Caring for an aging parent is one of the most personal things a person can do, and one of the most financially consequential. To understand how caregiving is affecting retirement and financial decision-making, Western & Southern surveyed 1,008 middle-aged Americans who are currently providing financial support, hands-on care, or both for an aging parent or in-law.

Among this group of surveyed caregivers, the costs go well beyond monthly expenses. Many are delaying retirement, making workplace sacrifices, and carrying financial stress they haven't shared with the people closest to them.

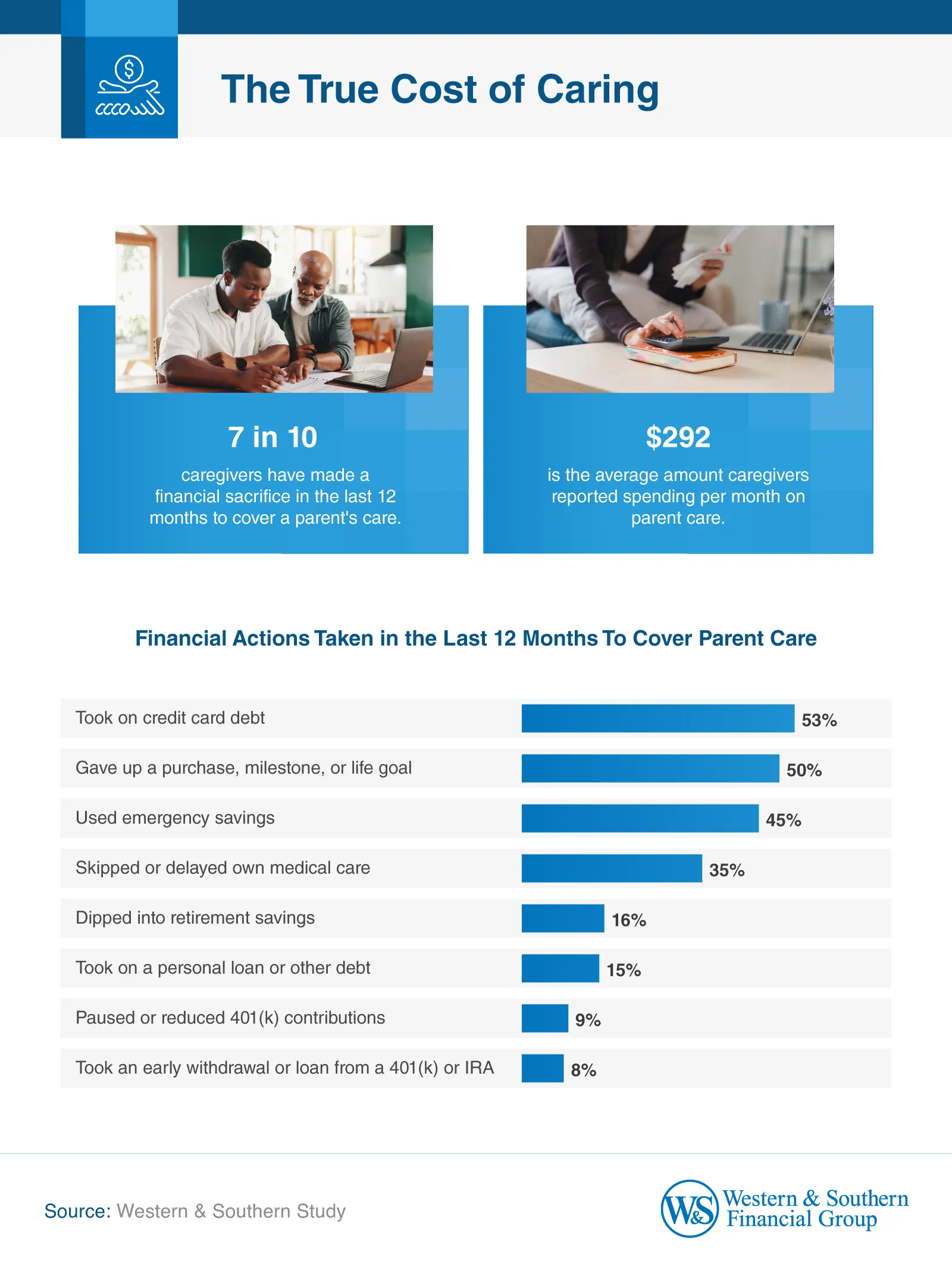

Caregivers Are Sacrificing

Supporting an aging parent often extends beyond occasional help with errands. For many middle-aged Americans, the financial burden is adding up quickly.

