Money is one of the most important parts of a marriage, yet it's often one of the least fully discussed. From debt and daily spending to retirement dreams and family obligations, financial expectations can shape a couple's future in many ways. Yet, alignment isn't guaranteed simply because two people share a life together.

To better understand how married couples navigate money, Western & Southern Financial Group surveyed 1,008 married Americans about their financial conversations, disagreements, and long-term plans. The findings reveal a mix of confidence and uncertainty. While many couples believe they are on the same page, deeper questions about retirement, financial dependence, and supporting loved ones suggest that important gaps remain.

The Conversations Couples Skip Before "I Do"

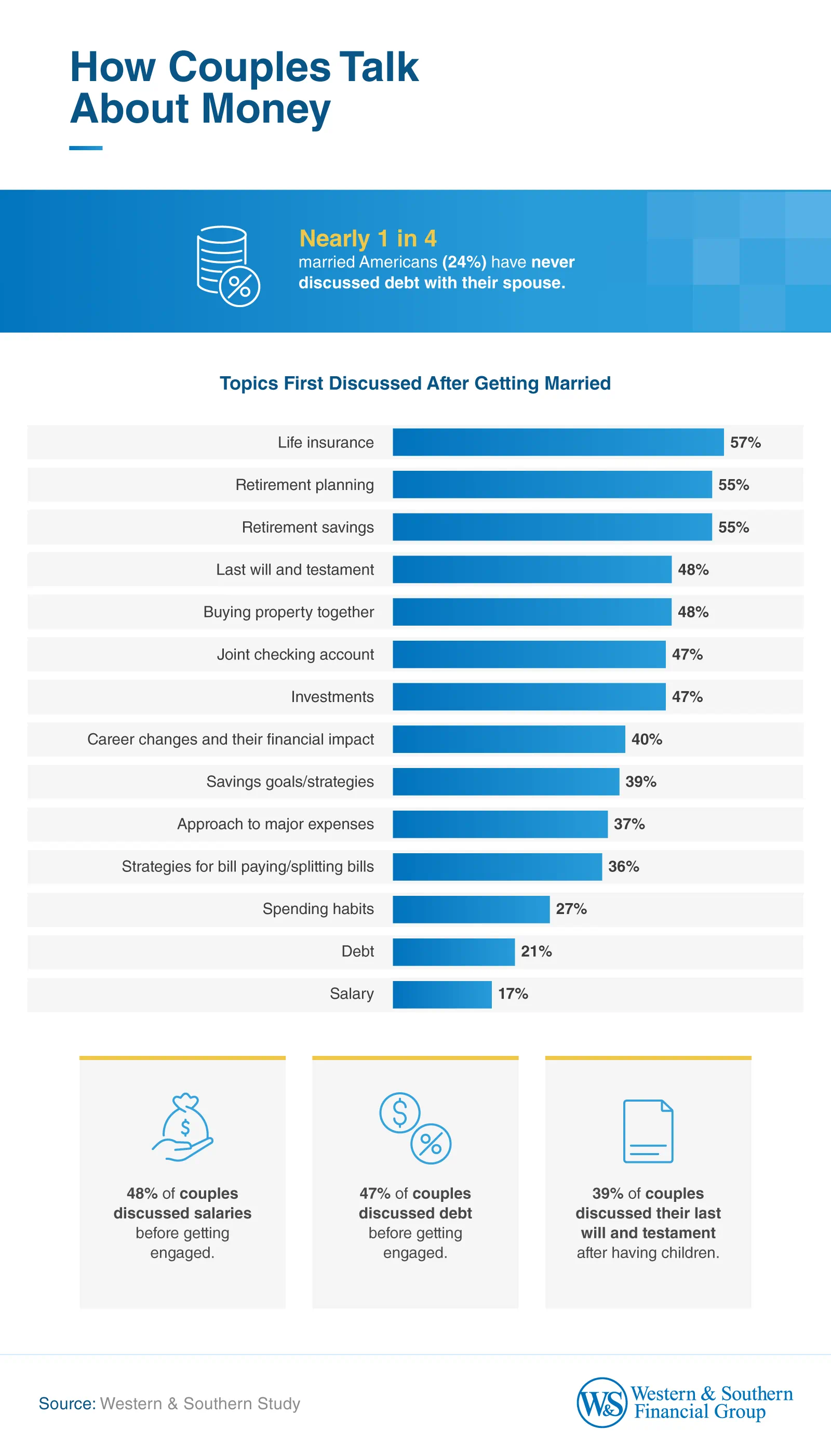

Money conversations often start later than many expect. Nearly a quarter of married Americans said they have never discussed debt with their spouse, and 40% said they avoided discussing long-term financial goals early in their relationship.

