If you and your family rely on your paycheck, you are relying on your ability to stay healthy. However, that is not guaranteed. The Social Security Administration estimates that before retirement, one out of every four 20-year-olds will develop a disability that keeps them out of work for at least a year.1

While Social Security Disability Insurance offers some protection if you cannot work, there are limits on when and how much this program will pay. That is why it may make sense to consider your own disability insurance policy.

Want to understand how disability insurance works? Here is what to know about these policies and how to decide if one may fit your situation.

What Is Disability Insurance?

Disability insurance provides monthly income if you become disabled. It is usually based on a percentage of your pre-tax income. For example, if you earn $4,000 a month before taxes and your policy covers 60% of your income, you would receive $2,400 a month after a disability.

When you apply, you will choose the amount you want to receive as a benefit. A higher benefit amount usually means a higher cost for the policy.

If you become partially disabled, the policy may provide a reduced payment. For example, if your condition limits you to working half your usual hours, you may receive half of your benefit.

When Do Payments Begin?

Disability income insurance falls into two main categories: short-term and long-term. Each differs in how quickly payments begin and how long they last. Most policies include a waiting period before benefits start, called the elimination period. For example, a one-month elimination period means you must be disabled for more than one month before receiving payments.

Short-Term vs. Long-Term Disability Insurance

| Feature | Short-Term Disability | Long-Term Disability |

|---|---|---|

| Waiting Period | Usually under 2 weeks | Often around 90 days |

| When Payments Begin | Sooner | Later |

| How Long Payments Last | A few months, up to 2 years | Several years, until age 65, retirement age, or longer |

The longer the disability insurance benefits payout period, the more your policy is likely to cost.

Which Physical or Health Issues Qualify for Payments?

Insurance companies often take a broad view of what qualifies for disability insurance benefits. Instead of listing specific illnesses or injuries, they focus on whether your condition is serious enough to keep you from working. A medical provider must make this determination.

Some conditions that may qualify include:

- Heart problems

- Cancer

- A back injury

- Blindness

- Lost of a hand or finger

- Pregnancy

Insurance policies have different standards for what counts as a disability. Some use an "own occupation" standard. You may qualify if a disability prevents you from doing your specific job. Others use an "any occupation" standard. This means the condition must be severe enough to prevent you from doing any type of work.

For example, if a surgeon loses a hand, they would likely qualify under an "own occupation" standard because they can no longer perform surgery. However, they may not qualify under an "any occupation" standard because they could still provide medical advice or teach students.

