Divorce after 50 — referred to as "gray divorce" — often coincides with a stage of life when financial paths are narrowing rather than expanding. As retirement draws closer, separating households, dividing assets, and rebuilding stability can carry lasting consequences that are difficult to reverse.

A survey of 235 Americans who have gone through divorce after the age of 50 was conducted by Western & Southern to examine how gray divorce affects retirement timelines, savings, housing, healthcare, and long-term financial security. The data reveals where financial strain shows up most after divorce and which choices can help shorten the road back to stability.

These findings reflect the experiences shared by the respondents surveyed and highlight common financial challenges reported after divorce later in life. Individual outcomes can vary widely, and the results are intended to offer directional insight rather than represent national trends.

Common Financial Costs of Divorce After 50

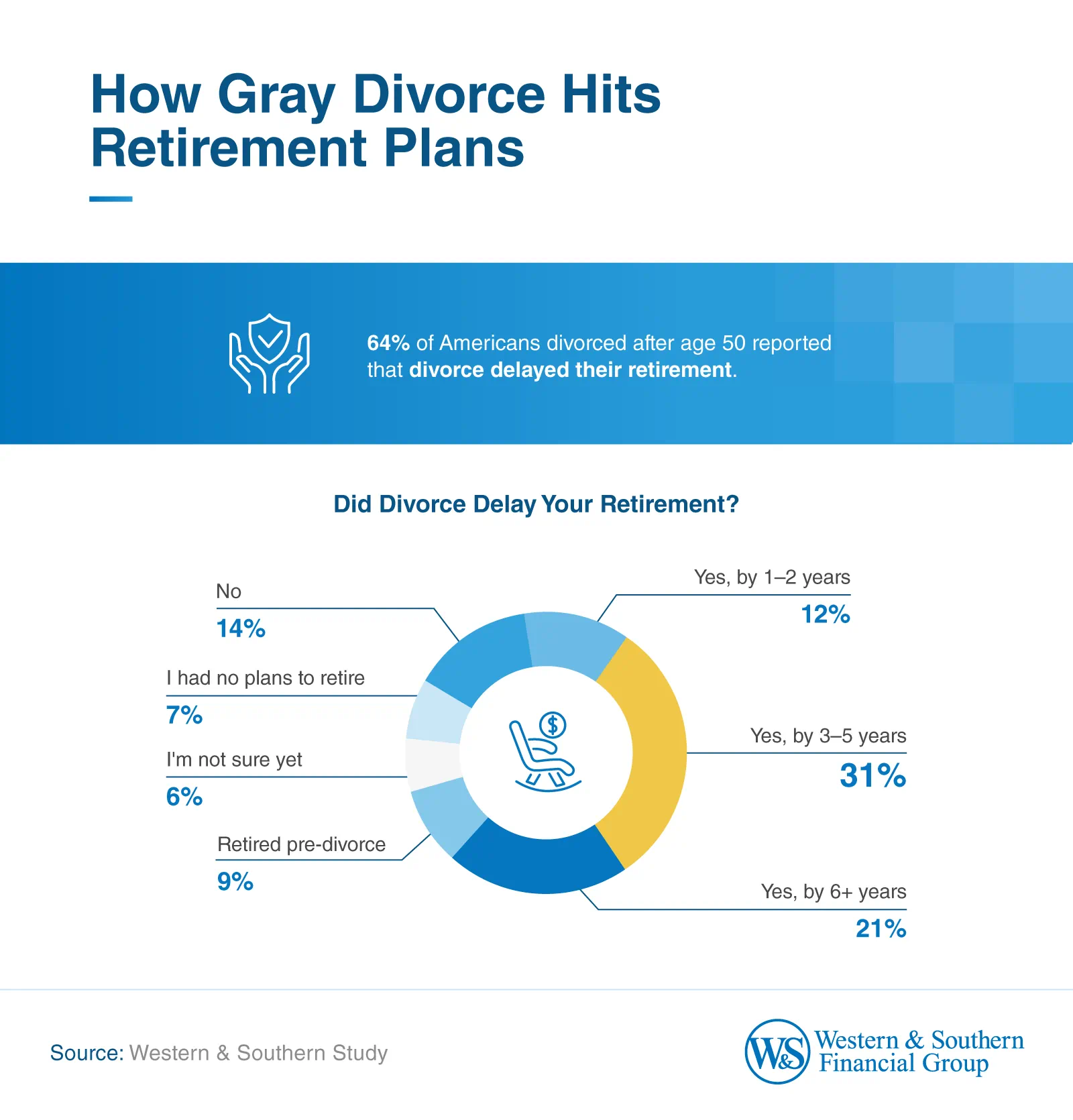

Gray divorce can disrupt retirement timelines, leading many respondents to rethink when — or if — they can stop working. Within this sample of divorced Americans over 50, 64% said divorce delayed their retirement. Just over half (52%) reported delays of 3 years or more, including 59% of men and 38% of women.

While male respondents more often reported longer retirement delays, female respondents more frequently said the split left them uncertain or without a clear retirement plan (26% of women vs. 7% of men).

