This guide gives educators the support they need to close that gap. From free, ready-made lesson plans to eye-opening data about Gen Z's financial knowledge, it offers a practical toolkit for teaching high school students how to budget, save, borrow, and plan for the future with confidence.

Which States Are Teaching Teens How To Manage Money?

As financial literacy becomes more necessary for navigating everything from student loans to credit cards, schools across the country are reevaluating how they teach money management. Most states include personal finance in their academic standards, but a surprising number still fall short when it comes to requiring instruction.

While 48 states include personal finance in their standards as of 2024, only 20 require high school students to take a standalone personal finance course in order to graduate. That means millions of teens could be leaving school without learning essential financial concepts like budgeting, savings, compound interest, and income tax — concepts that shape their financial decisions for years to come.

States with required personal finance courses include:

- Alabama

- Connecticut

- Florida

- Indiana

- Kansas

- Louisiana

- Minnesota

- Mississippi

- Nebraska

- New Hampshire

- North Carolina

- Ohio

- Pennsylvania

- Rhode Island

- South Carolina

- Tennessee

- Utah

- Virginia

- West Virginia

- Wisconsin

Even fewer states measure students' financial knowledge. Only Utah and Colorado require standardized testing on personal finance, signaling a lack of accountability in ensuring students develop the skills they need to manage their financial future.

In Alaska, California, and Washington, D.C., personal finance is not even included in state standards, leaving students not formally exposed to financial topics like credit scores, bank accounts, or emergency fund planning.

In today's world, where interest rates fluctuate, financial services are more digital, and young adults face increasing debt burdens, providing access to quality financial education is becoming a necessity.

Free Lessons, Real-Life Skills: Financial Education Made Easy

Teaching personal finance doesn't have to mean building a curriculum from the ground up. This toolkit highlights free, ready-made education resources that are aligned with national standards and ideal for helping high school students build real-world financial skills with minimal prep time.

Budgeting and Real-Life Math Exercises

One of the most practical ways to introduce students to financial literacy is through activities that mirror everyday money choices. The FDIC's Money Smart for Young Adults provides downloadable worksheets and lesson plans covering budgeting basics, spending habits, and financial goal setting.

Educators can access weekly and monthly budget templates, cost-of-living comparisons, and "living on a paycheck" simulations that help students connect math to real-life money management. These lessons also introduce the importance of building a savings account early.

Lessons on Saving, Credit, and Investing

To build foundational financial knowledge, the Consumer Financial Protection Bureau and the Federal Reserve offer age-appropriate content that covers topics like saving, credit scores, borrowing from lenders, and investing. These resources include interactive lesson plans and student-facing materials that explore topics like investing, compound interest, and credit card debt through case studies and hands-on exercises.

Goal-Setting and Decision-Making Activities

Teaching teens how to set financial goals and evaluate spending decisions is a core element of financial literacy. The Jump$tart National Standards for Personal Financial Education emphasize decision-making skills and goal setting, which are supported by free resources that guide students through setting SMART goals, identifying opportunity costs, and understanding how personal values influence financial choices. These activities promote responsible money management, long-term planning, and overall financial wellness.

Standards-Aligned for Seamless Classroom Integration

Every resource included in this toolkit aligns with current national benchmarks for personal finance education, making integration into high school classrooms straightforward. These materials can complement existing education programs across subjects like math, economics, and social studies. The Jump$tart Coalition and the Council for Economic Education provide the frameworks many of these tools follow, ensuring educators can confidently meet curriculum requirements while delivering impactful, real-life lessons.

Together, these resources give educators the support they need to build students' financial capability without extra burden. With the right tools, it's easier than ever to help teens make smarter decisions about their financial future.

