An ETF (exchange-traded fund) and a mutual fund both allow you to invest in a basket of securities through a single purchase, but they differ fundamentally in how you buy and sell shares, how they're taxed, and what costs you'll pay. Understanding these differences helps you keep more of your investment returns.

ETFs vs Mutual Funds: What Makes Them Different?

Both ETFs and mutual funds offer diversification and are regulated investment products. Most mutual funds and many ETFs are registered under the Investment Company Act of 1940, though some exchange-traded products are structured differently. They can track the same indexes or follow similar investment strategies. The differences lie in their mechanics.

Both ETFs and mutual funds can follow passive index strategies or active management approaches. While ETFs were historically associated with index tracking, actively managed ETFs have grown significantly and now represent a meaningful share of the marketplace.

Exchange Traded Funds (ETFs)

- ETFs trade on stock exchanges like individual stocks.

- You place an order through a brokerage account, and your trade executes at fluctuating market prices, that change second by second throughout the trading day.

- This intraday trading flexibility lets you react to market movements, set limit orders, or buy at specific prices.

Mutual Funds

- Mutual funds work differently. When you place an order, you don't know precisely what you'll pay.

- All orders submitted during the day receive the same net asset value (NAV) calculated after market close, typically around 4:00 p.m. Eastern.

- If you place an order at 10:00 a.m. or 3:45 p.m., you get the same end-of-day price.

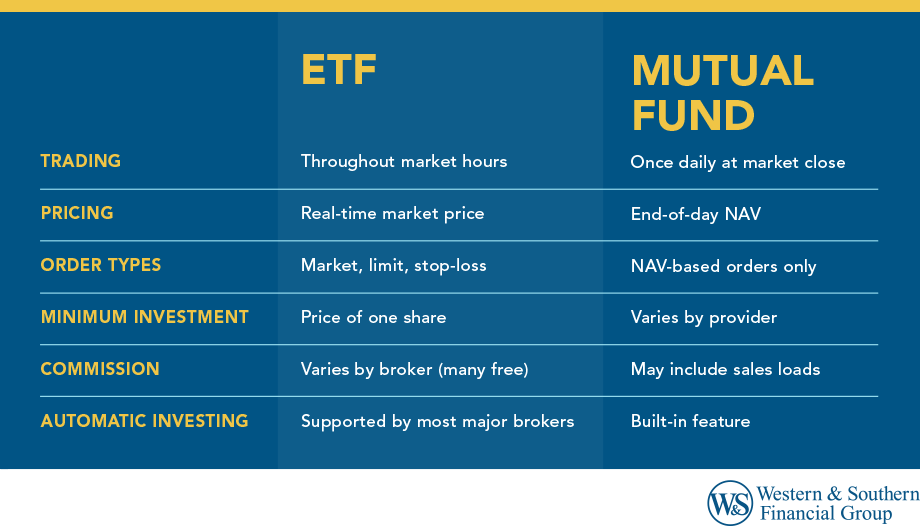

Trading and Pricing Comparison

| Feature | ETF | Mutual Fund |

|---|---|---|

| Trading | Throughout market hours | Once daily at market close |

| Pricing | Real-time market price | End-of-day NAV |

| Order Types | Market, limit, stop-loss | NAV-based orders only |

| Minimum Investment | Price of one share | Varies by provider |

| Brokerage Commissions | Varies by broker (many free) | May include sales loads |

| Automatic Investing | Supported by most major brokers | Built-in feature |

How Does Tax Efficiency Actually Work?

ETFs typically generate fewer taxable capital gains distributions than mutual funds, and that difference comes from their underlying structure.

That said, many index mutual funds are also highly tax-efficient due to low portfolio turnover. Additionally, some actively managed strategies may prioritize tax management as part of their investment approach.

When mutual fund investors sell shares, the fund manager often must sell underlying securities to raise cash for redemptions. If those securities have appreciated, the sale creates capital gains. These gains get distributed to all shareholders, including those who didn't sell. You can owe taxes on capital gain distributions even if you didn’t sell shares and even if the distribution is reinvested rather than paid out in cash.1

ETFs use an in-kind redemption process.2 When large institutional investors (authorized participants) redeem ETF shares, they receive the underlying securities rather than cash. This exchange doesn't trigger a taxable event for the fund.2 ETFs can still distribute dividends and, in some years, capital gains, but capital gains distributions are generally less common than in mutual funds.

The numbers tell the story. In 2025, just 7% of all ETFs distributed capital gains compared with 52% for mutual funds.3 For investors holding funds in taxable brokerage accounts, this difference compounds significantly over time.

The tax efficiency exception: This advantage largely disappears in tax-advantaged accounts. Inside a 401(k), IRA, or HSA, you won't pay taxes on capital gains distributions until withdrawal (or never, for Roth accounts). If most of your investing happens in retirement accounts, the ETF tax advantage matters less.

Another consideration: bid-ask spreads. ETFs have a small gap between buy and sell prices. For popular ETFs tracking major indexes, this spread is usually pennies per share. For thinly traded or niche ETFs, spreads can exceed 0.5%, partially offsetting cost advantages.

What Will You Actually Pay in Fees?

Fund expenses directly reduce your returns. A fund earning 8% with a 1% expense ratio delivers 7% to you. Over 30 years, on a $10,000 investment portfolio, that 1% difference costs you roughly $25,000 in lost growth.