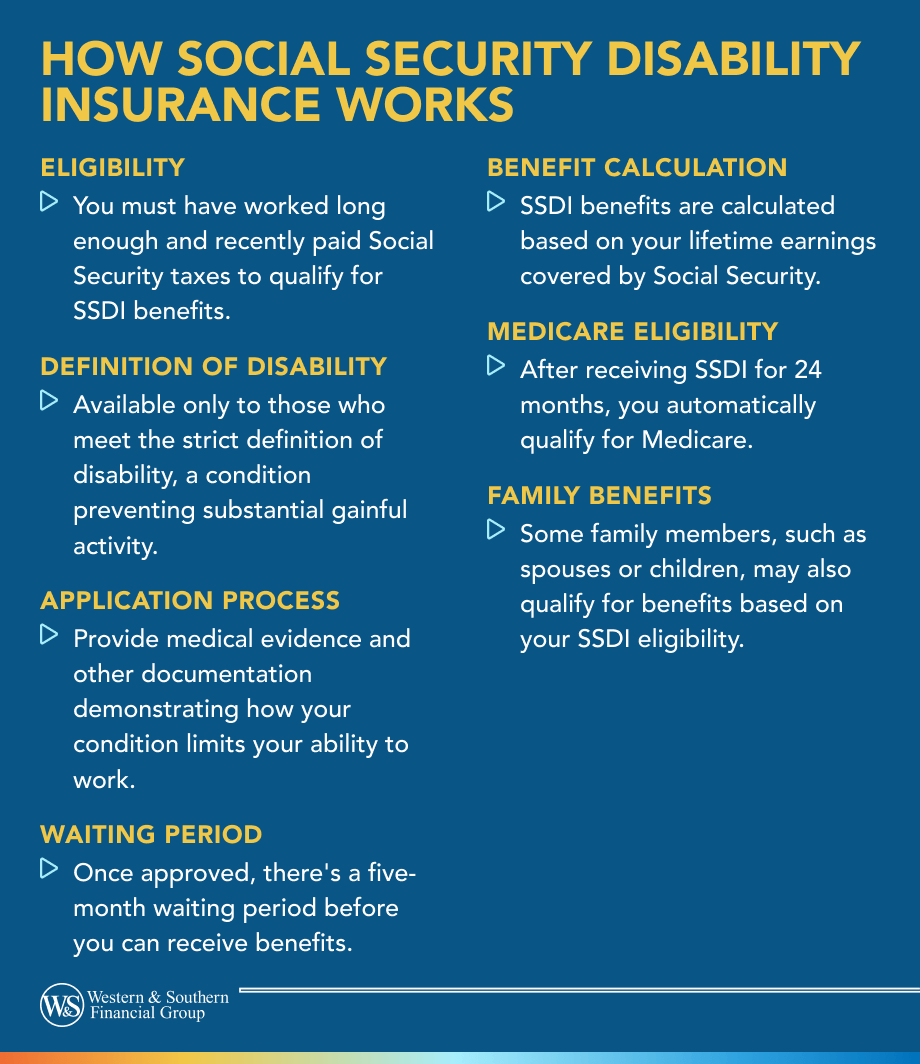

How Does Private Insurance Compare to Government Programs?

The federal government offers disability benefits through Social Security. There are two programs:

- Social Security Disability Insurance (SSDI): For people who have worked and paid Social Security taxes

- Supplemental Security Income (SSI): For people with very limited income and assets

To qualify for SSI, you must have less than $2,000 in assets.2 Both programs are designed for individuals with a serious disability expected to prevent work for at least one year.

Key Differences

The table below highlights how these options compare across key areas.

| Feature | SSDI | Private Insurance |

|---|---|---|

| Eligibility | Must meet strict "any occupation" definition | May use "own occupation" definition |

| Approval Time | Can take months to approve and begin payments | May begin sooner |

| Type of Disability Covered | Total disability only | May cover partial disability |

| Monthly Benefit Limits | Capped and may not cover all expenses | Can supplement income needs |

What This Means for You

SSDI has strict qualification rules and may take time to start payments. Benefits are limited and only apply if you cannot work at all.

Private insurance may offer more flexibility. It can provide coverage if you are unable to perform your specific job and may offer partial benefits. It can also help cover gaps if government benefits are not enough to meet your expenses.

What Are the Benefits of Disability Insurance?

There are several potential advantages to disability insurance. Someone who qualifies may choose to sign up for the following reasons:

- Keeps Your Income Going: Medical issues are a leading cause of bankruptcy in the United States. People may struggle to cover care costs and miss work. When income stops, it can lead to debt, missed housing payments, and risk of eviction or foreclosure. Disability insurance helps replace lost income so you can focus on recovery.

- Helps Protects Your Savings: Only 46% of Americans have enough emergency savings to cover at least three months of expenses.3 A serious disability can quickly drain those funds and may force withdrawals from retirement accounts, which can trigger taxes and IRS penalties. Disability insurance can provide income replacement and help you avoid using savings or retirement funds.

- Offers Tax-Free Benefits: If you pay for your own disability insurance, benefits are usually not taxed as income. Policies often replace 40% to 70% of your salary, and because taxes are not withheld, payments may cover a large share of your take-home income.

- Fills the Gaps in Government Programs: Social Security may provide long-term disability benefits, but approval can take time. Private disability insurance can help cover expenses while you wait and may offer higher monthly payments or benefits for partial disabilities.

What Are the Possible Drawbacks?

There are some downsides to disability insurance. Someone who qualifies might decide not to sign up for reasons such as these:

- Cost of Coverage: According to the nonprofit Life Happens, a long-term disability insurance policy may cost about 1% to 3% of your pre-tax income each year.4 Costs are often higher for older applicants, those with certain health conditions, and people in higher-risk jobs such as construction.

- Use-It-Or-Lose-It Benefits: Most disability insurance policies follow a use-it-or-lose-it structure. You only receive benefits if you become disabled.

