You're out of college, earning your own income, and deciding how to use it. Your first priority is likely paying off student loans while learning how to manage your expenses. There is another money move you may want to consider: investing.

Investing after college is not something you have to delay until you are older or earning more. Getting started early can work in your favor. Here's why, and how to think about investing while managing your other responsibilities.

Why Invest After College?

With everything else going on after college, why add “learn how to start investing” to your list? One reason is compound returns.

Compound Returns

Compound returns may help your investments grow over time. The money you put into an investment may earn a return. Those returns are added to your original amount, as long as you do not withdraw them, and they can then earn their own returns.

There is no guarantee you will earn a return, and you could lose some or all of your initial investment. Compounding can help your money grow when investments perform well, but there is always risk.

You can use a compound interest calculator to see how time can affect your results. The longer you wait to invest, the more you may limit your potential returns, even if you invest more later. Market performance and interest rates can vary, and losses are possible.

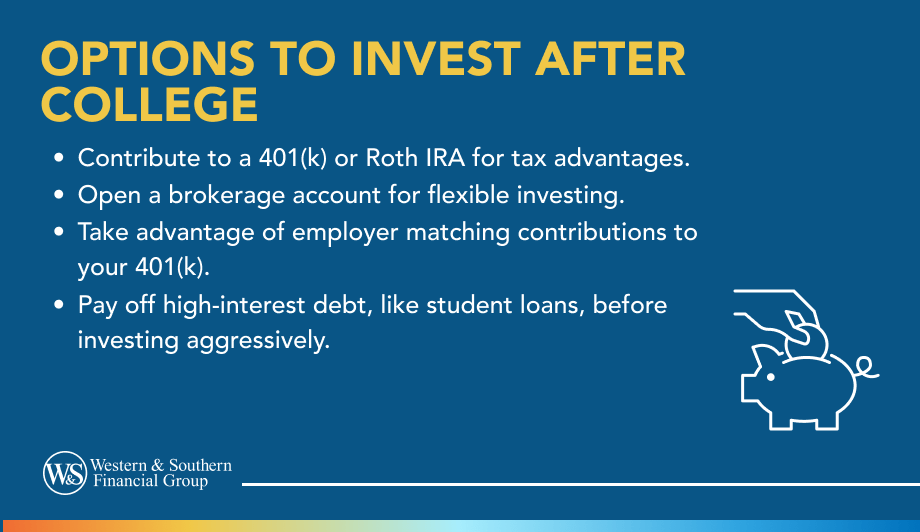

Shouldn't I Pay Off My Debt First?

Investing after college can offer benefits, but it also comes with risk. At the same time, you may have bills and debt to manage. So which should come first: investing or paying off debt?

In some cases, you may be able to do both. A balanced approach may allow you to make progress on student loans while also starting to invest.

One way to think about this is by comparing interest rates. The interest rate on your loan works like a fixed cost. Investment returns are less predictable, which makes this comparison less certain.

Depending on your situation, you might choose to make minimum payments on your debt while investing any extra money you have available.

How Can I Start Investing?

401(K) Plan

You may want to start by contributing to a 401(k) plan or a similar plan, such as a SIMPLE IRA. This can be a good option if your employer offers matching contributions. An employer match can increase the amount going into your account. If you still have room in your budget, you could use additional funds to pay down your student loans faster.

Roth IRA

You could also open a Roth IRA. Qualified withdrawals in retirement may be tax-free if you have held the account for at least five years and are age 59½ or older.

Some people expect to be in a higher tax bracket later in their careers. A Roth IRA is different from a 401(k), where contributions are typically tax-deferred and withdrawals are taxed.

Using both accounts can help you take advantage of different tax treatments. While Roth IRAs allow certain early withdrawals, access to a 401(k) before age 59½ may result in taxes and penalties.

Brokerage Accounts

You might also consider a taxable brokerage account. This type of account allows you to invest through a financial institution and gives you more flexibility to access your money.

Unlike retirement accounts, brokerage accounts do not offer the same tax benefits. However, they can provide more control over when you use your funds. You may want to speak with a registered representative to review your options.

Final Thoughts

Investing after college can feel like a lot to take on, but starting small can make it more manageable. Beginning early gives your money more time to grow. Saving and investing consistently over time can be more effective than waiting and trying to catch up later.