Retirement readiness looks very different depending on where you live, and if you're actively planning for your golden years, that gap matters. Western & Southern Financial Group looked at all 50 states across five factors (retirement savings, earnings, homeownership, cost of living, and quality of life) to find out which states have residents who are best prepared. Understanding where your state stands is a good starting point for figuring out where your own plan may need work.

Best States for Retirement Readiness

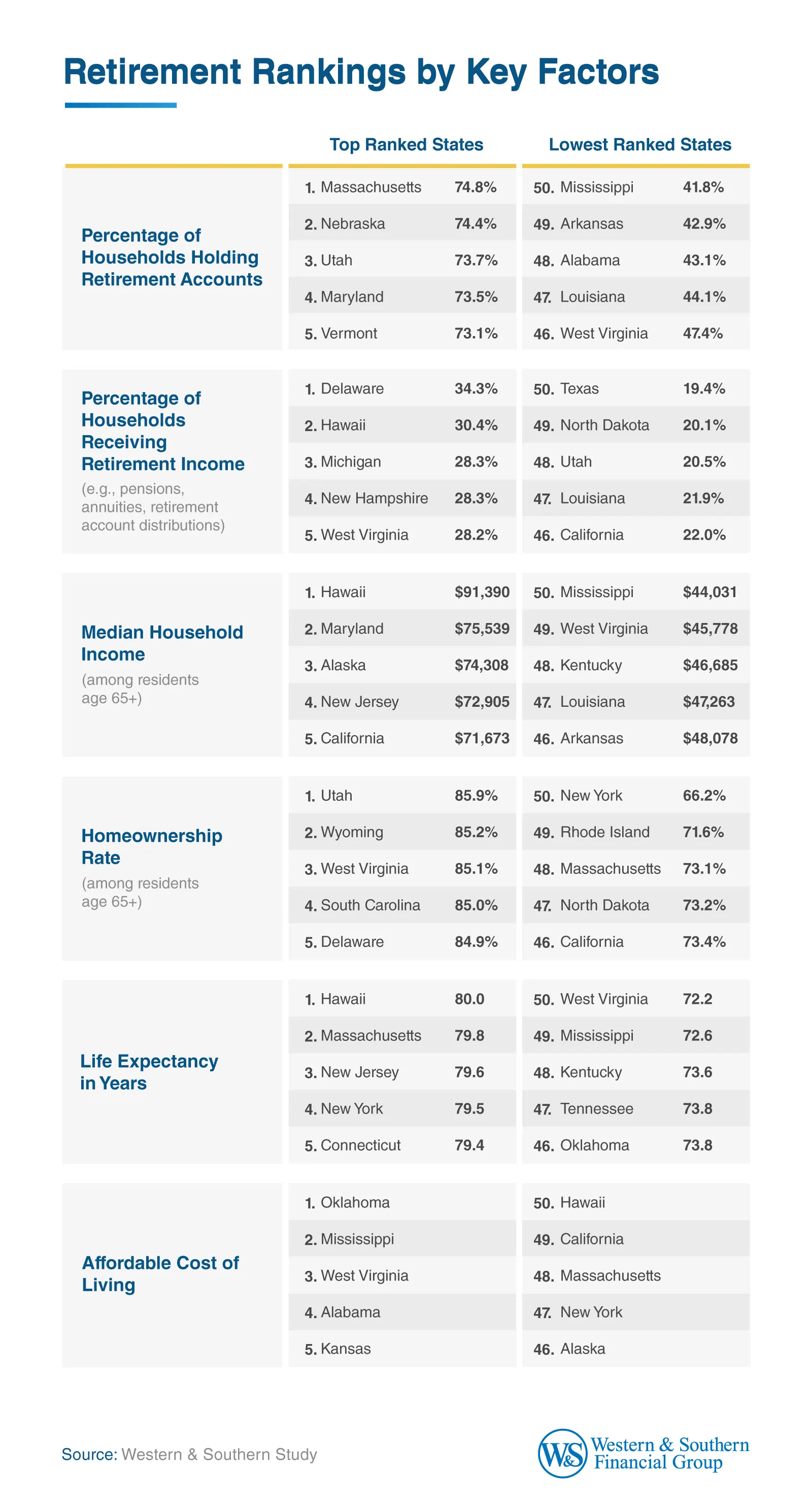

States that rank highly for retirement readiness tend to balance strong savings, stable income, and manageable living costs. However, even top-performing states show that no single factor guarantees overall success.

Delaware stands out as the top-ranked state, supported by the nation's highest share of households receiving retirement income (1st at 34.3%) and a high homeownership rank (5th). In contrast, Louisiana ranks last overall, with weak performance in both retirement savings (49th) and senior income (47th), limiting financial security for retirees.

Other states highlight how uneven these factors can be. For example, Mississippi ranks last in both retirement savings and earnings and is the only state to finish at the bottom in two categories. Yet, it places 8th in homeownership, showing strength in housing stability despite financial gaps. New Jersey performs well in earnings (4th) and quality of life (3rd) but ranks 44th in both homeownership and cost of living, placing it at No. 22 overall.

