Understanding Retirement Plans for Your Business

Most retirement plans available to small business owners fall into four primary categories: SEP IRAs, SIMPLE IRAs, 401(k) plans, and defined benefit plans. Business owners may also contribute to Traditional IRAs or Roth IRAs alongside an employer-sponsored retirement plan, depending on income limits, eligibility requirements, and contribution rules.

Key Factors to Consider

The right retirement solution is not always the one with the highest contribution limit. Business owners should also consider employee eligibility requirements, administrative responsibilities, available tax deductions, and potential tax credits.

Evaluating these factors can help narrow the available retirement savings options and identify a plan that aligns with both business needs and long-term retirement goals.

With these considerations in mind, the following sections examine the most common retirement plan options for small business owners.

SEP IRA Plans

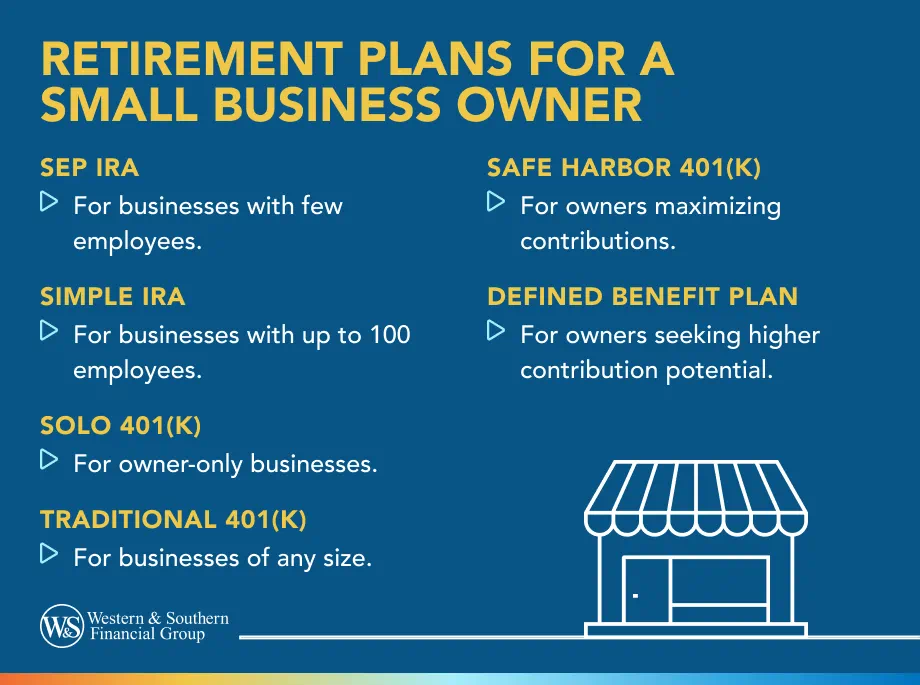

A SEP IRA, short for Simplified Employee Pension, is often used by sole proprietors, freelancers and small businesses with few employees seeking a potential tax advantage. It allows employer contributions to retirement accounts set up for eligible workers.

SEP IRAs are often attractive to sole proprietors and small businesses because employer contributions can vary based on business performance. Employers can decide each year whether to contribute and how much to contribute, subject to IRS limits. This flexibility may be helpful when business income fluctuates.

How a SEP IRA Works

SEP IRA contributions are funded by the employer only, and employees cannot make salary-deferral contributions.1 Employers decide each year whether to contribute and how much to contribute. The business generally contributes the same percentage of compensation for each eligible employee, including the owner.1

Pros and Cons

| Pros | Cons |

|---|---|

| Easy to establish | Employer-funded only |

| Employer contributions may be tax deductible | Costs may rise as staff grows |

| Flexible annual contributions | No employee payroll contributions |

| No annual Form 5500 filing | Equal-percentage contributions can increase costs |

A SEP IRA may work well for a small firm with only a few employees because it is easy to establish and maintain. As the business expands and payroll costs rise, however, the requirement to contribute the same percentage for eligible employees can make other retirement plan options more attractive.

SIMPLE IRA Plans

A SIMPLE IRA is designed for small businesses with 100 or fewer employees that want a straightforward retirement plan with employee contributions and required employer contributions. SIMPLE stands for Savings Incentive Match Plan for Employees.

Many businesses choose a SIMPLE IRA because it can provide a middle ground between a SEP IRA and a traditional 401(k). Unlike a SEP IRA, it allows employee contributions through payroll deductions. It also generally involves fewer compliance responsibilities than many 401(k) plans, making it a practical retirement savings program for small businesses.

How a SIMPLE IRA Works

Employees can contribute a portion of their salary through payroll deductions into Individual Retirement Accounts established under the plan. Employers must also make either matching or non-elective contributions. Eligible participants may also be able to make catch-up contributions based on age, subject to IRS limits.

Pros and Cons

| Pros | Cons |

|---|---|

| Easy to implement | Lower contribution limits |

| Employee payroll contributions | Employer contributions required |

| Employer match or non-elective contributions | Eligibility and withdrawal rules |

| Lower admin complexity | Early withdrawals may trigger taxes and penalties |

A SIMPLE IRA may be a practical option for small businesses that want to offer a workplace retirement plan without some of the complexity associated with a traditional 401(k).

