Ignoring Employer Matching: Never leave matching contributions on the table. These represent immediate 100% returns on your investment.

Inadequate Diversification: Whether you choose mutual funds or annuity contracts, ensure your investment strategy aligns with your risk tolerance and time horizon.

Poor Record Keeping: Both plans require careful documentation for tax purposes. Maintain detailed records of contributions, withdrawals, and investment changes.

The Role of Financial Advisors

Given the complexity of both retirement plans, consulting with a qualified financial advisor can prove invaluable. A professional can help you:

- Navigate investment options within your specific plan

- Optimize contribution strategies

- Plan withdrawal timing to minimize tax consequences

- Integrate either plan into your broader retirement strategy

Final Thoughts

The choice between 457(b) vs 403(b) often comes down to your employer and career path rather than personal preference. However, understanding these plans' features helps you maximize whichever option you have available.

Your financial future depends on starting early, contributing consistently, and making informed decisions about the retirement plans available to you. Whether that's a 457(b), 403(b), or both, take action today to help secure your tomorrow.

Explore how these plans can help secure your retirement. Start Your Free Plan

Sources

- Internal Revenue Service Publication 571: Tax-Sheltered Annuity Plans (403(b) Plans) – Internal Revenue Service. https://www.irs.gov/pub/irs-pdf/p571.pdf

- 457(b) Deferred Compensation Plans – Internal Revenue Service. https://www.irs.gov/retirement-plans/non-governmental-457b-deferred-compensation-plans

- Retirement Plan Contribution Limits – Internal Revenue Service. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-contributions

- Early Withdrawal Penalties and Exceptions – Internal Revenue Service. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-tax-on-early-distributions

Footnotes

- Securities offered by Registered Representatives through W&S Brokerage Services, Inc. (W&SBS), member FINRA/SIPC. Advisory Services offered by Financial Advisors through W&SBS, a registered investment advisor. All companies are members of Western Southern Financial Group