Americans are living longer than previous generations, stretching retirement well beyond the timelines many financial plans were originally built to support. A longer life brings real opportunities, but it also raises a question that too few people ask early enough: Will the money last?

To explore how Americans are thinking about and preparing for longer lifespans, Western & Southern Financial Group surveyed 975 adults aged 30 and older about their retirement expectations and financial planning habits. While the sample is not nationally representative, the findings point to some notable patterns worth considering, particularly around the gap between how long respondents expect to live and how long they expect their savings to hold out.

How Big Is the Longevity Gap?

Among surveyed respondents, the average expected lifespan is 85, yet savings are projected to run out at 79. That 6-year gap between expected lifespan and savings runway is what this survey calls the longevity gap, and for many respondents, it is considerably wider.

More than one-quarter of respondents (27%) face a projected gap of 10 or more years, meaning their savings could run out a full decade before they expect to pass away. Even so, retirement planning horizons don't always reflect those long-term expectations.

More than one-quarter of respondents (27%) face a projected gap of 10 or more years, meaning their savings could run out a full decade before they expect to pass away. Even so, retirement planning horizons don't always reflect those long-term expectations.

More than a third of respondents expect to live to 90 or older, yet most aren't preparing financially for 30 or more years of retirement. Baby boomers show a particularly notable contrast: 41% expect to live to 90 or beyond, but only 15% are planning for a retirement lasting more than 30 years, the lowest rate of any generation in the sample.

Some of the longevity gap may be tied to limited planning activity. One-quarter of respondents have never calculated how many years of retirement they need to fund, and among those who have attempted the math, 33% have never estimated how long their savings might last.

Contribution patterns in the sample are also worth noting. One in 5 respondents reported currently putting nothing toward retirement savings. That share was highest among baby boomers, with 34% reporting no current contributions. Among respondents by marital status, 30% of divorced respondents and 18% of married respondents reported making zero contributions.

Outliving their savings is a concern shared widely across the sample. Nearly two-thirds of respondents (63%) said they worry about it, including 68% of women and 58% of men.

Concern was also higher among younger people: 70% of millennials and 69% of Gen X respondents reported anxiety about outliving retirement savings, compared with 54% of baby boomers. A higher share of non-homeowners (73%) expressed concern than homeowners (59%), and more unemployed workers (77%) were worried than full-time workers (67%) or retirees (46%).

When asked what they would do if their savings fell short, respondents anticipated a range of adjustments, including:

- Downsizing or selling a home (43%)

- Relying on government assistance (39%)

- Starting a side hustle (33%)

- Returning to work (26%)

- Relying on family support (19%)

One-quarter of respondents said they simply don't know what they would do if their retirement savings ran out.

Healthcare, Caregiving, and the Costs Most Plans Don't Account For

Longer lifespans tend to bring rising healthcare and caregiving costs, and the survey findings suggest many respondents haven't fully factored those expenses into their retirement plans. A significant part of that may come down to gaps in awareness about how retirement healthcare coverage actually works.

One of the more striking findings involves Medicare. Nearly half of respondents (47%) either believe or aren't sure that Medicare covers long-term care costs, such as nursing home care or in-home aides, including 20% who believe it does and 27% who are unsure.

Medicare does not cover long-term care services. This misunderstanding was more common among younger respondents, with 55% of Gen X and 51% of millennials answering incorrectly or expressing uncertainty, compared to 34% of baby boomers.

