Money worries rarely show up one at a time. Debt, income responsibilities, and long-term obligations often overlap, creating pressure that builds quietly until a major life event forces decisions. Let’s look at how life insurance intersects with common financial challenges and where coverage can help reduce strain when the unexpected happens.

Understanding Common Financial Concerns

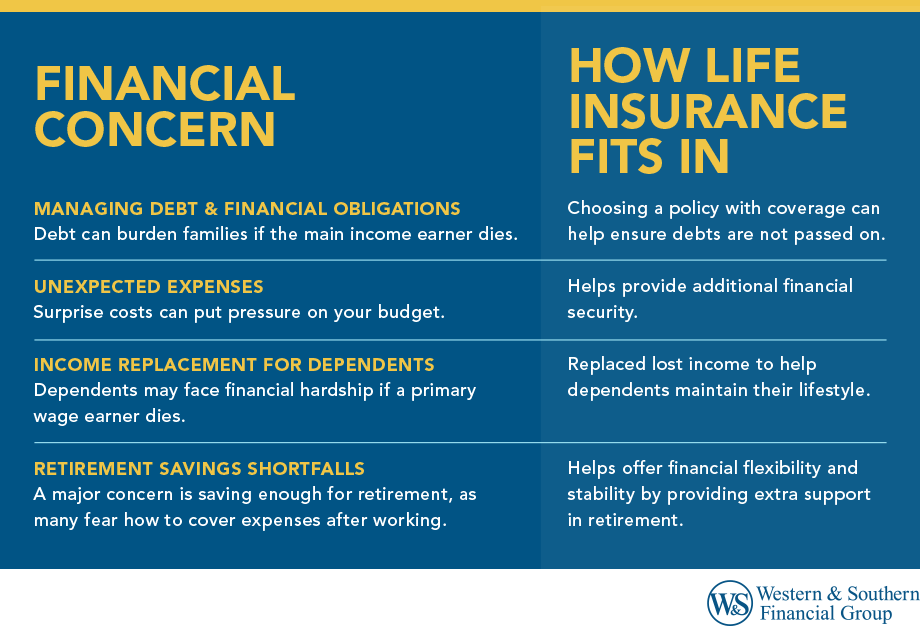

Financial concerns rarely exist in isolation. Debt affects savings. Medical bills delay retirement contributions. A mortgage becomes harder to manage when income disappears. When these issues overlap, risk compounds quickly, especially for families, business owners, and anyone others rely on financially.

Life insurance is not meant to solve every problem. It is designed to respond to one specific event with wide-reaching consequences: death. The financial impact can be immediate and long-lasting.

Managing Debt and Financial Obligations

Most households carry some form of debt, often more than one.

Common obligations include:

- Mortgage payments

- Student loans

- Credit card debt

- Auto loans

- Personal loans

These obligations do not disappear when someone dies. For surviving family members, debt can quickly turn grief into a financial emergency.

If the primary income earner is gone, monthly payments may fall on savings that were never meant to carry that burden. In some cases, surviving spouses or partners may need to liquidate assets or take on additional debt just to keep up.

Life insurance does not eliminate debt, but it can provide liquidity when it is needed most. Timing matters.

Emergency Savings and Unexpected Expenses

Emergency savings play an important role, but they are limited. Medical bills, funeral costs, and sudden income loss can drain even well-funded accounts faster than expected.

Common unexpected expenses include:

- Medical bills tied to illness or accidents

- Funeral and final expenses

- Temporary loss of income for surviving family members

- Immediate household costs while decisions are still unresolved

Life insurance is designed to provide a death benefit. That payout can help cover large, immediate expenses without forcing rushed decisions during a crisis.

Income Replacement for Dependents

When someone provides income, their absence creates a gap that savings alone may not fill. Spouses, children, and other dependents often rely on that income for both short-term needs and long-term stability.

Income replacement is not about duplicating a paycheck forever. It is about buying time.

- Time to adjust

- Time to grieve

- Time to make thoughtful decisions

The right time horizon depends on factors such as:

- Age of dependents

- Existing retirement savings

- Education costs

- Outstanding mortgage payments

This is where term life insurance often plays a central role.

Retirement Savings Gaps and Long-Term Security

Many people reach midlife with unfinished retirement goals. The plan was to catch up later. Increase contributions. Rely on higher income. Then life intervenes.

When one partner dies before retirement, the surviving partner may face:

- Reduced household income

- Lower Social Security benefits

- Ongoing mortgage payments

- Higher medical costs later in life

Life insurance does not replace retirement savings, but it can help offset the strain left behind when long-term plans are interrupted.

How Life Insurance Can Help Address These Financial Concerns

Life insurance is most effective when each concern is paired with a clear purpose. Broad coverage without intention often leads to frustration. Coverage tied to specific needs tends to perform better when it matters most.

Using Life Insurance to Help Protect Against Income Loss

For many households, income replacement is the primary reason for purchasing coverage. Term life insurance is commonly used because the coverage period can align with working years.

A term life policy may help:

- Replace lost income during peak earning years

- Support mortgage payments and education costs

- Reduce pressure to return to work too soon

Illustrative Example

Michael, a 35 year old marketing executive earning $120,000 annually, had two young children and a mortgage. He purchased a $2 million, 30 year term policy for $125 per month. When he died unexpectedly at 42, the death benefit allowed his wife to pay off the mortgage, set aside funds for college, and invest the remaining amount to help replace income.

Results vary. For illustrative purposes only.

Covering Debt and Final Expenses

Debt and final expenses often surface quickly. Life insurance can provide immediate funds that help prevent survivors from using retirement accounts or selling assets under pressure.