- Wait Time Before Payments: Most policies include an elimination period. This is the amount of time you must wait before benefits begin. The waiting period can range from days to months. If you recover before the elimination period ends, you may not receive any payments.

- Coverage Qualification: To qualify for disability insurance, you usually need to complete medical underwriting. If you have preexisting conditions or health concerns, the insurer may charge higher premiums.

Are There Alternatives to Disability Insurance?

Workers' compensation provides disability benefits if you get hurt or become sick at work. However, it does not cover disabilities caused outside of your workplace.

Your employer may also offer group disability insurance as an employee benefit. They might pay some or all of the insurance premiums, which can lower your out-of-pocket cost compared to buying your own policy. However, if you leave your job, you will usually lose this coverage.

Another option is a critical illness insurance policy. These policies cover specific conditions, such as a heart attack, stroke, cancer, paralysis, or an organ transplant. If you are diagnosed with one of these conditions, the policy pays a lump-sum benefit. This is a one-time payment, unlike disability insurance, which may provide ongoing income.

You can also add a disability waiver of premium rider to a life insurance policy. If you become disabled, the insurer will stop charging your life insurance premiums. This can reduce your monthly expenses and help you keep your coverage in place. If your policy has cash value, it can continue to grow over time.

Do You Need Disability Insurance?

Consider how you would manage a long period without income due to a disability. Insurance can help, but it is not the only option. If you have strong savings or other sources of support, you may not need an individual policy.

Your current financial strategy may also cover some types of disability but not all. Insurance can help fill those gaps.

For example, you might skip short-term disability insurance if you have enough savings to replace your income for a few months. However, you could choose a long-term disability policy to help cover a lasting condition. Another option is to use short-term coverage for minor illnesses or injuries, with the expectation that you may qualify for Social Security Disability Insurance (SSDI) if a serious issue occurs.

Another factor to consider is whether you can handle the cost of premiums. If cost is a concern, you could choose a policy that replaces only part of your income. You can do this by lowering the monthly benefit, shortening the payout period, or increasing the waiting period before benefits begin.

With this approach, your premiums may cost less while still providing some level of income support. If you become disabled, you would have partial income replacement, which can help reduce how much you need to withdraw from your savings.

How Do You Apply for Disability Insurance?

There are several ways to apply for a disability insurance policy. Here is a simple four-step process.

1. Contact an Insurance Company

When you contact an disability insurance company, you will speak with a financial professional. They will review your situation and explain available policies. You can then choose:

- Short-term or long-term coverage

- Coverage amount

- Elimination period

- Optional policy features

2. Submit an Application

If you're interested in disability insurance, you'll need to submit an application. To do so, you will need to provide:

- Contact information

- Occupation

- Current earnings

- Preferred policy type

Because disability insurance is based on replacing your current earnings, you may need to submit pay stubs or your tax return to show how much you're currently making. You might also need to answer health questions and take a medical exam.

3. Receive the Insurer's Decision

The insurance company will review your application, earnings and medical records. After review, they will decide whether you qualify and at what premium. If you have preexisting medical conditions, they could charge more, deny the application or give you a policy that excludes covering the condition.

For example, if you have an existing heart problem, the policy might not cover disability from future heart issues but would for any other cause.

4. Accept the Policy and Pay Your Premium

If you are happy with the insurance offer, you can pay the first premium to set up coverage. From there, you'll be covered as long as you keep up with the premium payments. Should you ever end up being disabled, you will contact the insurance company, file a claim and get a doctor to verify that you are disabled. Once you get past the policy elimination period, you'll start receiving your disability insurance benefits.

Bottom Line

Your need and eligibility for disability insurance depends on many factors. If you feel you could benefit from more information or a personalized look at your individual situation, consider meeting with a financial professional. With their help, you can decide if you need disability insurance and, if so, get the application process started.

Sources

- Disability Benefits. https://www.ssa.gov/pubs/EN-05-10029.pdf.

- Understanding Supplemental Security Income SSI Eligibility Requirements -- 2025 Edition. https://www.ssa.gov/ssi/text-eligibility-ussi.htm.

- Bankrate’s 2026 Annual Emergency Savings Report. https://www.bankrate.com/banking/savings/emergency-savings-report/.

- How much does disability insurance cost? https://lifehappens.org/disability-insurance-101/how-much-does-disability-insurance-cost/.