What Gen Z's Struggles Say About the Need for Financial Education

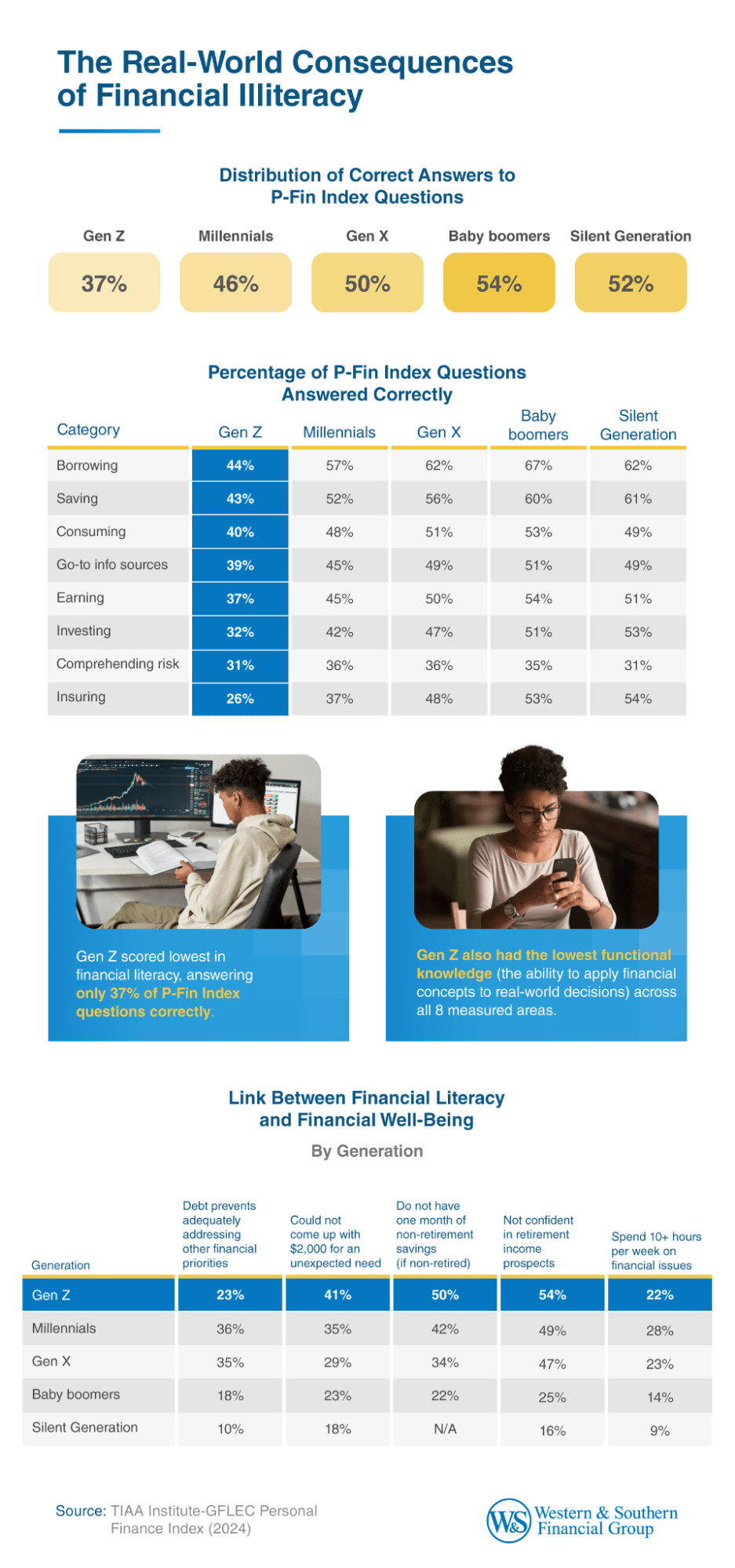

The growing gap in financial literacy across generations is a warning sign. Researchers at the TIAA Institute and the Global Financial Literacy Excellence Center (GFLEC) developed the Personal Finance Index (P-Fin Index), a national survey that assesses how well U.S. adults understand and apply financial knowledge in real life.

The index measures financial literacy across eight core areas: earning, consuming, saving, investing, borrowing, insuring, comprehending risk, and identifying go-to information sources. Participants answered 28 questions based on real-world financial decisions. Their scores reflect the percentage of correct responses, offering one of the most comprehensive snapshots of functional financial literacy in the United States.

According to the 2024 P-Fin Index, Gen Z scores lowest across the board. On average, Gen Z adults (ages 18 to 26) answered only 37% of the questions correctly, the lowest performance among all five generations.

Millennials performed better than Gen Z at 46%, while Gen X, baby boomers, and the Silent Generation each averaged 50% or higher. Even the top-scoring group, baby boomers, answered only 54% of questions correctly, highlighting gaps in financial capability across age groups.

The outlook, though, is especially concerning for Gen Z. They scored the lowest in all eight categories of financial knowledge and were also the least sure about their financial future. More than half (54%) reported not feeling confident about their retirement income prospects. Nearly 2 in 5 Gen Z adults fall into the "very low financial literacy" category. That share decreases with age, dropping to just 13% among the Silent Generation.

Frequently Asked Questions About Financial Literacy

For teens preparing for higher education, jobs, and adult responsibilities, understanding financial concepts early can shape lifelong financial well-being. Below are answers to common questions educators and students may have about financial literacy.

What Does Financial Literacy Mean?

Financial literacy refers to the ability to understand and use financial knowledge to manage personal finances effectively. This includes skills like budgeting, saving, borrowing, investing, and understanding credit, as well as making decisions that support long-term financial security and wellness.

What Are the 7 Key Components of Financial Literacy?

The 7 key components of financial literacy are:

- Earning (understanding income and taxes)

- Spending (creating and managing a budget)

- Saving (building an emergency fund or savings account)

- Investing (learning about risk, return, and diversification)

- Borrowing (responsibly using credit and managing debt repayment)

- Protecting (using insurance and fraud prevention)

- Decision-making (applying knowledge to real-life financial choices)

Other core components are retirement planning and understanding financial products and consumer protections.