Financial expectations often form long before marriage. On average, Americans sought a partner earning a minimum salary of $33,086. Irresponsible spending (41%) was the biggest financial dealbreaker during dating, followed by:

- Credit card debt (21%)

- Lack of financial literacy (20%)

- Too low a salary (12%)

- Still living with parents (12%)

- No savings account (10%)

- Parent(s) paying one or more bills (7%)

- Personal loans (7%)

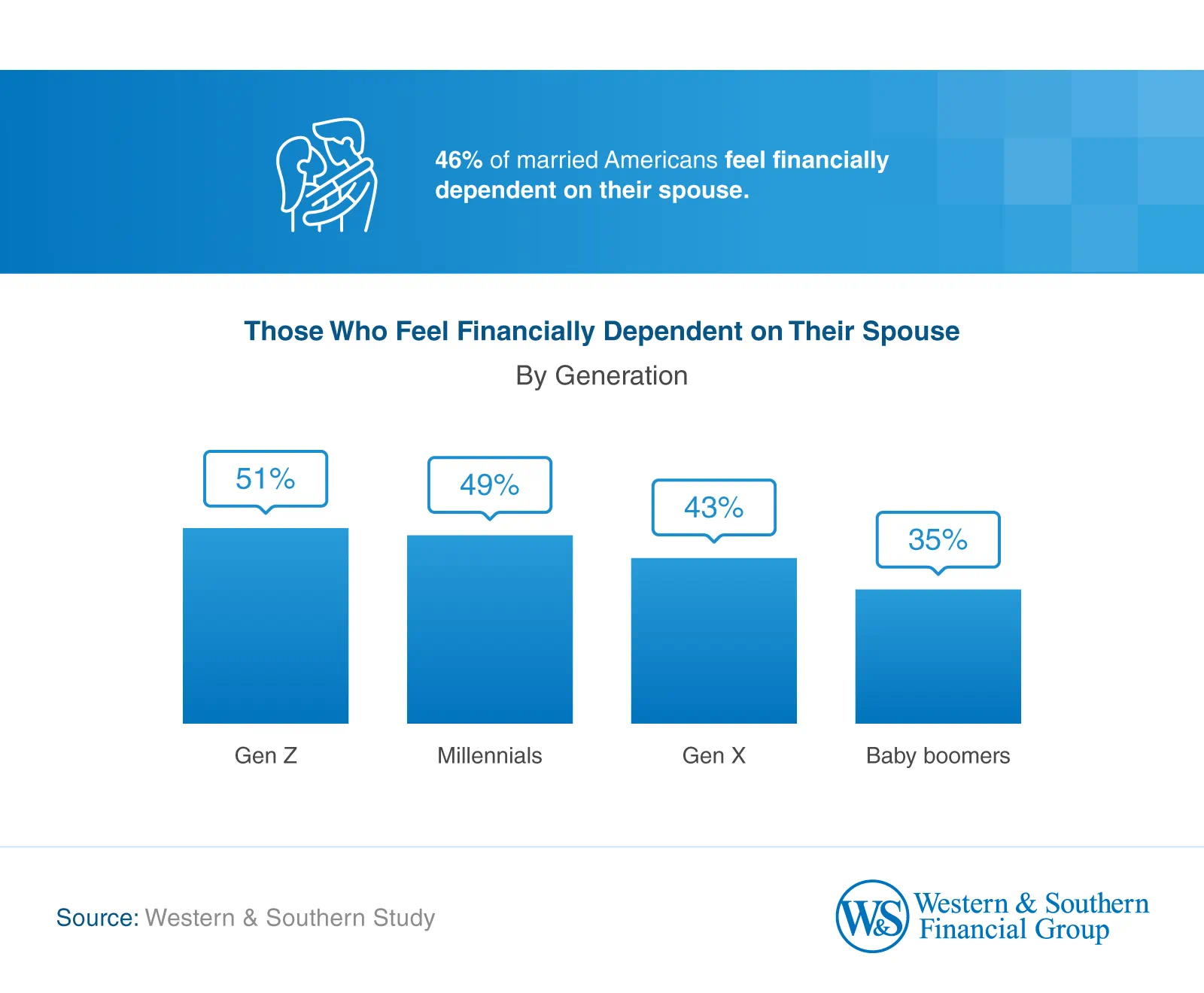

Despite these expectations, only 12% of couples consulted a financial advisor together before marriage, though that figure rises to 17% after getting married. Nearly half of all married Americans (46%) feel financially dependent on their spouse, meaning they could not maintain their current lifestyle without their partner's support. Among this group, 58% of married women and 30% of married men reported feeling this way.