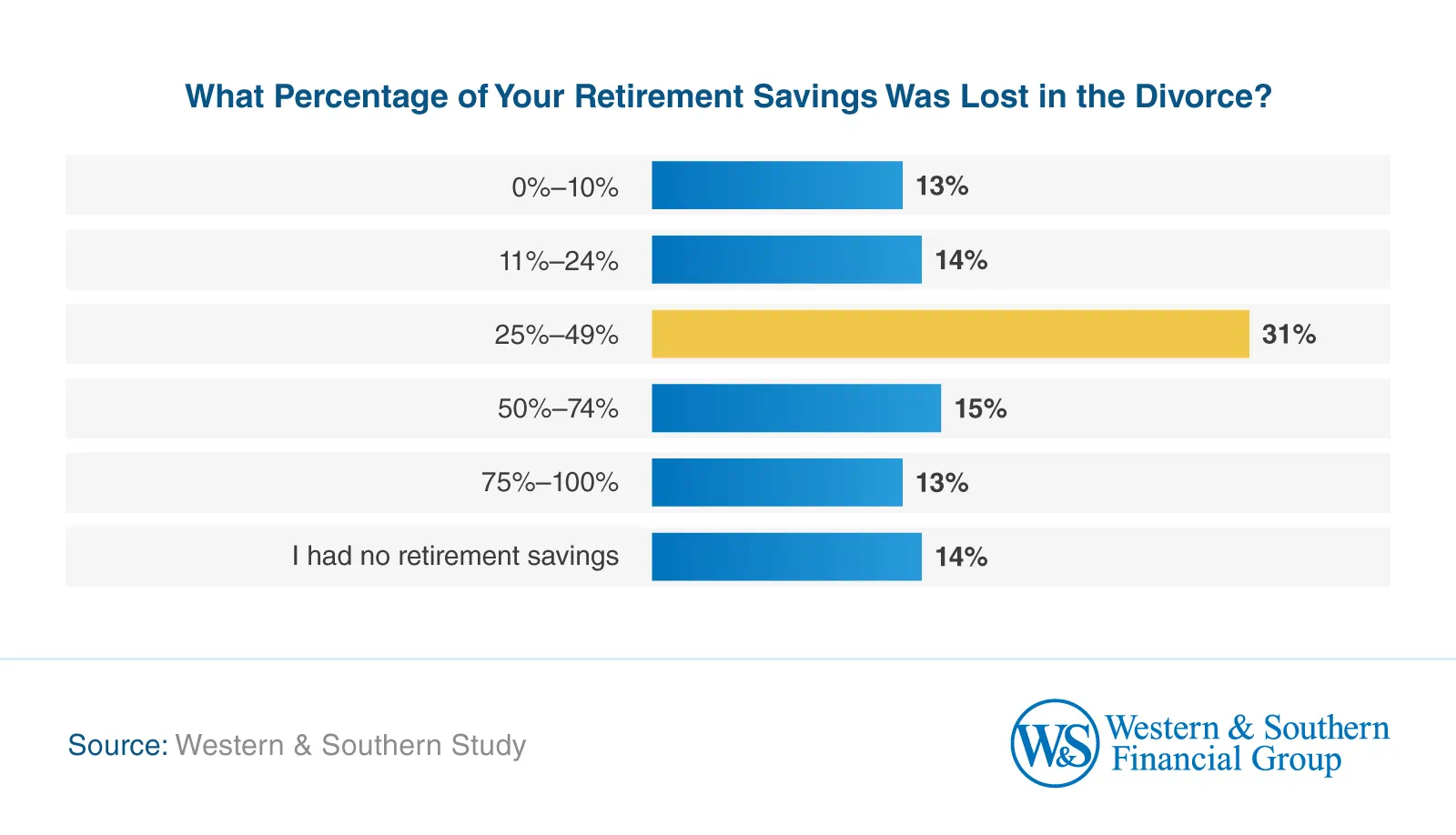

Retirement savings take a sharp hit during gray divorce. About one-third of divorced respondents (31%) lost 25%-49% of their retirement savings, while more than one-quarter (28%) lost 50%-100% due to division, fees, or early withdrawals. More than 1 in 10 (14%) said they had no retirement savings at the time of the divorce.