Caregivers reported spending an average of $292 per month on parental care, and 7 in 10 said they made a financial sacrifice within the past year to keep up with those responsibilities. Some also turned to long-term savings to bridge the gap. Nearly 1 in 10 caregivers (8%) withdrew money from a retirement account, averaging $5,787 per withdrawal.

More than 3 in 4 caregivers (78%) said they permanently gave up a significant purchase, milestone, or personal goal because of elder care costs. The most significant were:

- Travel or vacation: 19%

- Personal hobbies or pursuits: 12%

- Buying or upgrading a home: 12%

- Home renovations or repairs: 6%

- A new vehicle: 6%

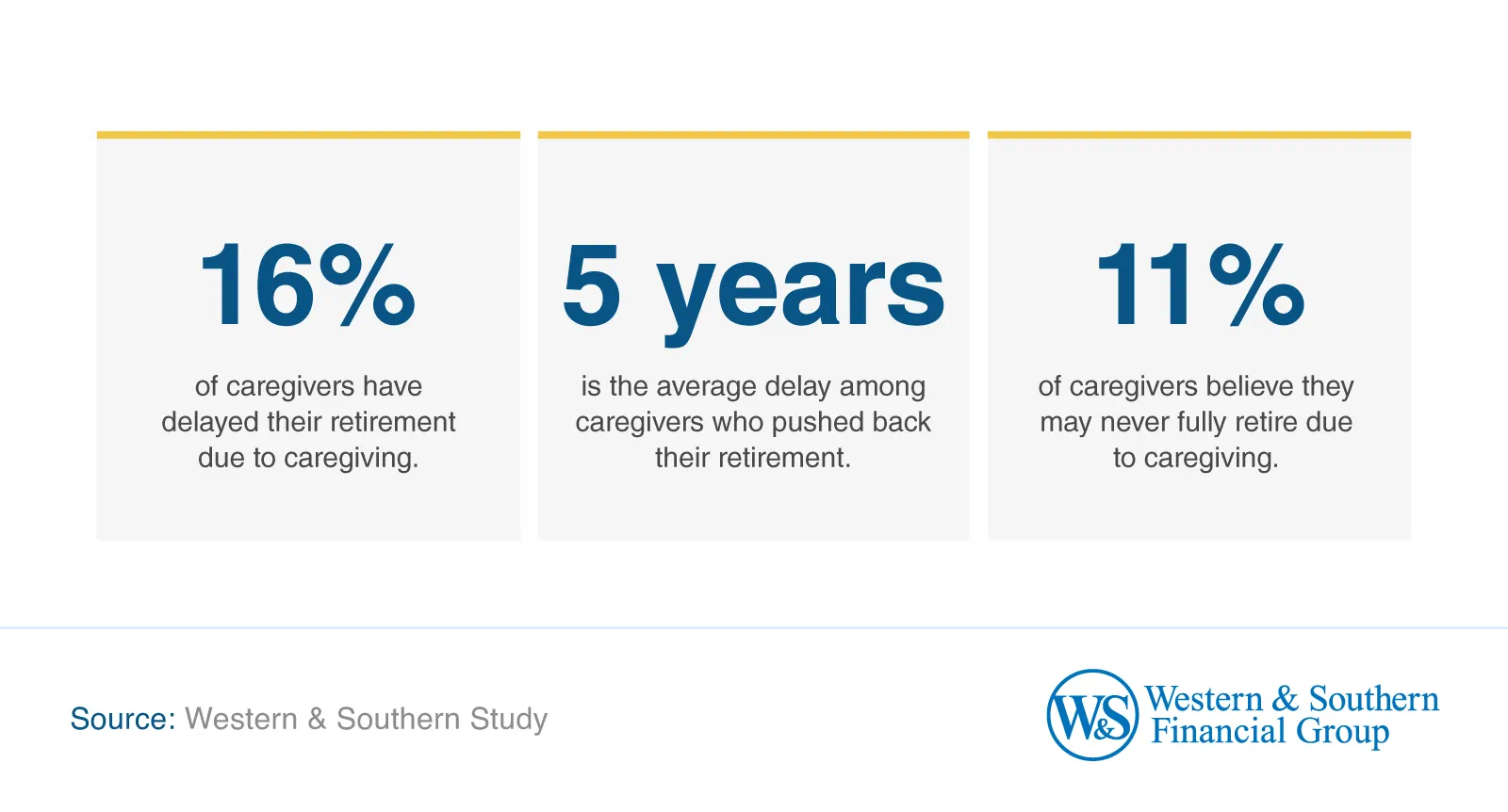

Overall, 16% of caregivers have delayed their retirement to support an aging parent, postponing it by an average of 5 years.

Caregiving pressures were also associated with emotional strain within households, with 52% saying caregiving has caused family tension. More than 1 in 4 caregivers (27%) said they've hidden the financial strain from their children. Another 22% concealed it from siblings, and 19% kept it from a spouse or partner.