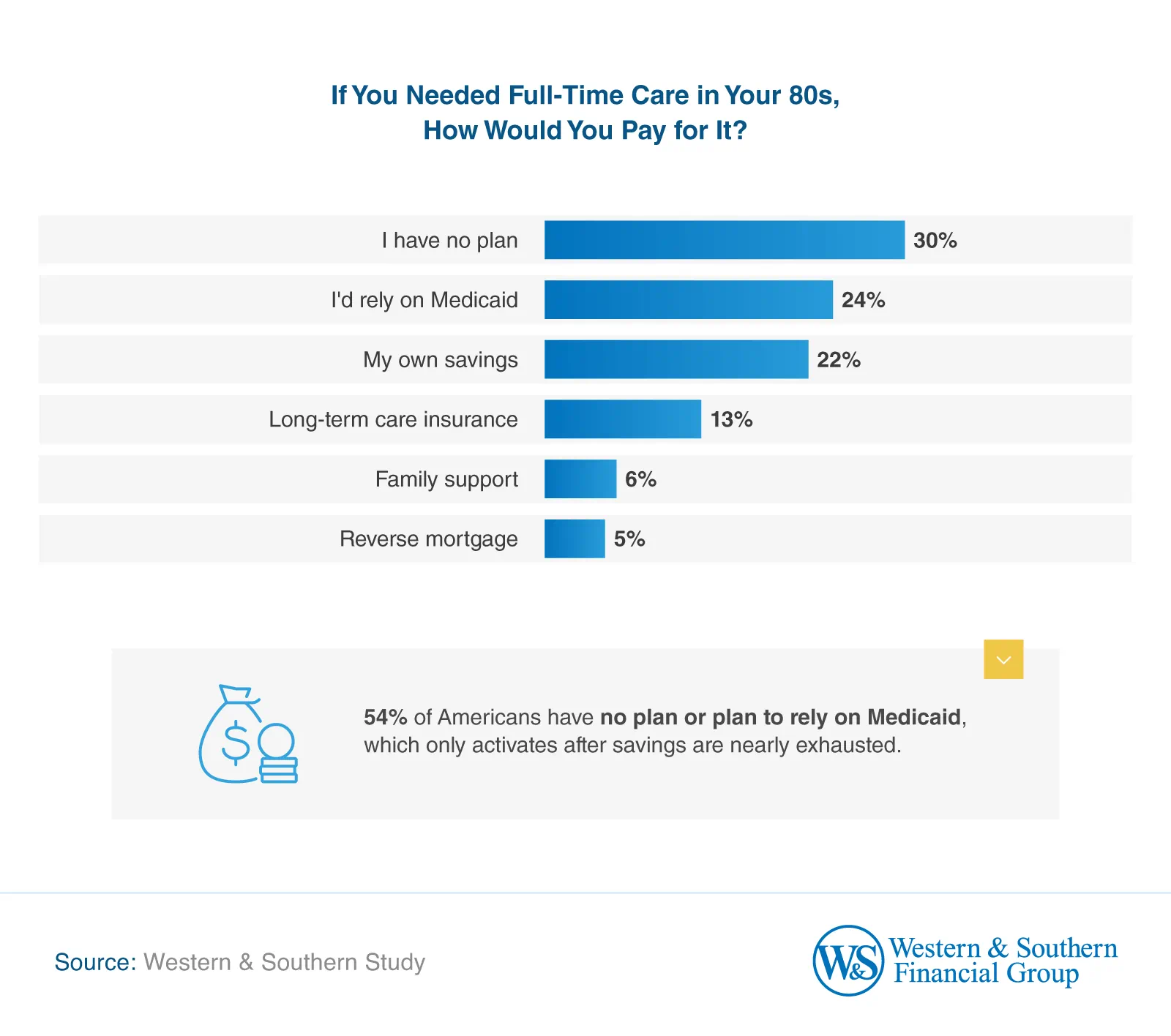

When asked how they would pay for full-time care in their 80s, 3 in 10 respondents said they have no plan, while 24% expect to rely on Medicaid. It's worth noting that Medicaid may cover long-term care, but eligibility depends on meeting specific income and asset requirements. Gen X respondents reported the highest uncertainty in this area, with 36% saying they have no long-term care plan.

Caregiving responsibilities add another layer of financial complexity for many households. Currently, 14% of respondents are serving as caregivers, and another 16% expect to take on that role in the future, potentially during their peak earning years. Millennials reported the highest caregiving expectations in the sample, with 16% already providing support and 28% expecting to do so later.

Despite all of this, very few respondents have modeled these costs into their planning. Only 18% said they have accounted for inflation or rising healthcare costs in their retirement plans, including 23% of men and 14% of women. Another 38% said they have thought about it but haven't calculated the impact, and 30% have taken no action at all.

Taking Stock of Retirement Readiness

Many respondents in the sample appear to be approaching retirement without key financial tools in place. Nearly half (48%) reported having none of the core retirement planning safeguards, while 52% have at least one. Among respondents by marital status, divorced individuals appear particularly underprotected, with 65% reporting none of the key planning tools in place, compared to 35% of married respondents.