401(k) Retirement Plans

Among retirement options for a small business owner, the 401(k) plan often provides the greatest flexibility and contribution potential. Business owners can choose among several structures depending on company size and objectives.

Several types of 401(k) plans are available to small business owners, each with different contribution opportunities and administrative requirements.

Traditional Small Business 401(k) Plans

A traditional small business 401(k) plan allows employees to contribute through payroll deductions, and employers may also make matching or profit-sharing contributions.2 Plans may include features such as Roth contributions and participant loans.

- Pros: Higher contribution opportunities; flexible plan design

- Cons: Administrative requirements; possible testing and filing obligations

Solo 401(k) Plans

A Solo 401(k) is designed for self-employed individuals and owner-only businesses. Owners may contribute as both an employee and employer, subject to IRS limits.2

- Pros: High contribution potential; designed for owner-only businesses

- Cons: Not available once eligible common-law employees are hired

Safe Harbor 401(k) Plans

A safe harbor 401(k) plan uses required employer contributions to help satisfy certain nondiscrimination testing requirements.2 This structure can help business owners maximize contributions while simplifying certain testing requirements.

- Pros: Simplifies certain testing requirements; supports higher employee deferrals

- Cons: Required employer contributions

Profit-Sharing Contributions in a 401(k) Plan

Profit-sharing contributions are employer contributions that can be added to a 401(k) plan. Despite the name, they do not require the business to generate profits in a given year. This approach allows employers to make discretionary contributions to help owners and employees build retirement savings.

- Pros: Flexible employer contribution strategy

- Cons: Requires thoughtful plan design and ongoing administration

Defined Benefit Plans

Defined benefit plans, often referred to as traditional pension plans, promise a future benefit based on a formula. They can allow significantly higher contribution opportunities than many defined contribution plans, particularly for high-income business owners who are approaching retirement and want to accelerate retirement savings.

How Defined Benefit Plans Work

A defined benefit plan uses actuarial calculations to determine the contributions needed to fund the promised benefit.1 Because contribution levels are based on projected retirement benefits rather than annual contribution limits alone, some owners may be able to contribute substantially more than under defined contribution plans. The formula may consider factors such as compensation, age, years of service and retirement age.

This type of plan is more complex than a SEP IRA, SIMPLE IRA or 401(k). It may require actuarial services, annual filings and consistent funding. Because of those requirements, it is often used by established businesses with predictable profits.

When To Consider

Defined benefit plans may be worth considering for:

- Business owners seeking higher contribution limits

- Owners approaching retirement who want to accelerate retirement savings

- Businesses with stable cash flow and predictable earnings

- Employers interested in providing a specified retirement benefit

While defined benefit plans may offer substantial contribution opportunities, they also involve ongoing funding obligations and a higher level of administration.

Retirement Plan Contribution Limits

Contribution limits vary by plan type and may change from year to year. While SIMPLE IRAs generally have lower contribution limits than many 401(k) plans, defined benefit plans may allow substantially larger contributions for some business owners.

Contribution Potential by Plan Type

The table below compares contribution potential across common retirement plans.

| Plan Type | Contribution Potential | Administrative Complexity |

|---|---|---|

| SEP IRA | High | Low |

| SIMPLE IRA | Moderate | Low |

| Solo 401(k) | High | Moderate |

| Traditional 401(k) | High | Moderate to High |

| Safe Harbor 401(k) | High | Moderate |

| Defined Benefit Plan | Highest for some owners | High |

While contribution potential is important, it is only one factor when evaluating retirement plans. The next steps can help business owners identify a plan that aligns with their goals and business needs.

Steps to Choose a Retirement Plan for Your Small Business

Selecting the right retirement plan starts with understanding your business's priorities. The following steps can help you compare common options and evaluate which plan may be the most appropriate fit.

Step 1: Define Your Goals

Start by identifying your primary objective. Some business owners prioritize maximizing retirement savings, while others focus on employee benefits, tax advantages or a combination of goals.

Step 2: Consider Your Workforce

Employee count, compensation levels and eligibility requirements can affect both the cost and suitability of a retirement plan. A plan that works well for a sole proprietor may not be the right fit after hiring employees.

Step 3: Evaluate Contribution and Funding Requirements

Consider how much you want to contribute and whether those contributions need to vary from year to year. Some plans offer greater flexibility, while others may require ongoing employer contributions.

Step 4: Understand Administrative Responsibilities

Retirement plans differ in their administrative requirements. Consider responsibilities such as payroll deductions, participant communications, compliance testing, recordkeeping and required filings.

Step 5: Seek Professional Guidance

A tax advisor, plan administrator, ERISA attorney or financial professional can help evaluate plan options, contribution strategies, and compliance requirements. Reviewing your retirement plan periodically can help ensure it continues to align with your business needs as your circumstances evolve.

Conclusion

No single retirement solution is appropriate for every small business owner. The most practical approach is to compare each plan's structure against your workforce, cash flow, tax situation and retirement goals.

With the right guidance, a small business retirement plan can help owners build retirement accounts, provide potential tax advantages, support employees and create a clearer path toward future retirement income.

Sources

- Publication 560 (2025) Retirement Plans for Small Business. https://www.irs.gov/publications/p560

- 401(k) Plan Overview. https://www.irs.gov/retirement-plans/plan-sponsor/401k-plan-overview