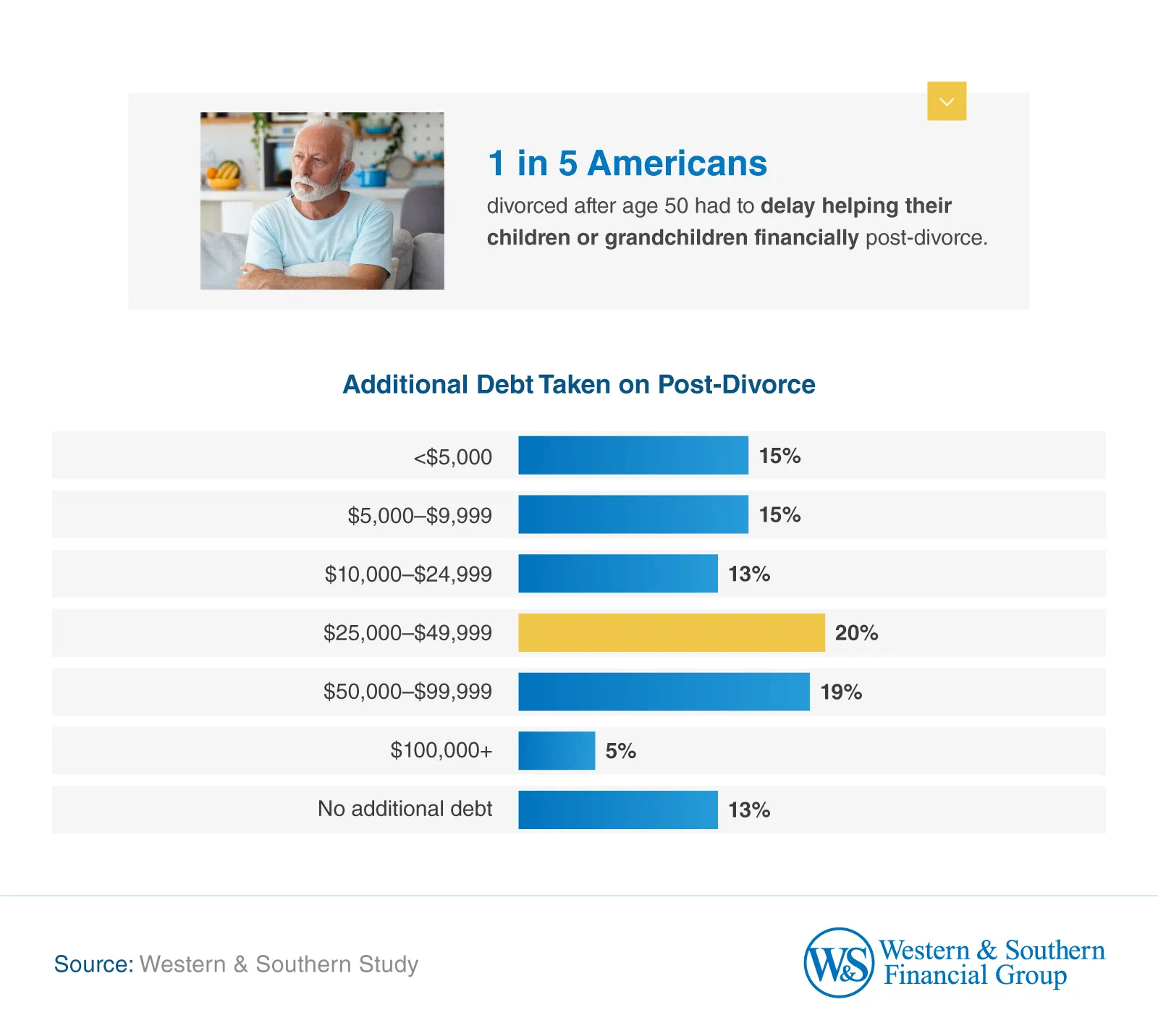

The financial ripple effects extend beyond retirement accounts into everyday obligations and family support. Two-thirds of survey respondents (67%) took on additional debt after divorce, with the median person accumulating between $25,000 and $49,999. Twenty percent also said they had to delay helping children or grandchildren financially, which highlights how gray divorce can disrupt multiple generations at once.

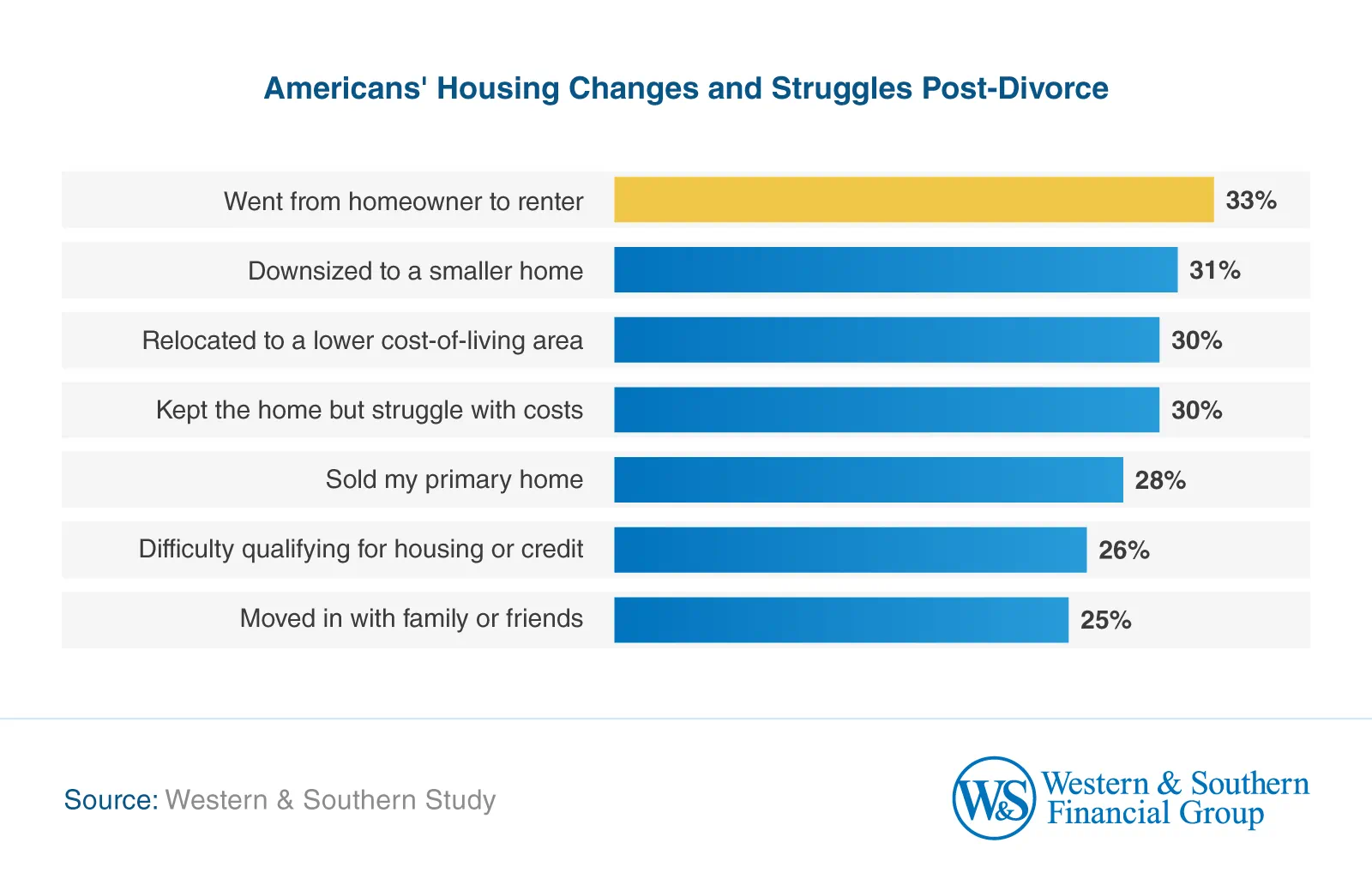

Maintaining housing stability can be more difficult after a gray divorce. One-third of respondents reported moving from homeownership to renting, making it the most common post-divorce housing shift. Nearly as many downsized to a smaller home (31%) or relocated to a lower-cost area (30%).