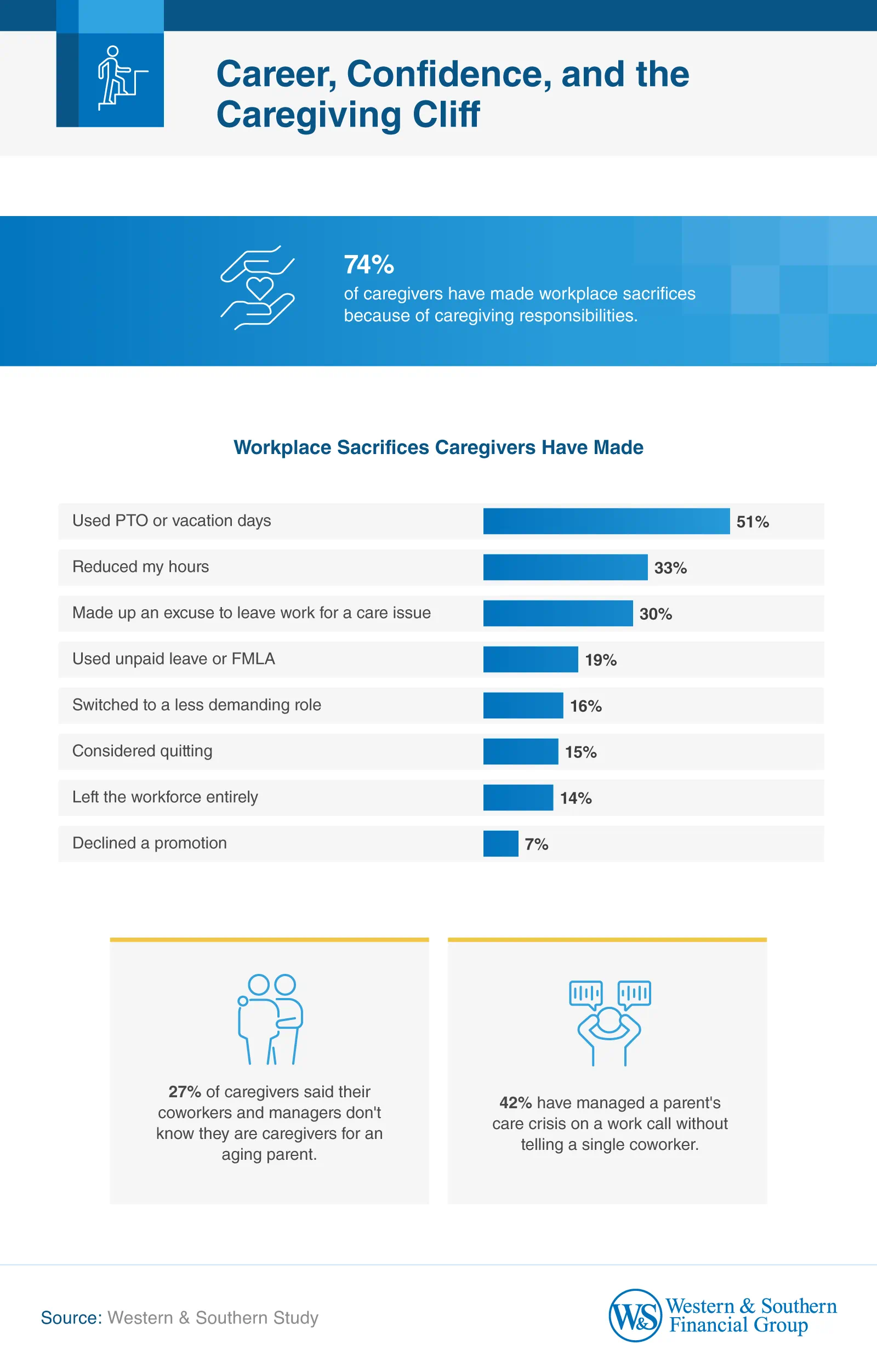

When Caregiving Collides With Work

For many surveyed caregivers, balancing a career and caregiving responsibilities has proven difficult. Nearly three-quarters (74%) said they've made workplace sacrifices because of caregiving. Those compromises ranged from using PTO to turning down promotions.

Return-to-office policies have added another layer of pressure. One-third of caregivers said in-office mandates have made caregiving harder or caused them to consider leaving their jobs. For employees already managing appointments, emergencies, and daily support tasks, less flexibility can create difficult trade-offs between work and family responsibilities.

Caregiving challenges were also associated with lower retirement confidence. More than 1 in 4 caregivers (27%) said they are not at all confident they'll be able to retire comfortably, while 11% now believe they may never fully retire.