Among those who do have safeguards, guaranteed lifetime income such as an annuity or pension is the most commonly reported, with 29% of respondents saying they have one. Other tools appear less frequently across the sample and include:

- Working with a financial advisor (22%)

- Maintaining an HSA (19%)

- Having a written retirement income plan (10%)

- Conducting a 30-year withdrawal stress test (4%)

For those who do work with a financial advisor, engagement tends to be relatively consistent. Among respondents with an advisor, 77% check in at least annually, while 23% communicate only sporadically or almost never.

Among respondents who have not yet claimed Social Security benefits, only 12% said they plan to do so at age 70, the age that maximizes monthly benefits. Meanwhile, 21% plan to claim at 62, which permanently reduces payments. That share rises to 31% among baby boomers, making them the most likely generation in the sample to plan for early claiming.

Confidence in long-term income sources was limited across the sample as well:

- 43% of respondents said they are not confident that their Social Security or pension benefits will last 30 years.

- 36% are somewhat confident.

- 12% are very confident.

- 9% do not expect to receive Social Security at all.

Skepticism was notably higher among younger respondents. Half of Gen X and 47% of millennials expressed low confidence, and 16% of millennials said they don't expect to receive any Social Security income.

The generational picture comes into sharper focus when looking at projected savings gaps. Millennials in the sample face the largest estimated longevity gap at 7 years, with median savings of $70,000 projected to run out at age 75 against an expected lifespan of 82. Gen X faces a 6-year gap, and baby boomers a 4-year gap.

The survey also asked respondents how they would react if they discovered a retirement shortfall. Thirty-seven percent said they would take no action, while 63% said they would take at least one corrective step. Among those who would act, the most commonly cited strategies were:

- Increasing savings (30%)

- Seeking professional financial advice (21%)

- Delaying Social Security benefits (19%)

Inaction was more commonly reported among older respondents. Nearly half of baby boomers (48%) said they would do nothing, compared to 31% of millennials and 31% of Gen X respondents.

Turning Awareness Into Action

The findings from this survey indicate that people are aware that retirement is approaching, but their planning hasn't always kept pace with reality. Living into your 80s or 90s is increasingly common, which means your financial goals need to account for healthcare costs, potential caregiving responsibilities, and the real possibility that your savings could run out before you do.

The good news is that there are tools available to help close that gap, including employer-sponsored retirement plans, IRAs, diversified investments, and working with a financial advisor to evaluate long-term financial needs. The most important step is simply starting that conversation sooner rather than later.

Methodology

Western & Southern Financial Group commissioned an online survey of 975 U.S. adults ages 30 and older through CloudResearch Connect to examine retirement planning behaviors, longevity expectations, and financial preparedness for longer lifespans. The sample included younger adults, alongside Americans approaching or already in retirement. Respondents were 59% female and 41% male. Percentages may not total 100% due to rounding or multi-select questions.

About Western & Southern Financial Group

Founded in Cincinnati in 1888 as The Western and Southern Life Insurance Company, Western & Southern Financial Group, Inc., is No. 310 on the Fortune 500® and the parent company of a group of diversified financial services businesses. It serves 6.3 million customers — individuals, families, businesses, foundations and nonprofits — with a wide range of insurance, investment and retirement solutions through an ever-growing distribution system. Assets owned ($88.0 billion) and managed ($44.5 billion) totaled $132.5 billion as of Dec. 31, 2025.1 Western & Southern is one of the strongest life insurance groups in the world, with seven life insurance subsidiaries that maintain very strong financial strength ratings. For more information, visit westernsouthern.com.

1 The financial information presented here is preliminary and unaudited.

Review our current financial ratings.

From Fortune. ©2025 Fortune Media (USA) Corporation. All rights reserved. Used under license. Fortune and Fortune 500 are registered trademarks of Fortune Media (USA) Corporation and are used under license. Fortune and Fortune Media (USA) Corporation are not affiliated with, and do not endorse products or services of, Western & Southern Financial Group.

Fair Use Statement

This content may be shared for non-commercial purposes with appropriate credit to Western & Southern Financial Group and a direct link to the original study.

Western & Southern Financial Group and its member companies do not provide legal services, divorce mediation, divorce analysis, or estate planning services, and we do not act as a divorce attorney, mediator, or legal advisor. Individuals should seek the advice of an appropriate professional regarding their specific circumstances.