Even those who stayed put face mounting pressure. Three in 10 respondents kept their home but struggled to afford ongoing costs, while 28% sold their primary residence altogether. More than one-quarter reported difficulty qualifying for housing or credit (26%), and a similar share had to move in with family or friends (25%).

Gender Differences in Post-Divorce Financial Experiences

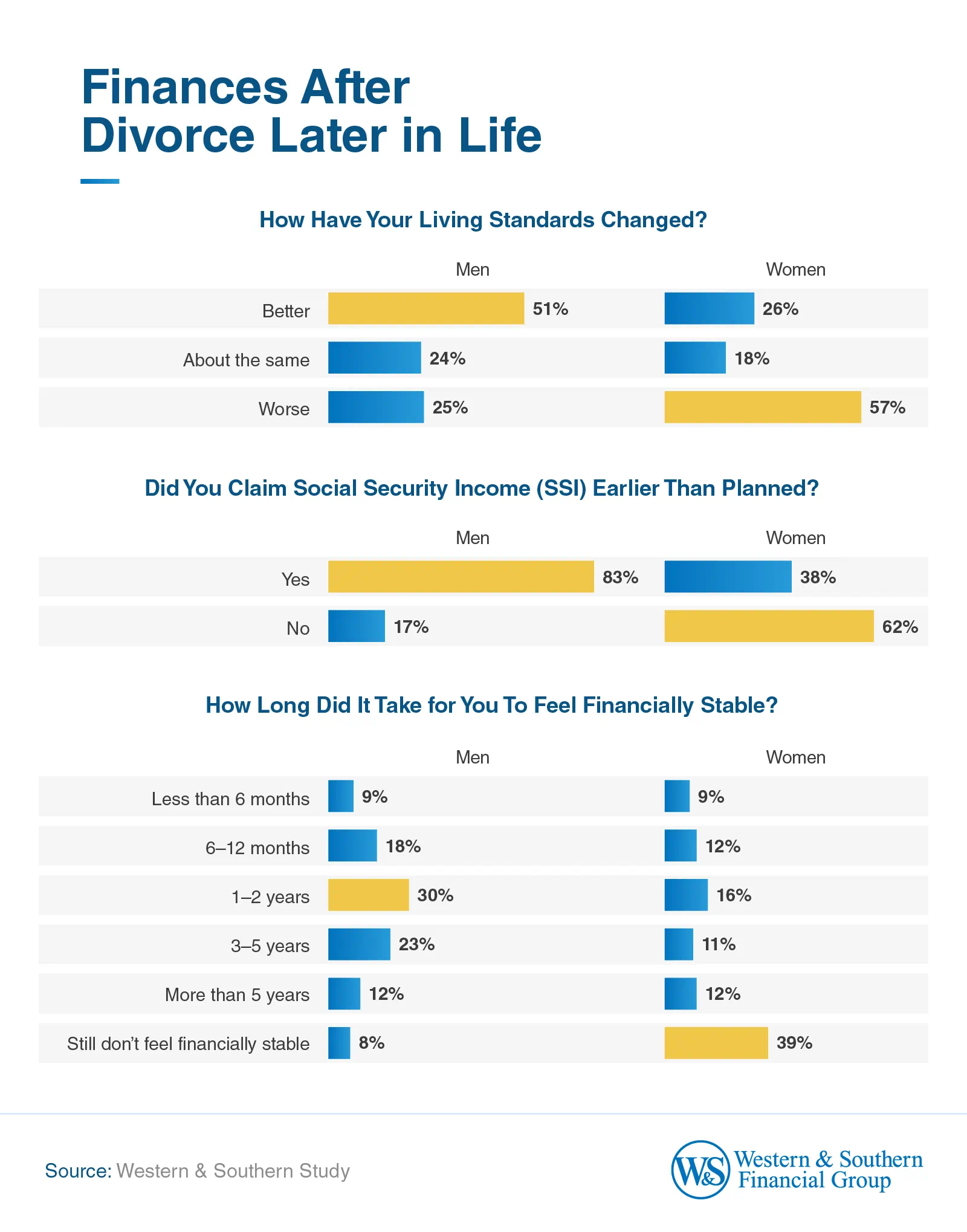

Women in this study reported experiencing a steeper dip in financial well-being after gray divorce than men. While 35% of respondents reported a decline in their standard of living, that share rises to 57% among women, compared to 25% of men.

Men were also more likely than women to say their living situation had improved (51% vs. 26%). And nearly 2 in 5 women (39%) said they still don't feel financially stable post-divorce, compared to 8% of men.

