The new IRS rules for retirement plans could help boost savers toward their retirement goals. The limits for contributions to 401(k) plans have increased for 2025. Other updates to the rules for individual retirement accounts (IRAs) and other types of retirement accounts may mean significant adjustments for your saving strategy moving forward.

Here are key changes to note about the IRS 2026 limits and new rules for retirement plans.

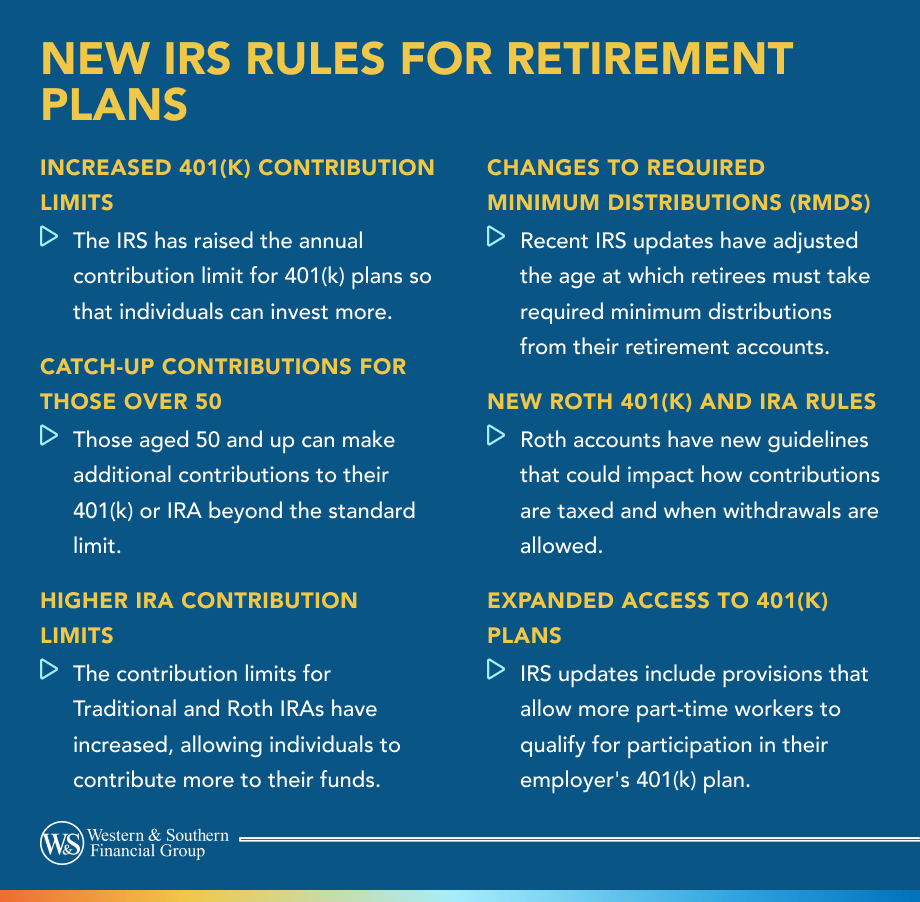

New Contribution Limit for 401(k) Plans

While many expected larger adjustments for 2026, the base 401(k) contribution limit isn’t seeing major movement.1 The maximum contribution amount has increased by $1,000, which means individuals under age 50 can save up to $24,500 in their 401(k) plan this year. The new limit also applies to 403(b) plans, the federal government's Thrift Savings Plan and most 457 plans. Plus, savers who are age 50 or older by December 31 can make annual catch-up contributions up to $8,000 in 2026.

Contribution Limits & Deductions for IRA Plans

The IRS has increased the 2026 contribution limits for IRA plans. Taxpayers can now save up to $7,500 per year in a traditional or Roth IRA, and those age 50 or older can contribute up to $8,600 annually through catch-up contributions.1

However, your IRA contributions you can deduct from your taxes. Once your adjusted gross income for the year reaches a certain amount, your ability to claim IRA contributions as deductions begins to phase out.

Traditional IRAs

Deduction eligibility for contributions to a traditional IRA begins to phase out starting at an adjusted gross income of $129,000 per year for couples filing jointly or $81,000 per year for individuals filing alone or as the head of household.2 This is an increase from $126,000 for joint returns and $79,000 for single returns in 2025.

Roth IRAs

For the 2026 tax year, Roth IRA contribution eligibility begins to phase out at a modified adjusted gross income (MAGI) of $153,000 for single filers and heads of household, with contributions no longer allowed once MAGI reaches $168,000. For married couples filing jointly, the phase-out range starts at $242,000 and ends at $252,000, meaning couples with a MAGI of $252,000 or more cannot contribute. These updated income limits reflect annual inflation adjustments.3

Changes to Other Retirement Plans

The new IRS rules for retirement plans also affect other types of savings accounts this year. For savings incentive match plan for employees (SIMPLE) plans, the contribution limit has increased to $17,000 (up from $16,500 in 2025).2 The contribution limit to simplified employee pension (SEP) plans has increased to $72,000 from $70,000 last year.

Saver's Credit Changes

The IRS's cost-of-living updates for 2026 also affect taxpayers' eligibility for the saver's credit. This tax credit allows some individuals to deduct up to 50% of the contributions to their retirement accounts. This year, households that are married and filing jointly are eligible for the saver's credit if their adjusted gross income does not exceed $80,500 (up from $79,000 in 2025). Individuals qualify if their adjusted gross income is below $60,375 - a limit that applies to both single filers and heads of household (up from $59,250 last year).1

Conclusion

Whether you're saving for retirement through an employer-sponsored 401(k), an IRA or a combination of methods, it's a good idea to consult with a financial professional as you plan for the future.

Adjust your savings strategy to benefit from the latest retirement plan updates. Start Your Free Plan

Sources

- 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500.

- The 2026 Retirement Plan Contribution Limits. https://www.whitecoatinvestor.com/retirement-plan-contribution-limits/.