The asset-weighted average expense ratio for all U.S. mutual funds and exchange-traded funds ticked down to 0.34% in 2024 from 0.36% in 2023.4 But averages mask wide variation.

While passive strategies typically carry lower expense ratios, active management seeks to add value through security selection, risk management, and tactical positioning. Some active managers aim to outperform benchmarks or provide downside protection during volatile markets. Costs are only one part of the total return equation.

Expense Ratio Breakdown (2024)

| Fund Type | Asset-Weighted Average |

|---|---|

| All Passive Funds | 0.11% |

| All Active Funds | 0.59% |

| Index Equity ETFs | 0.14% |

| Active Equity Mutual Funds | 0.60% |

| Broad Market Index ETFs | Under 0.05% |

Broad market index ETFs that track the S&P 500, for example, often charge less than 0.05%. Some providers have pushed core index fund expenses to essentially zero.4

Beyond expense ratios, watch for these costs:

Sales loads: Some mutual funds charge sales loads (a sales charge paid when you buy or sell). No-load funds and most ETFs don’t charge sales loads, though you may still pay expense ratios and trading-related costs.5

12b-1 fees: These marketing and distribution fees, typically 0.25-1%, get buried in mutual fund expense ratios. ETFs rarely charge them.5

Trading costs: Many brokers now offer commission-free ETF trades, but some charge $5-$20 per trade. Frequent traders should compare brokerage fee schedules.

Active management may also provide benefits that aren’t reflected solely in expense ratios, such as risk management during market downturns, sector rotation, or income strategies tailored to specific objectives. Investors should weigh both cost and potential value when comparing fund options.

Are ETFs or Mutual Funds a Right Fit?

Neither ETFs nor mutual funds are universally "better." The right choice depends on how you invest, where you invest, and what you're investing for.

ETFs Often Work Better When You

- Invest primarily in taxable brokerage accounts

- Want to control exactly when and at what price you buy

- Make lump-sum investments rather than regular contributions

- Prefer either index-based or actively managed strategies in an exchange-traded format

- Have a smaller initial investment amount

Mutual Funds Often Work Well When You

- Invest through an employer-sponsored retirement plan, where mutual funds are commonly offered

- Want to make consistent, long-term contributions in either retirement or taxable accounts

- Prefer automatic investing features that support regular contributions

- Are interested in actively managed strategies, whether offered as a mutual fund or ETF

- Plan to make frequent small purchases where transaction costs could matter

- Appreciate a structured, hands-off approach to investing

How to Evaluate & Compare Funds

Step 1: Define Your Investment Objectives

Start with what you're trying to accomplish. A broad-market index fund tracking the S&P 500 differs fundamentally from a sector fund or an actively managed fund. Compare funds with similar asset class strategies before comparing structures.

Step 2: Calculate Total Cost of Ownership

Look beyond headline expense ratios. For ETFs, factor in bid-ask spreads and any trading commissions. For mutual funds, check for loads, redemption fees, and 12b-1 fees. Use FINRA's Fund Analyzer for a complete comparison.6

Step 3: Consider Your Account Type

If investing in a taxable account, the ETF's tax efficiency advantage matters significantly. In tax-advantaged accounts, the playing field levels out. Match the fund type to the account.

Step 4: Review the Fund’s Track Record and Structure

Read the prospectus. For index funds, review how closely the fund has tracked its benchmark (tracking error). For actively managed funds, evaluate long-term performance relative to benchmarks and peers, keeping in mind consistency across different market cycles. For ETFs, review average trading volume and historical bid-ask spreads. Low-volume ETFs can be more expensive to trade. Good portfolio management means matching the fund’s strategy, costs, and behavior fit.

Which Fund Is Right For You?

Choosing between an ETF and a mutual fund isn’t about ranking one above the other, it’s about choosing the right tool for your specific financial house.

ETFs may offer advantages in tax efficiency and trading flexibility in taxable accounts, but both structures can be effective depending on strategy, cost, and investor preference. But if you are building your retirement through a 401(k) or want the strict discipline of automated, hands-off investing, a traditional mutual fund remains a stellar choice.

Don't let paralysis by analysis keep you on the sidelines. Whether you prefer the intraday flexibility of an ETF or the once-a-day simplicity of a mutual fund, both vehicles offer a highly effective way to build a diversified portfolio.

Provided for informational purposes only. Not all products and services discussed are available through member of Western & Southern Financial Group.

Sources

- Mutual Funds (Costs, Distributions, etc.) – Internal Revenue Service. https://www.irs.gov/faqs/capital-gains-losses-and-sale-of-home/mutual-funds-costs-distributions-etc.

- Tax efficiency is structural: ETFs continue to issue fewer capital gains than mutual funds - State Street Corporation. https://www.ssga.com/us/en/individual/insights/tax-efficiency-is-structural-etfs-continue-to-issue-fewer-capital-gains-than-mutual-funds.

- 2025 Investment Company Fact Book – Investment Company Institute. https://www.icifactbook.org/.

- How Fund Fees are Evolving in the US – Morningstar. https://www.morningstar.com/business/insights/blog/funds/us-fund-fee-study/.

- Mutual Fund and ETF Fees and Expenses – Investor Bulletin – U.S. Securities and Exchange Commission. https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-bulletins/mutual-fund-and-etf-fees-and-expenses-investor-bulletin.

- Fund Analyzer by FINRA – Financial Industry Regulatory Authority. https://tools.finra.org/fund_analyzer/.