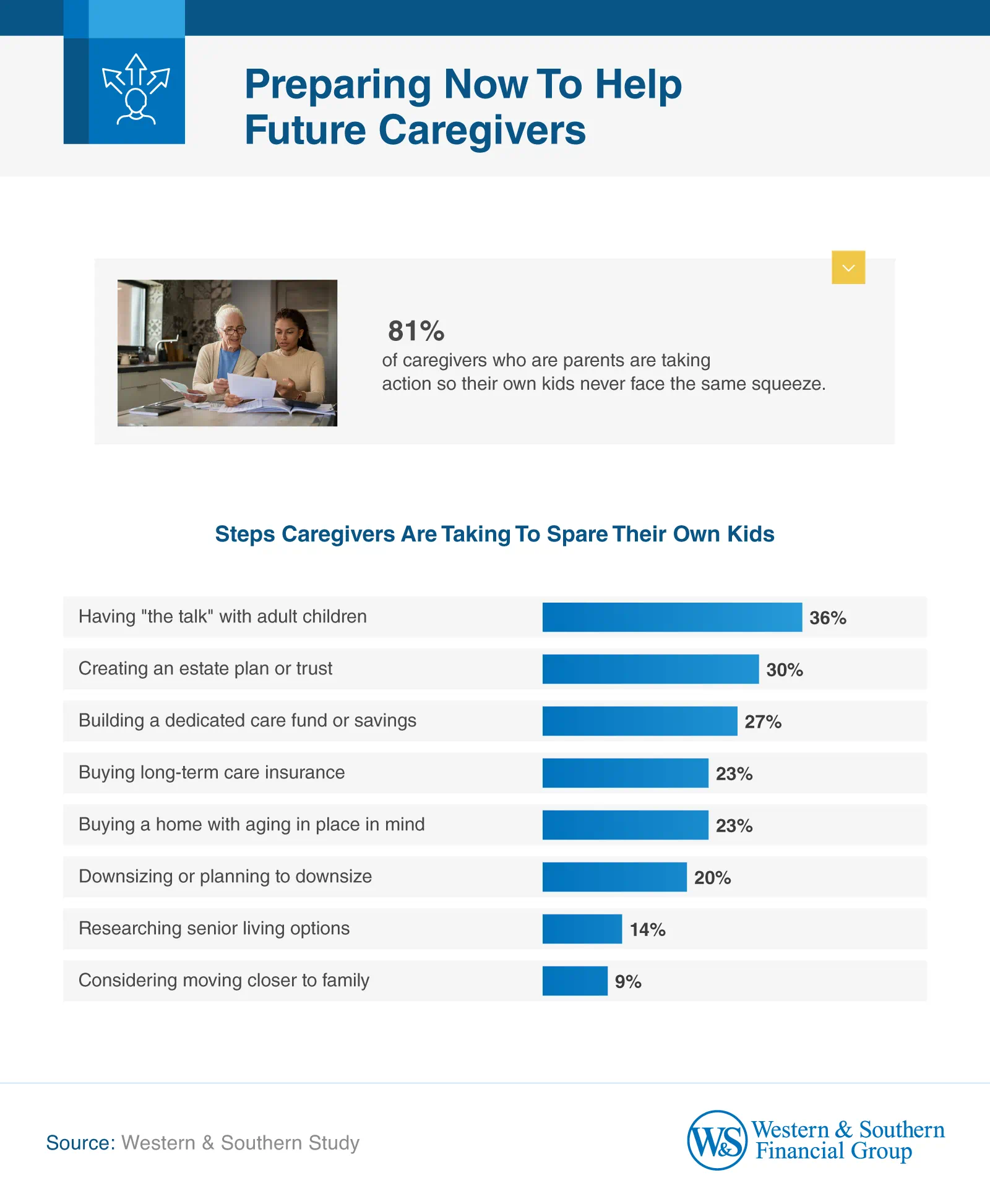

Lessons Learned

Watching parents age has influenced how people think about their own financial future. Among caregivers who are parents themselves, 81% said they are taking steps to help their children avoid facing the same financial and emotional pressure later in life.

Caregiving has left a significant share feeling less prepared for their own retirement years. While 32% said the experience has made them feel more financially prepared for aging, 46% reported feeling less prepared after watching their parents struggle financially or medically.