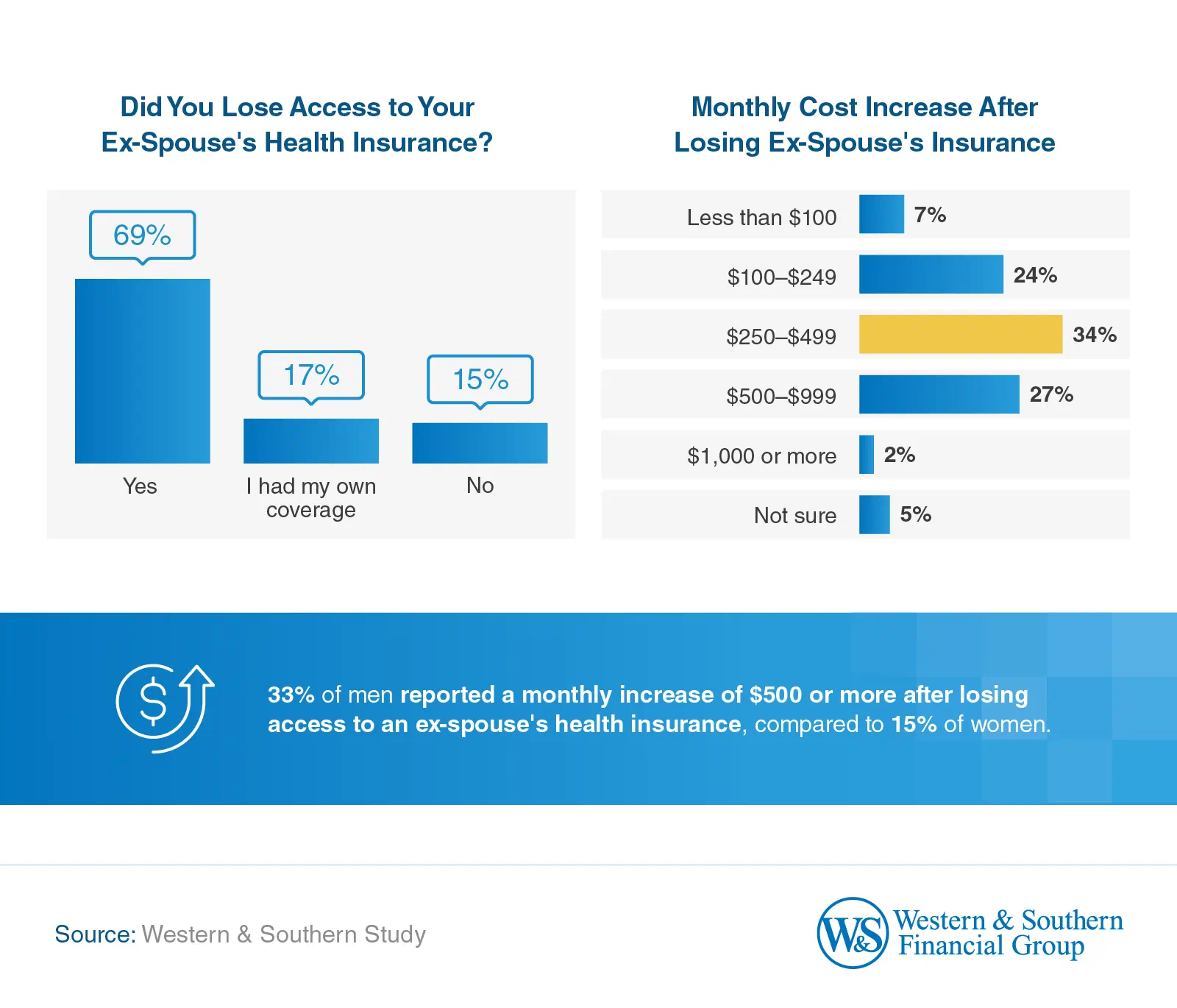

Divorce also affects income timing and healthcare access. About 7 in 10 respondents (71%) claimed Social Security earlier than planned, with men (83%) doing so more often than women (38%). Health insurance losses are widespread, with 69% losing access to a spouse's coverage.

Legal protections further widen the gap after a gray divorce. A Qualified Domestic Relations Order (QDRO) — a legal document used to divide retirement benefits in a divorce — was handled correctly for fewer than one-quarter of women (24%), compared with nearly two-thirds of men (63%). More than 4 in 10 women (43%) said no QDRO was used at all, increasing the risk of retirement asset losses that can be difficult to recover later in life.

