The fact that women make 77 cents for every dollar a man earns is often cited.1 But what isn't discussed as frequently is how this pay disparity - and gender inequality in general - creates significant differences in a man's versus a woman's ability to retire.

Just like the wage gap, the gender retirement gap is real and poses a persistent problem. Several wide-ranging societal and policy changes must take place to close this gap and address the issues that negatively affect retirement for women. In the meantime, women can take steps in their own lives to help ensure they save enough for retirement. Here's what to know.

What Is the Gender Retirement Gap?

The gender retirement gap is the disparity that exists between men and women both in retirement savings and retirement readiness.

Many Americans face challenges when it comes to saving for retirement. Today, the average American has $87,000 in retirement savings.2 But the gap between men and women remains significant. A look at 2025 Census Bureau data shows the difference:3

| Age 65+ Receiving Retirement Income | Men | Women |

|---|---|---|

| Pensions, 401(k)s, IRAs, and similar sources |

53% | 44% |

This highlights how fewer women in this age group receive income from these key retirement sources.

Factors Driving the Gender Retirement Gap

Unless significant action is taken on a national level, the retirement gap between genders will likely present an ongoing problem for women. This is because various factors contribute to the widening gap in retirement security and retirement readiness.

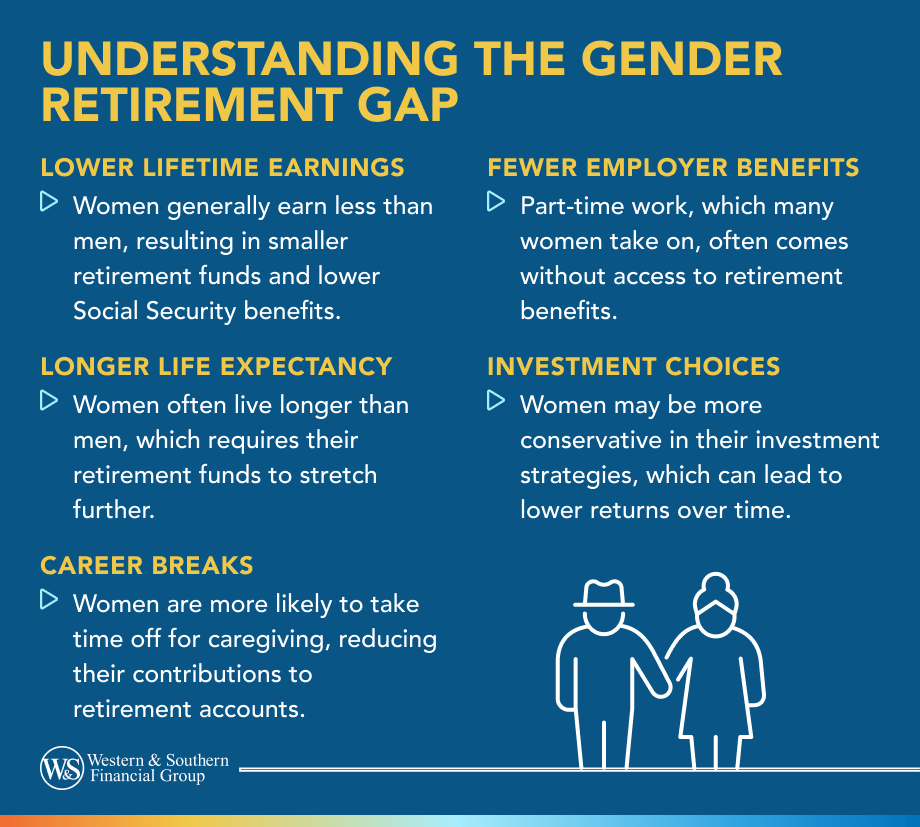

Wage Disparity

The gender wage gap is one of the biggest drivers of the retirement gap. It’s harder for women to save at the same pace as men when they’re earning less for similar work. Even though the gap has narrowed slightly - with women earning 85 cents for every dollar men earn as of late 2025 - lower pay often limits how much women can set aside after covering their living expenses.4

To be clear, the gender wage gap is a complex issue. Discrimination contributes to this disparity, but so do several unique situations women face.