Couples also identified the topics they wish they had addressed before getting married. The most common ones included:

- Spending habits (17%)

- Saving goals or strategies (13%)

- Debt (12%)

- Approach to major expenses and financial obligations (10%)

- Strategies for bill paying or splitting bills (9%)

- Retirement savings (8%)

- Investments (7%)

- Retirement planning (7%)

Financial secrecy also remains a pressure point: 25% of married Americans admitted to hiding a significant purchase or debt from their spouse, and 30% said they would end a relationship due to financial dishonesty. Gen Z is the most likely to draw that line (45%), compared to millennials (31%), Gen X (29%), and baby boomers (20%).

Planning Together or Apart?

Financial disagreements are common, with spending habits (53%) and impulse buying (45%) topping the list of arguments among married couples. Married women (35%) were more likely than married men (30%) to argue about their spouse's failure to save. Just 10% overall said they never fight about money.

Change after marriage may contribute to tension. More than half of married couples (58%) said their partner's financial habits shifted after they got married, and only 27% entered marriage with a formal financial plan

Change after marriage may contribute to tension. More than half of married couples (58%) said their partner's financial habits shifted after they got married, and only 27% entered marriage with a formal financial plan

Even so, most couples report satisfaction. Eighty-eight percent of married couples said they're currently satisfied with their marriage, including 63% who are very satisfied and 25% who are somewhat satisfied. Those who entered marriage with a formal financial plan were more likely than those without one to report satisfaction (95% vs. 86%).[5] [6] It's worth noting, however, that this is a correlational finding and does not indicate that financial planning directly improves marital satisfaction.

Alignment becomes more complicated when the extended family is involved. More than half of married couples (54%) reported not being in full agreement about financially supporting aging parents or adult children, highlighting another area where long-term expectations may differ.

Alignment becomes more complicated when the extended family is involved. More than half of married couples (54%) reported not being in full agreement about financially supporting aging parents or adult children, highlighting another area where long-term expectations may differ.

Retirement Dreams, Different Timelines

Retirement conversations are common, but agreement is less certain. While 75% of married Americans said they have discussed retirement expectations, fewer than half (43%) completely agree on what retirement will look like.

Only 28% of married Americans said they're very confident their finances could handle an early spousal retirement. Baby boomers are the exception, with 52% feeling "very confident," compared to Gen X (26%) and millennials (25%). A higher share of women (43%) than men (24%) felt financially unprepared for early retirement.

Men were more likely than women to say they want to keep working after retirement age (46% vs. 20%). Twenty-five percent of women and 16% of men said both partners want to continue working. Couples also shared their potential post-retirement housing plans.

Closing the Financial Alignment Gap

Marriage brings shared responsibilities, but financial alignment doesn't happen automatically. This study shows that many couples still avoid key conversations about debt, retirement, and family support, even years after getting married.

Whether the topic is daily spending habits or retirement expectations, these gaps in planning can leave couples navigating major financial decisions without a shared foundation. For couples today, the path to financial alignment may begin with the conversations they've been putting off.

Methodology

Western & Southern Financial Group surveyed 1,008 married Americans about money conversations and financial strategy in their relationships. The respondent pool included 56% women and 43% men. Generationally, participants identified as 10% baby boomers, 29% Gen X, 56% millennials, and 5% Gen Z.

The data was collected in February 2026. Because the survey relied on voluntary participation, the results may reflect self-selection bias, meaning those who chose to respond may differ from the broader population of married Americans.

About Western & Southern Financial Group

Founded in Cincinnati in 1888 as The Western and Southern Life Insurance Company, Western & Southern Financial Group, Inc., is No. 310 on the Fortune 500® and the parent company of a group of diversified financial services businesses. It serves 6.3 million customers — individuals, families, businesses, foundations and nonprofits — with a wide range of insurance, investment and retirement solutions through an ever-growing distribution system. Assets owned ($88.0 billion) and managed ($44.5 billion) totaled $132.5 billion as of Dec. 31, 2025.1 Western & Southern is one of the strongest life insurance groups in the world, with seven life insurance subsidiaries that maintain very strong financial strength ratings. For more information, visit westernsouthern.com.

1 The financial information presented here is preliminary and unaudited.

Review our current financial ratings.

From Fortune. ©2025 Fortune Media (USA) Corporation. All rights reserved. Used under license. Fortune and Fortune 500 are registered trademarks of Fortune Media (USA) Corporation and are used under license. Fortune and Fortune Media (USA) Corporation are not affiliated with, and do not endorse products or services of, Western & Southern Financial Group.

Fair Use Statement

This content may be shared for non-commercial purposes with appropriate credit to Western & Southern Financial Group and a direct link to the original study.