Support, Decisions, and Reflections After Divorce

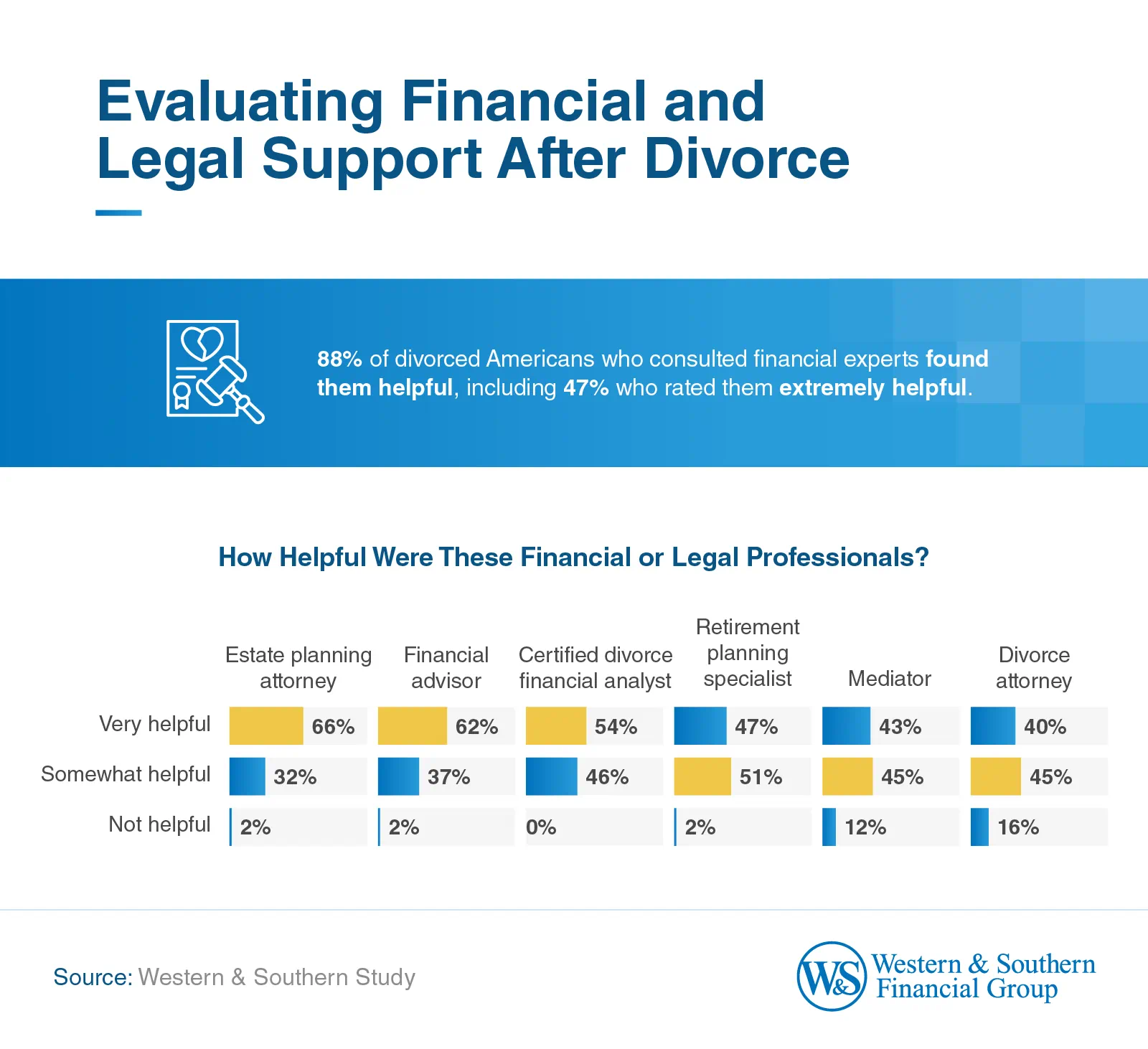

Nearly 9 in 10 respondents who consulted financial or legal professionals (88%) reported that the guidance was helpful. That includes 47% who said these professionals were extremely helpful.

Estate planning attorneys (66%), financial advisors (62%), and certified divorce financial analysts (54%) were most often cited as very helpful.

Survey respondents who worked with retirement-focused professionals were more likely to report that their QDROs were handled correctly, including 88% who used estate planning attorneys and 71% who worked with certified divorce financial analysts. Proper execution drops sharply among those who relied only on a divorce attorney (55%).

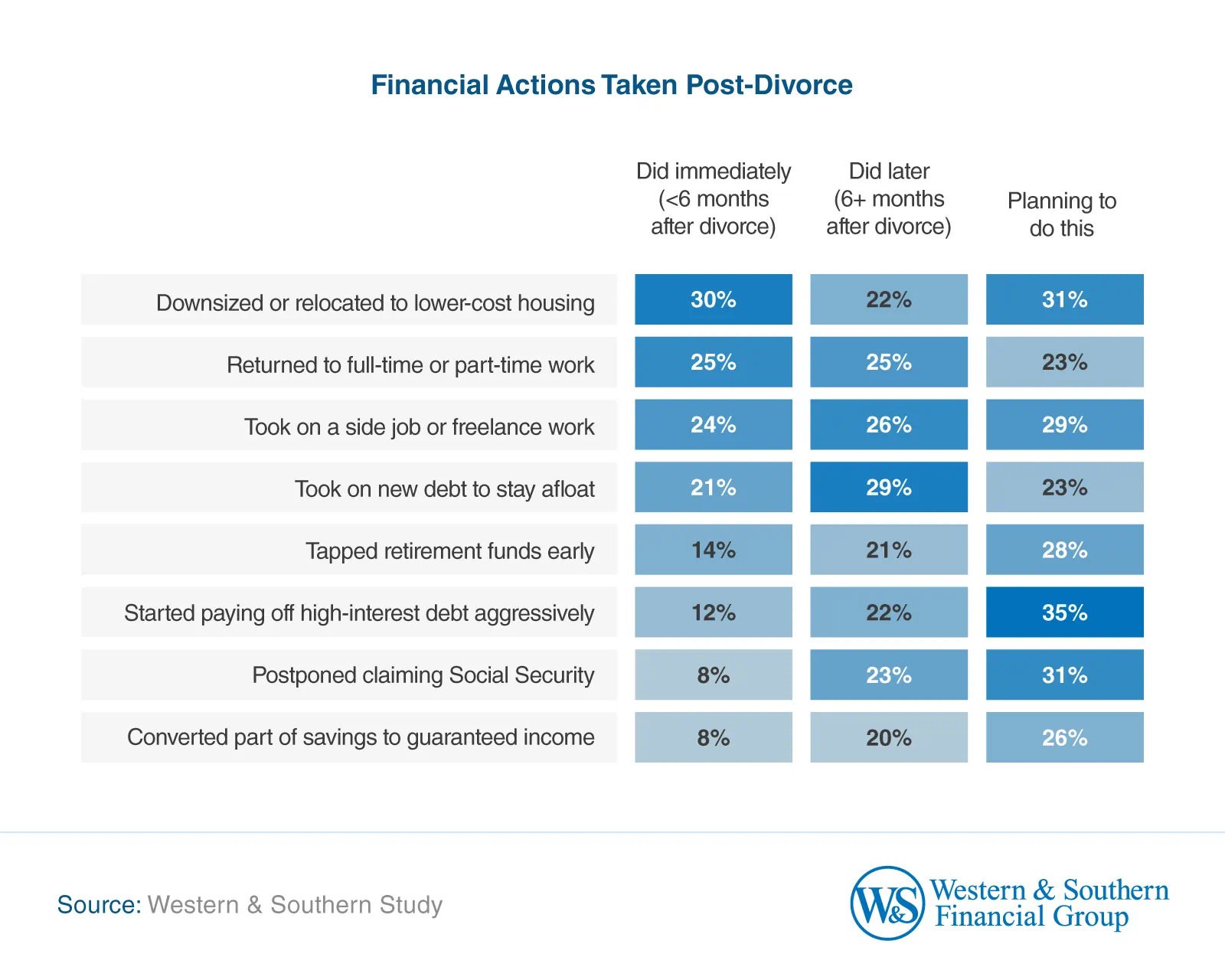

Many respondents reported making reactive financial decisions shortly after divorce. Thirty percent downsized or relocated immediately after, while 21% took on new debt within 6 months just to stay afloat.