Family Commitments

If a woman decides to have a family, she may spend several months - or even years - away from the workforce. After maternity leave, she might:

- Work part-time

- Scale back her hours to focus on childcare

- Step away from her career entirely if balancing job demands and family needs becomes too difficult

These challenges can be even harder when an employer doesn’t offer enough flexibility for her situation.

We already saw this play out during the pandemic when many women exited the workforce between 2020 and 2023. According to research from the Institute for Women’s Policy Research (IWPR), women’s employment didn’t return to pre-COVID levels until January 2023 - nearly a full year after men’s.5

A big reason: Countless professionals felt forced to quit because they lacked the support needed to juggle remote work, distance learning for their children, and everyday family responsibilities.

Missed Career Opportunities

When women leave the workforce entirely or move in and out of it, they can lose access to career-building opportunities and long-term financial growth. Several challenges may arise:

Career & Earnings Impact

- Missing chances to build new skills that support advancement.

- Being passed over for promotions due to gender bias or concerns about long-term availability.

- Reduced access to higher-paying roles that often come with continuous career progression.

Retirement Savings Impact

- No employer matching contributions during time away from work.

- Lower personal contributions to a 401(k) or individual retirement account (IRA).

Social Security Impact

- Social Security benefits are calculated using a worker’s 35 highest-earning years. Time out of the workforce can:

- Reduce the number of high-earning years used in the formula.

- Result in lower average monthly earnings used to determine benefits.

Longer Life Expectancies

Women also tend to live longer than men. On average, a woman who reaches age 65 lives almost three years longer than a man the same age.6 Though a longer life expectancy is overall a positive thing, it's a double-edged sword when it comes to retirement. A longer life expectancy can be positive, but it also creates challenges in retirement:

- Savings must stretch further. Living longer means retirement money needs to last for more years.

- Health care needs may increase. Additional years often bring higher medical or long-term care costs.

A recent study found that a retired couple need nearly $344,000 for health care expenses in retirement.7 Even if a woman has to cover only half that amount, it could still take up a large portion of her savings.

From less time in the workforce to lower Social Security earnings and longer life expectancy, these factors significantly affect not only women's ability to retire but to do so comfortably. Given the obstacles they face, women must be even more diligent about saving for retirement and following an effective long-term plan.

Close the savings gap by factoring in career and wage challenges in your retirement plan. Start Your Free Plan

6 Strategies Women Can Use to Close the Gap

Women can exert some control in narrowing how the gender retirement gap affects them individually. While significant societal and policy changes may be needed to level the playing field, here are six strategies that can help women build their savings and plan to retire comfortably.

1. Contribute to Your Employer-Sponsored Retirement Plan

If you work and are eligible for a workplace retirement plan - such as a 401(k), 457(b), or 403(b) - this can be a smart time to begin contributing. Even if it feels like you don’t have extra money, small amounts like $25 or $50 a month can make a meaningful difference over time.

Contributing every month to retirement also will get you into the habit of saving. If your employer offers a matching contribution, you avoid leaving free money unclaimed and give your account added potential for growth.

If you’re 50 or older, you may qualify for catch-up contributions, which could allow you to put up to an additional $8,600 per year into your workplace plan, depending on the type of account.8 Another benefit of contributing to your employer's plan is that you may be able to get a tax deduction for your contributions, which could lower your current tax bill and potentially provide a larger refund you could reinvest back into your retirement account.

2. Open a Traditional or Roth IRA

If you’ve maxed out your employer’s plan - or simply want more control over your retirement savings - opening a traditional IRA or Roth may be a helpful next step. Here is a quick comparison of the two IRA types:

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Type of Contributions | Pre-tax dollars | After-tax dollars |

| Tax Treatment Now | Contributions may be tax-deductible based on income9 | No tax deduction for contributions |

| Tax Treatment in Retirement | Withdrawals are taxed as income | Qualified withdrawals are tax-free |

| Contribution Limit | $7,500 (lower than a 401(k)) | $7,500 (same as Traditional IRA) |

| 401(k) Contribution Comparison | 401(k) limit is $24,500 in 20268 | Same comparison applies |

| Investment Options | Wide range: stocks, bonds, mutual funds, index funds | Wide range: stocks, bonds, mutual funds, index funds |

| Early Withdrawal Rules | Taxes and penalties apply if withdrawn early | No penalties if rules are met and withdrawals are after age 59½ |

| Ideal For | Those who want a tax break now | Those who prefer tax-free income later |

3. Talk With a Financial Professional

If you think you could benefit from some guidance, consider talking with a financial professional who can help you craft your unique retirement strategy.