Common uses include:

- Paying off mortgage balances

- Eliminating credit card debt

- Covering funeral costs and medical bills

This type of coverage is frequently overlooked until the need becomes urgent.

Life Insurance and Retirement Planning Considerations

Permanent life insurance policies, such as whole life and universal life, include a cash value component that may grow on a tax deferred basis over time.

Some policyholders view this as an added source of flexibility rather than a replacement for retirement savings.

Key limitations to understand:

- Cash value takes years to build

- Premiums are higher than term insurance

- Policy loans can reduce the death benefit

Variable life insurance also introduces market exposure, meaning returns are not guaranteed. Interest rates, policy charges, and market performance all affect results.

Life insurance may complement retirement strategies when used intentionally, but it does not address retirement shortfalls on its own.

Life Insurance as Part of an Estate Plan

Life insurance can support estate planning when funds are needed quickly.

Common estate related uses include:

- Covering estate taxes

- Paying final expenses without selling assets

- Helping equalize inheritances when assets are illiquid

Death benefits are generally income tax free to beneficiaries, though estate taxes may apply depending on ownership and policy structure.

Alignment with wills and trusts is important. Without coordination, even a well structured policy can create unintended issues.

Comparing Life Insurance Options for Different Financial Needs

Various financial concerns necessitate different types of insurance policy structures. There isn't a one-size-fits-all best option.

| Type of Life Insurance | Coverage Duration | Potential Cash Value | Premium Pattern | Best Suited For |

|---|---|---|---|---|

| Term Life Insurance | Fixed period | Majority do not | Lower, fixed | Temporary income replacement |

| Whole Life Insurance | Lifetime | Yes | Higher, fixed | Long-term coverage |

| Universal Life Insurance | Lifetime | Yes | Adjustable | Flexibility in premiums and benefits |

| Variable Life Insurance | Lifetime | Yes, market-based | Fluctuates | Those comfortable with investment risk |

Overall, permanent policies offer long-term coverage, as long as you pay your premiums, but come with complexity. Term policies are straightforward, though they expire when the term ends.

Matching the policy type to the financial concern matters more than the policy label.

How to Choose the Right Life Insurance Policy

Choosing a life insurance policy is less about finding a perfect product and more about understanding which financial risks matter most right now. The right choice today may not be the right choice forever, and that is okay. What matters is alignment between coverage, obligations, and reality.

This decision often sits at the intersection of math and emotion. Numbers matter. Context does too.

Key Factors to Consider

Start with your current financial picture, not an idealized future version of it. Life insurance works best when it reflects how your household actually functions.

Important factors include:

- Dependents and Shared Financial Responsibility: Anyone who relies on your income should factor into the decision. This may include a spouse, children, aging parents, or business partners. The more people who depend on you financially, the greater the impact of lost income.

- Debt and Fixed Obligations: Mortgage payments, student loans, credit card balances, and education costs shape how much flexibility survivors would have. Some debts end at death, but many do not. Knowing which obligations remain matters.

- Time Horizon: Consider how long and how much coverage is truly needed . A 30-year mortgage, children who will be financially independent in 20 years, or a business loan with a defined payoff date may point toward term coverage. Lifetime obligations or estate-related concerns may point elsewhere.

- Budget and Potential Cash Flow: Premiums could fit within any existing cash flow without creating strain. A policy that becomes hard to maintain increases the risk of lapse.

- Health and Underwriting Considerations: Age, medical history, and medical exam results all affect policy costs. Delaying an application can limit options if health changes later.

Working with an experienced insurance agent or financial professional can help clarify tradeoffs, but the final decision should reflect your comfort level and priorities.

How to Estimate the Right Coverage Amount

Coverage amounts feel less abstract when tied to real numbers. Instead of guessing, break the estimate into parts.

Common approaches include:

- Income-Based Estimates: Many households start with a multiple of annual income, often 10 to 15 times. This offers a rough baseline but should not stand alone.

- Debt and Expense Inventory: Add mortgage balances, remaining student loans, credit card debt, and anticipated funeral expenses. These are immediate costs survivors may face.

- Future Financial Needs: Consider education costs, ongoing living expenses, and the retirement outlook for a surviving partner. Even a shorter income replacement period can leave long-term gaps.

- Existing Assets and Savings: Retirement savings, emergency funds, and employer-provided life insurance affect how much additional coverage may be needed. Life insurance is meant to supplement these resources, not replace them.

Coverage needs change over time. Marriage, divorce, children, business ownership, and approaching retirement all warrant a reassessment.

Reassessing and Adjusting Over Time

Life insurance decisions are not permanent commitments to one strategy. Many people layer coverage, combine term and permanent policies, or adjust coverage as obligations shrink.

Regular reviews help answer questions such as:

- Is this policy aligned with current debt levels?

- Have retirement savings grown enough to reduce coverage needs?

- Has income changed significantly?

- Are beneficiaries still appropriate?

Adjustments may include reducing coverage, adding supplemental policies, or converting term coverage when available. The goal is relevance, not constant optimization.

Choosing the right life insurance policy comes down to intention. When coverage reflects real responsibilities and realistic timelines, it is more likely to perform its role when it matters most.

Final Thoughts

Life insurance can be a risk management tool that addresses financial concerns built over time, such as debt and helping protect your family. When integrated into a broader strategy and guided by a professional, it can help families manage uncertainty and mitigate the impact of financial disruptions.

Take steps to address financial concerns with life insurance coverage that fit your goals. Request a Free Life Insurance Quote