Strong homeownership alone does not guarantee a high ranking. South Carolina ranks 4th in senior homeownership but 34th in retirement savings, resulting in a No. 29 overall ranking.

What Drives Retirement Readiness

Retirement preparedness depends on a combination of financial resources, affordability, and longevity. States that perform well in one area may still struggle overall if other factors fall short.

West Virginia illustrates this imbalance clearly. The state ranks among the top for senior homeownership (85%) and offers one of the lowest costs of living, yet it falls near the bottom for senior median income ($45,778) and ranks last in life expectancy at 72.2 years.

Hawaii presents the opposite challenge. It leads the nation in median income for seniors ($91,390) and life expectancy (80 years), but its high cost of living reduces how far those earnings can stretch, making it difficult to retire comfortably.

Massachusetts also shows how affordability can offset strong financial habits. The state leads in the share of households holding retirement accounts (74.8%) but ranks among the five least affordable states, limiting the impact of those savings over time.

Preparing for Retirement

Retirement readiness isn't determined by any single factor. Savings, income, housing stability, affordability, and even life expectancy all play a role, and a strength in one area can easily be offset by a gap in another.

Knowing where your state ranks is useful context, but your personal situation, what you've saved, what you owe, and what you expect to spend, matters just as much. If the data here raises questions about your own retirement plan, Western & Southern has retirement planning resources to help you think through the next steps.

Methodology

The 2026 Western & Southern Financial Group Retirement Readiness Index ranked all 50 U.S. states based on the financial, economic, and quality-of-life factors that most directly shape a retiree's ability to maintain long-term security and comfort. Drawing exclusively from publicly available federal datasets, the index provides a data-driven look at where Americans are best and least prepared for retirement.

Data Sources and Factors Considered

The index is built on five core categories, each weighted to reflect its relative importance to financial retirement preparedness. Category weights were updated for 2026 to better reflect the growing impact of regional affordability on retirement security.

Scoring Categories and Weights

Retirement Savings and Benefits — 30 Points

- Percentage of Households Holding Retirement Accounts (20 Points): The share of households that hold a 401(k), IRA, or other retirement account, reflecting the breadth of financial preparation across the state's population.

- Source: U.S. Census Bureau, Survey of Income and Program Participation (SIPP), 2023

- Pension Participation Rate (10 Points): The percentage of households receiving retirement income, including pensions, annuities, and retirement account distributions, indicating access to stable income beyond personal savings.

- Source: U.S. Census Bureau, American Community Survey 1-Year Estimates 2024, Table B19059

Earnings — 20 Points

- Median Household Income, Householders 65 and Older: The median annual income for households headed by someone 65 or older, capturing the overall earning power available to retirees in each state.

- Source: U.S. Census Bureau, American Community Survey 1-Year Estimates 2024, Table S1903

Homeownership Rate — 20 Points

- The percentage of residents 65 and older who own their home, reflecting housing stability and reduced exposure to rising rental costs in retirement.

- Source: U.S. Census Bureau, American Community Survey 1-Year Estimates 2024, Table S0103

Quality of Life — 15 Points

- Life expectancy at birth in each state, used as an indicator of overall health conditions and the likely duration of retirement.

- Source: CDC National Center for Health Statistics, U.S. State Life Tables 2022, published December 2025

Cost of Living — 15 Points (Inverted Score)

- A composite cost-of-living index score where a lower value receives a higher score, as affordability directly determines how far retirement income and savings stretch.

- Source: Missouri Economic Research and Information Center (MERIC) / C2ER, Q2 2025

About Western & Southern Financial Group

Founded in Cincinnati in 1888 as The Western and Southern Life Insurance Company, Western & Southern Financial Group, Inc., is No. 310 on the Fortune 500® and the parent company of a group of diversified financial services businesses. It serves 6.3 million customers — individuals, families, businesses, foundations and nonprofits — with a wide range of insurance, investment and retirement solutions through an ever-growing distribution system. Assets owned ($88.0 billion) and managed ($44.5 billion) totaled $132.5 billion as of Dec. 31, 2025.1 Western & Southern is one of the strongest life insurance groups in the world, with seven life insurance subsidiaries that maintain very strong financial strength ratings. For more information, visit westernsouthern.com.

1 The financial information presented here is preliminary and unaudited.

Review our current financial ratings.

From Fortune. ©2025 Fortune Media (USA) Corporation. All rights reserved. Used under license. Fortune and Fortune 500 are registered trademarks of Fortune Media (USA) Corporation and are used under license. Fortune and Fortune Media (USA) Corporation are not affiliated with, and do not endorse products or services of, Western & Southern Financial Group.

Fair Use Statement

This content may be shared for noncommercial purposes with proper attribution to Western & Southern Financial Group and a link to the original source.