Additionally, many employers now offer financial wellness programs, which allow employees to access financial education for free or discounted rates. If your employer doesn't offer these services, consider talking to a fee-only financial professional who will charge an hourly rate or flat fee based on the services you need.

4. Consider an Annuity

An annuity, which can only be issued by an insurance company, can be used to provide guaranteed income in retirement. With it, you contribute money to a tax-deferred account. Depending on the type of annuity, you also may receive a minimum guaranteed interest rate, which means the money will grow over time.

One thing to keep in mind with an annuity is that, like a 401(k) and a traditional IRA, you'll have to pay taxes on the gains once you withdraw the money. You'll enjoy tax-deferred growth while the money is in the account, but you'll need to factor in future taxes in retirement.

5. Ask for a Raise or Title Change

The job market is booming, and there are more job openings than there are people to fill them.10

If you’re a valued, high-performing employee or have taken on more work in recent years, it’s reasonable to ask for a raise. Replacing employees often costs companies more than retaining them, so it’s usually in an employer’s best interest to help keep you with the organization.11

If a raise isn't possible, ask for a title change. For example: A step up in title from senior manager to director or from coordinator to administrator may help position you for a higher-paying role in a future job search, especially if your employer is unwilling to bump up your pay right now.

6. Consider Long-Term Care Insurance

As mentioned, women often live longer than men, which means they may face higher health care costs in retirement.

To better prepare for this, consider long-term care insurance. Similar to health insurance, you pay a monthly premium for coverage. However, the main difference with long-term care insurance is that you can use this coverage can help pay for long-term care needs, such as:

- Nursing home stays

- Assisted living

- In-home support services

If traditional long-term care insurance feels too costly, a hybrid policy may be an option. It combines life insurance with long-term care benefits. With this approach, you can use a portion of the policy’s death benefit to pay for long-term care costs while you’re still living.

Having a plan to pay for future health care costs is also a critical part of retirement planning, so shop around for quotes to see how much a long-term care policy may cost you. The younger and healthier you are, the more affordable this policy might be, so it's often advantageous to look for a policy as soon as possible.

Shaping Your Retirement Strategy

The gender retirement gap will continue to create differences in retirement for women and men for the foreseeable future. However, women can take steps in their own lives to help address this.

If you have a workplace retirement plan, try to contribute to it early and often. Open a traditional or Roth IRA to increase your retirement savings and gain more flexibility in your retirement planning. Plan to talk with a financial advisor to help ensure you're on the right path, and consider an annuity or long-term care insurance to provide guaranteed income in retirement and to better prepare for future health care expenses. The more you are prepared today, the more financially prepared you'll be tomorrow.

Build a retirement strategy that helps narrow the gender savings gap. Start Your Free Plan

Sources

- Equal pay for work of equal value. https://www.unwomen.org/en/news/in-focus/csw61/equal-pay.

- Average retirement savings in the U.S. https://www.fool.com/research/average-retirement-savings/.

- Retirement Income: Survey of Income and Program Participation Snapshots. https://www.census.gov/content/dam/Census/library/factsheets/2025/demo/p70fs-207.pdf.

- Gender pay gap in U.S. has narrowed slightly over 2 decades. https://www.forbes.com/advisor/business/gender-pay-gap-statistics/.

- New Research Reveals Women’s Progress - and Ongoing Struggles - Since COVID-19. https://iwpr.org/new-research-reveals-womens-progress-and-ongoing-struggles-since-covid-19/.

- Retirement & Survivors Benefits: Life Expectancy Calculator. https://www.ssa.gov/oact/population/longevity.html.

- How to plan for rising health care costs. https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs.

- 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500.

- Individual retirement arrangements (IRAs). https://www.irs.gov/retirement-plans/individual-retirement-arrangements-iras.

- Understanding America’s Labor Shortage. https://www.uschamber.com/workforce/understanding-americas-labor-shortage.

- The Real Cost of Replacing an Employee. https://bloomfire.com/blog/cost-of-replacing-an-employee/.