What Is the 50/30/20 Rule for Financial Literacy?

The 50/30/20 rule is a simple budgeting strategy that divides income into three categories:

- 50% for needs (housing, groceries, utilities)

- 30% for wants (non-essentials like entertainment or dining out)

- 20% for savings and debt repayment

This method can help individuals build good money management habits and encourage consistent saving.

When Is Financial Literacy Month?

Financial Literacy Month takes place every April and is recognized across the United States as a time to promote financial education. It encourages schools, nonprofits, financial institutions, and government organizations to highlight the importance of personal finance through education programs, public campaigns, and classroom activities. It is also a valuable opportunity for students to explore additional resources and strengthen their financial knowledge.

Bridging the Financial Literacy Divide in High Schools

Teens need financial education now more than ever, and high school is the ideal place to start. With free, standards-aligned tools and a growing national focus on financial literacy, educators have the opportunity to make a lasting impact on students' financial well-being.

Whether it is building a budget, understanding compound interest, or preparing for long-term goals like college or retirement savings, early exposure to real-world financial concepts can set students on a path to financial security. By using these resources in the classroom, educators can help students build the confidence and capability they need to make smart financial decisions for life.

Methodology

This campaign was developed to support the integration of personal finance education in high school classrooms by equipping educators with free, standards-aligned resources and highlighting the current gaps in financial literacy instruction across the U.S.

The goal of the campaign is to:

- Provide educators with a centralized toolkit of personal finance lesson plans, activities, and worksheets

- Promote the adoption of financial education at the high school level

- Use publicly available data to underscore the importance of early financial literacy instruction

The campaign draws exclusively from authoritative, publicly accessible sources, including nonprofit and government-backed education initiatives:

- Council for Economic Education's Survey of the States (2024): To analyze which states require or offer personal finance courses in high schools

- TIAA Institute & GFLEC – 2024 Personal Finance Index (P-Fin Index): To examine the link between financial literacy and real-world financial behavior

- FDIC's Money Smart for Young Adults: A free, standards-aligned curriculum for personal finance instruction

- Federal Reserve Education & CFPB Youth Financial Education Tools: To source lesson plans and educational materials that support core financial literacy topics

- Jump$tart Coalition & Council for Economic Education National Standards: To ensure all toolkit materials align with recognized personal finance education benchmarks

About Western & Southern Financial Group

Founded in Cincinnati in 1888 as The Western and Southern Life Insurance Company, Western & Southern Financial Group, Inc., a Fortune 500® company at No. 284, is the parent company of a group of diversified financial services businesses. Its assets owned ($82.6 billion) and managed ($40.2 billion) totaled $122.8 billion as of March 31, 2025.1 Western & Southern is one of the strongest life insurance groups in the world. Its seven life insurance subsidiaries (The Western and Southern Life Insurance Company, Western-Southern Life Assurance Company, Columbus Life Insurance Company, Gerber Life Insurance Company,2 Integrity Life Insurance Company, The Lafayette Life Insurance Company, and National Integrity Life Insurance Company) maintain very strong financial ratings. Other member companies include Eagle Realty Group, LLC; Fabric by Gerber Life; Fort Washington Investment Advisors, Inc.;3 Gerber Life Agency;4 IFS Financial Services, Inc.; Touchstone Advisors, Inc.;3 Touchstone Securities, Inc.;5 W&S Brokerage Services, Inc.;3,5 and W&S Financial Group Distributors, Inc.6 Western & Southern is a title sponsor of several major Cincinnati events every year. From 2002 to 2023, it served as the title sponsor of the nation’s longest-running professional tennis tournament played in its city of origin, the Western & Southern Open. The renamed Cincinnati Open is one of nine ATP Masters 1000 tournaments, the world’s premier tournaments after the Grand Slams, and a WTA 1000 tournament. The company proudly continues to serve as a major sponsor.

1 The financial information presented here is preliminary and unaudited.

2 Gerber Life is a registered trademark. Used under license from Société des Produits Nestlé S.A. and Gerber Products Company. 3 A registered investment advisor.

4 In the State of California, Gerber Life Agency, LLC is known as and does business as Gerber Life Insurance Agency, LLC.

5 A registered broker-dealer and member FINRA/SIPC.

6 W&S Financial Group Distributors, Inc. (doing business as W&S Financial Insurance Services in CA).

Review our current financial ratings.

From Fortune ©2024 Fortune Media IP Limited. All rights reserved. Used under license. Fortune and Fortune 500 are registered trademarks of Fortune Media IP Limited and are used under license. Fortune and Fortune Media IP Limited are not affiliated with, and do not endorse the products or services of Western & Southern Financial Group.

Fair Use Statement

These findings may be shared for non-commercial purposes as long as proper credit is given via a link.