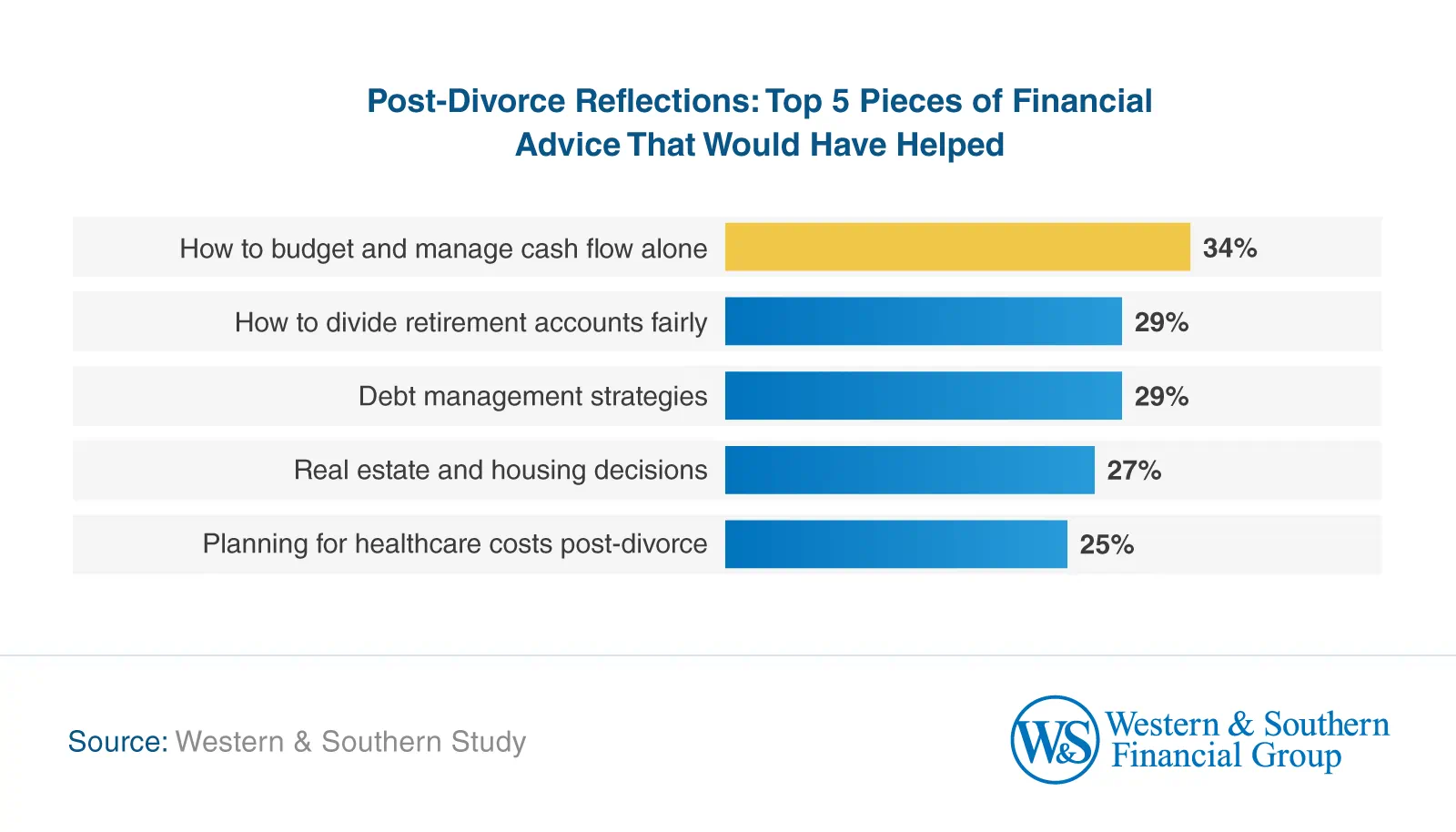

After going through a gray divorce, respondents reflected on what financial advice would have helped them most. Their top answers included knowing how to budget and manage their finances (34%), understanding how to divide retirement accounts fairly (29%), and having strategies for managing debt (29%).