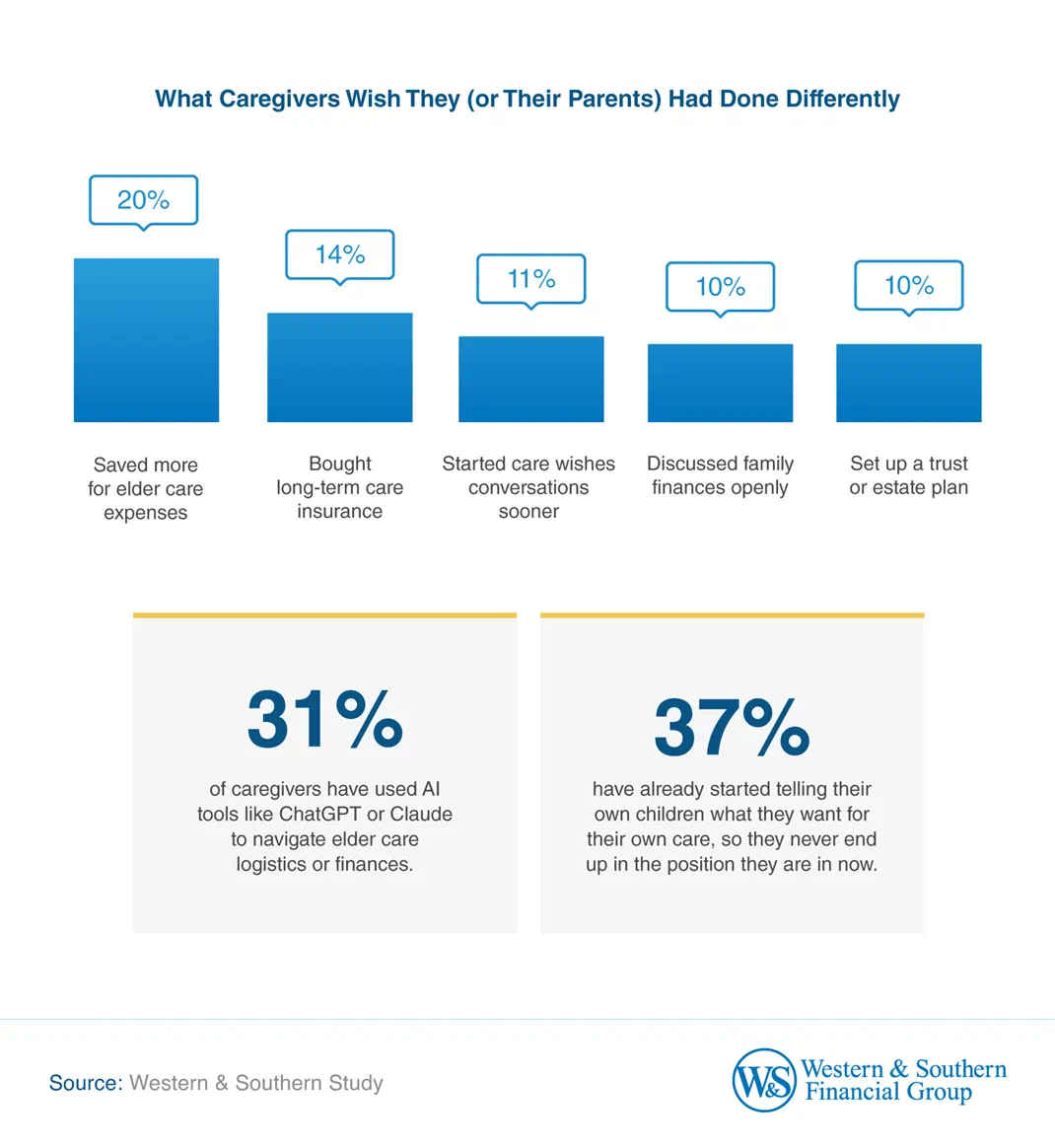

When asked what they or their parents could have done differently, saving more for senior care expenses topped the list, cited by 1 in 5 surveyed caregivers. More than 1 in 10 caregivers (14%) also wished they or their parents had bought long-term care insurance.

Some caregivers are turning to technology for extra support. Nearly 1 in 3 (31%) said they've used AI tools like ChatGPT or Claude to help manage elder care logistics or financial questions. From organizing appointments to researching care options, digital tools are becoming part of how some families manage caregiving responsibilities.

Rethinking Retirement & Family Financial Protection

For many in this sample, going through the experience of caregiving has prompted a closer look at their own financial strategy, and what they might do differently for the people who come after them. The costs, both financial and personal, tend to catch families off guard. Earlier conversations and retirement planning for caregivers may be worth considering before the pressure arrives.

Methodology

Western & Southern surveyed 1,008 middle-aged Americans who currently provide financial support, hands-on care, or both for an aging parent or in-law. Respondents represented a mix of generations, household incomes, and employment statuses. The generational breakdown was 51% millennials, 45% Gen X, and 4% baby boomers. Sixty-two percent identified as women, and 37% identified as men. All respondents were actively providing care for an aging parent or in-law at the time of the survey. Data was collected in May 2026.

About Western & Southern Financial Group

Founded in Cincinnati in 1888 as The Western and Southern Life Insurance Company, Western & Southern Financial Group, Inc., is No. 321 on the Fortune 500® and the parent company of a group of diversified financial services businesses. It serves 6.3 million customers — individuals, families, businesses, foundations and nonprofits — with a wide range of insurance, investment and retirement solutions through an ever-growing distribution system. Assets owned ($90.0 billion) and managed ($42.3 billion) totaled $132.5 billion as of Mar. 31, 2026.1 Western & Southern is one of the strongest life insurance groups in the world, with seven life insurance subsidiaries that maintain very strong financial strength ratings. For more information, visit westernsouthern.com.

1 The financial information presented here is preliminary and unaudited.

Review our current financial ratings.

From Fortune ©2026 Fortune Media IP Limited. All rights reserved. Used under license. Fortune and Fortune 500 are registered trademarks of Fortune Media IP Limited and are used under license. Fortune Magazine and Fortune Media (USA) Corporation are not affiliated with, and do not endorse products or services of, Western & Southern Financial Group.

Fair Use Statement

This content may be shared for non-commercial purposes with appropriate credit to Western & Southern Financial Group and a direct link to the original study.