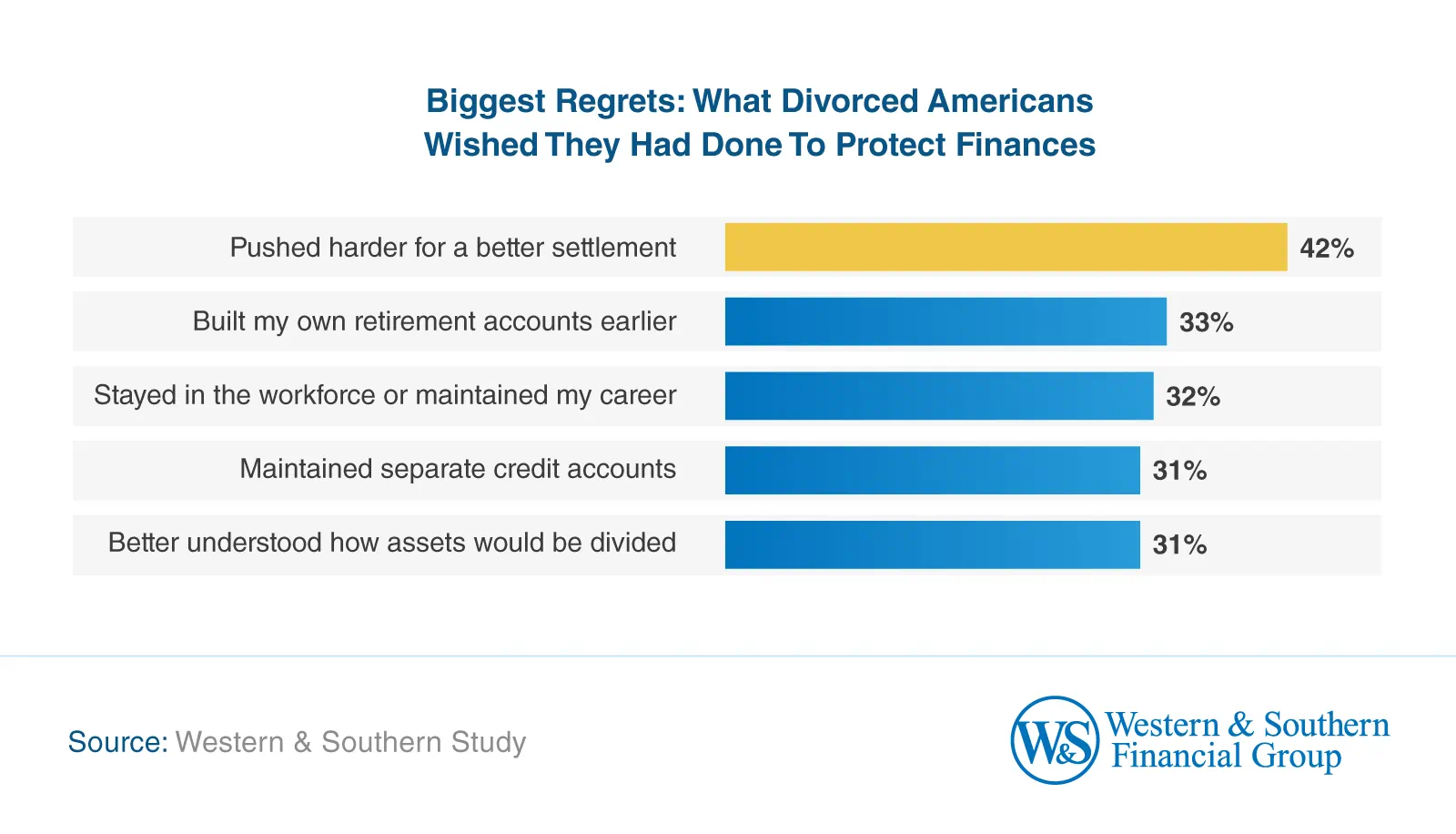

When it came to financial regrets, respondents most often wished they had pushed harder for a better settlement (42%). Another 33% regretted not starting their own retirement account earlier.

Steps Toward a Stronger Financial Future

Divorce brings financial challenges, but thoughtful planning can help mitigate the impact. Reviewing retirement accounts, securing legal protections like QDROs, and reassessing life insurance coverage are key steps toward regaining stability. Working with a financial professional can also help provide clarity and confidence as you plan for the years ahead.

Methodology

This study surveyed 235 U.S. adults who reported being divorced at age 50 or older to examine the financial fallout of gray divorce. Responses were collected via Connect, Prolific, and MTurk between December 2025 and January 2026. Of respondents, 69% identified as men and 31% as women, and 13% reported being ineligible to receive Social Security Income.

Outcome-based percentages include only respondents who provided definitive answers. Those who were already retired, had no retirement plans, were unsure, or selected "prefer not to answer" were excluded from relevant calculations but retained in charts for transparency. Some questions allowed multiple responses, so totals may exceed 100%.

Median values reflect the response range in which cumulative responses exceeded 50%. Average (mean) figures were estimated using conservative midpoints for each range, with open-ended categories assigned conservative floor values. Gender comparisons reflect relative differences within the survey sample only and do not imply causal relationships.

Findings are based on self-reported data and may be subject to recall bias or personal interpretation. Respondents also self-selected whether to work with financial or legal professionals, meaning differences in reported outcomes may reflect underlying financial resources, planning experience, or divorce complexity rather than a direct cause-and-effect relationship.

The study also does not account for regional cost-of-living differences, variations in state divorce laws, or differences in access to employer-sponsored benefits, and results should be viewed as directional rather than precise financial measurements.

About Western & Southern Financial Group

Founded in Cincinnati in 1888 as The Western and Southern Life Insurance Company, Western & Southern Financial Group, Inc., is No. 310 on the Fortune 500® and the parent company of a group of diversified financial services businesses. It serves 6.5 million customers — individuals, families, businesses, foundations and nonprofits — with a wide range of insurance, investment and retirement solutions through an ever-growing distribution system. Assets owned ($86.8 billion) and managed ($43.7 billion) totaled $130.5 billion as of Sept. 30, 2025.1 Western & Southern is one of the strongest life insurance groups in the world, with seven life insurance subsidiaries that maintain very strong financial strength ratings. For more information, visit westernsouthern.com.

1 The financial information presented here is preliminary and unaudited.Review our current financial ratings.

From Fortune. ©2025 Fortune Media (USA) Corporation. All rights reserved. Used under license. Fortune and Fortune 500 are registered trademarks of Fortune Media (USA) Corporation and are used under license. Fortune and Fortune Media (USA) Corporation are not affiliated with, and do not endorse products or services of, Western & Southern Financial Group.

Fair Use Statement

This content may be shared for non-commercial purposes with proper credit to Western & Southern and a link to the original study.

Western & Southern Financial Group and its member companies do not provide legal services, divorce mediation, divorce analysis, or estate planning services, and we do not act as a divorce attorney, mediator, or legal advisor. Individuals should seek the advice of an appropriate professional regarding their specific circumstances.